Economics

Updated on 2023-08-29T11:59:24.055157Z

How can you Define Economics?

Economics is one of the arms of social science discipline, which is concerned with the description and analysis of manufacturing, distribution and consumption of products and services.

The term ‘Economics’ is believed to be originated from the Greek word ‘Oikonomia’, which means household management. Initially, a Greek philosopher Aristotle defined Economics as a ‘science of household management’, but with time, its definition has changed.

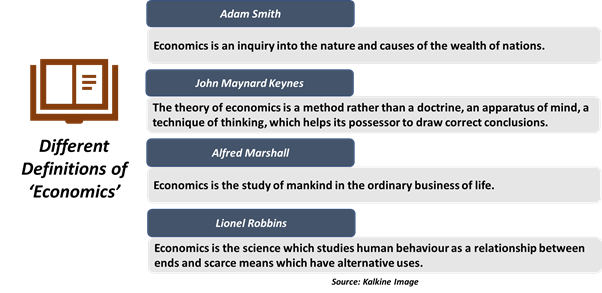

Towards the end of the 18th century, the father of Economics Mr Adam Smith described Economics as a ‘Science of Wealth’, which investigates into the nature and reasons of the wealth of nations. Subsequently, several economists came up with their own definitions of ‘Economics’, some of which are listed in the below figure:

Also Read! What is Behavioural Economics?

What are the Three Fundamental Questions in Economics?

As every economy is limited by its technological knowledge and resources, the society has to answer three fundamental economic questions before making choices. These questions comprise what to produce, how to produce and for whom to produce.

What to Produce?

Given the constraint on availability of resources, economic agents have to determine what to produce for an economy and in what quantity. In today’s economy, goods and services are typically produced based on demand and supply forces. In other words, firms produce commodities that are demanded by the consumers and refrain from making goods not in demand. This prevents the ineffective utilisation of resources and averts wastage.

How to Produce?

While the major aim of any firm producing goods and services is profit maximisation, a key question that arises is determining the methods of production. This question deals with the production process, inputs used in production and proportion in which these inputs will be merged to manufacture goods and services in the most profitable way.

For Whom to Produce?

When the product or service is produced, another key challenge is to analyse who will consume the produced output. In a free market economy, goods are provided to the section of society that carries the ability to pay for them. So, an individual’s income is used as the criteria to decide the quality and quantity of goods and services produced.

However, in more altruistic societies, products and services can also be produced for individuals who cannot afford or pay for them. For instance, free healthcare is provided in many western or advanced economies of the world.

How can you Differentiate Between Macroeconomics and Microeconomics?

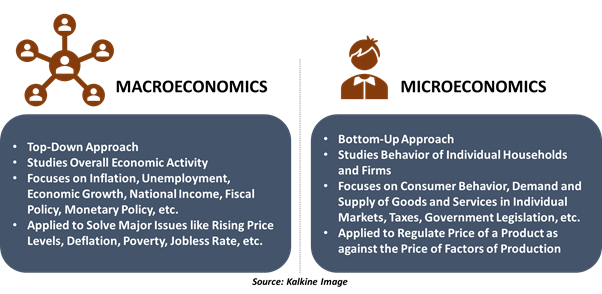

Economics is broadly categorised into two types: macroeconomics and microeconomics. While macroeconomics studies the behavior of economy as a whole, microeconomics focuses on individual businesses and consumers.

Macroeconomics

Macroeconomics involves the study of structure, performance, decision-making and behavior of an aggregate economy. This branch of economics is primarily concerned with broader aspects like aggregate economic growth, unemployment, inflation, fiscal policy and monetary policy, overseas trade and overall standard of living.

Microeconomics

On the flip side, microeconomics involves the study of economic interactions of a particular entity, individual or a business. This branch of economics deals with the demand and supply of goods and services in different markets, consumer behavior, dynamics in individual labour markets, taxes, government legislation and regulations.

What are the Fundamental Principles of Economics?

An American macroeconomist, N. Gregory Mankiw outlined ten fundamental principles of economics to provide a road map to individuals for understanding economic events. Below is the list of the principles highlighted by Mr Mankiw:

- Individuals Respond to Incentives: As people usually make decisions while comparing benefits and costs, they respond to incentives, which can be positive as well as negative.

- Individuals Face Trade-Offs: To make decisions, individuals trade one thing for the another because it is not possible to get everything at the exact same time, given the income levels.

- Rational Individuals Think within the Margin: Economists assume that individuals are rational and think within the margin. This means individuals make decisions comparing marginal costs and marginal benefits.

- Cost of Something is What Individuals Give Up To Get it: This principle deals with the idea of opportunity cost, which indicates what must be given up to get something else.

- Free Trade can Deliver Mutual Benefit: Individuals trading in a free market act in a way that both sides benefit from the trading. In other words, as free trade enables nations to specialise as per their comparative advantage, it makes everyone better off.

- Markets are Generally a Good Way to Arrange Economic Activity: This principle is associated with Mr Adam Smith’s observation of invisible hand guiding the economy. It means that when firms and households interact in an economy with the support of an invisible hand, they generate surpluses for the economy.

- Standard of Living of a Nation Relies on its Production: It means the standard of living of a country goes hand in hand with the goods produced within its domain. A higher standard of living is generally connected with greater production.

- Sometimes, the Government can Enhance Economic Outcomes: As per this principle, the government can sometimes improve economic outcomes, not always. Particularly in case of market failures that happen due to inefficient allocation of resources, government can promote equity and efficiency.

- If Government Prints Too Much Money, Prices Increase: In case the government prints excessive money, the demand for goods and services increases in an economy. This activity triggers a rise in price by firms, stimulating inflation.

- Society Experiences a Trade-Off Between Unemployment and Inflation over Short Run: This principle highlights the relationship between unemployment and inflation. When prices increase in an economy over the short run, suppliers intend to increase the production of products and services. Towards this end, they hire more workers, which lowers the unemployment rate in the short run.

Are Economic Indicators Important to Investors?

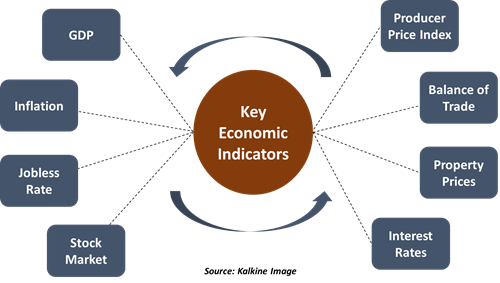

Economic indicators are often being gauged by investors to understand where the economy is heading into. By following economic indicators, investors anticipate market volatility and discover potential trading opportunities. In other words, these indicators support investors in deciding when to purchase or sell their investments.

The below figure summarises some key macroeconomic indicators often being followed by investors to make smart investment decisions:

How is Equity Market Related to Economy?

A rally in the stock market may indicate better micro conditions or macro conditions, and the same is true vice a versa as well. However, there are other factors also that describe the foreplay between economics and equity market. Equity market is a forward-looking event, which is not just driven by economic forces, but also investors’ psychology, geo-political concerns and sectoral trends.

For instance, the COVID-19 crisis saw a weakening of fundamentals at both macro and micro levels, suppressing the market in the beginning. However, post digesting the event consequences, investors' psychology defined an altogether different charter for equity market revival, not resonating with weak economic fundamentals and bearish economic growth trends.