Kalkine has a fully transformed New Avatar.

Company Overview: Alumina Limited invests in bauxite mining, alumina refining and selected aluminum smelting operations. The Company's business undertaking is in the global bauxite, alumina and aluminum industry, which it conducts principally through bauxite mining and alumina refining, with some minor alumina-based chemicals businesses, aluminum smelting and the marketing of those products. The Company conducts these business activities through its joint venture, Alcoa World Alumina & Chemicals (AWAC). AWAC is a producer of alumina and miner of bauxite. AWAC operates mines integrated with alumina refineries in Western Australia and Brazil. Other refineries operate in Spain and Texas in the United States. AWAC's bauxite deposits are extracted by open cast mining from strata, typically 4 to 6 meters thick under a shallow covering of topsoil and vegetation. The topsoil is removed and stored for later use in restoration of the forest. AWAC supplies bauxite ore to Pinjarra and Kwinana Refineries.

.png)

AWC Details

Long-term Growth Potential Intact: Alumina Limited (ASX: AWC) is a mid-cap resource company with the market capitalisation of circa $6.59 Bn as of 11 September 2019. It is one of Australia’s top 100 companies, delivering decent returns, consistent performance and ongoing growth. The principal activities revolve around 40% interest in series of the operating entities forming Alcoa World Alumina and Chemicals (or AWAC). AWAC has interests in the bauxite mining, alumina refining and aluminium smelting. Recently, the company declared its results for the half-year ended 30 June 2019 in which it reported a statutory net profit after tax of US$210.9 million. Additionally, the company has declared a fully franked interim dividend of 4.4 US cents per share, which will be paid on 12 September 2019. As per the company’s CEO named Mike Ferraro, the tight Western world alumina market conditions of 2018 have been subsided in 1H FY19 as curtailed supply came back on stream and new refineries ramped up. Against the backdrop, AWAC has reduced production costs which have contributed to the cash margins in the half of more than $150 per tonne even though the alumina prices were lower. In the month of June 2019, Alumina Limited has rolled over a tranche of bank facility that was due to mature in the month of July 2020 and established a new tranche under the same facility. As a result, Alumina Limited has a US$350 million syndicated bank facility with tranches maturing in the month of October 2022 (US$100 million), July 2023 (US$150 million), and July 2024 (US$100 million). The general and administrative expenses of 1H FY19, excluding the benefit of the weaker AUD, were largely in line with 1H FY18. Alumina Limited’s net debt as at June 30, 2019, stood at $54.7 million and gearing came in at 2.7%.

The company’s cash from operating activities has witnessed a CAGR growth of 145.0% in the time frame of FY15- FY18 and, therefore, it can be said that the company has decent operational capabilities. There are expectations that the company’s capabilities to garner revenues and carrying out operations might help it in delivering decent performance over the long-term.

.png)

Alumina Limited Half-Year Results (IFRS) (Source: Company Reports)

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in Alumina Limited:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

Higher RoE Than Industry Median: Alumina Limited’s return on equity (or RoE) in 1H FY19 stood at 10.3%, which is higher than the industry median of 6.4% and, thus, it can be said that the company has been delivering decent returns to its shareholders which might attract the attention of the market players moving forward. At the end of 1H FY19, the company has Debt/Equity ratio of 0.05x which is lower than the industry median of 0.08x and, therefore, it can be said that the company’s balance sheet is less leveraged as compared to the broader industry and it can be said that AWC’s balance sheet is more stable. Generally, lower debt on the balance sheet is considered positive as it helps the company in focusing on its long-term growth objectives.

.png)

Key Metrics (Source: Thomson Reuters)

Announcement By Alcoa Corporation About New Operating Model: Alcoa Corporation, which is a global leader in bauxite, alumina, and aluminum products, recently made an announcement that, effective November 1, 2019, it would be implementing the new operating model that would result in the leaner, more integrated, operator-centric organization which accelerates the company’s strategic priorities. Alcoa would be eliminating the business unit structure and consolidate sales, procurement and other commercial capabilities at the enterprise level. Under a new operating model, the Alcoa Executive Team would be streamlined from 12 to 7 direct reports to the CEO. The new structure would be reducing overhead, promote operational and commercial excellence, increase the connectivity between the company’s plants and leadership, ensure continued focus towards safety as the highest priority, and position Alcoa for sustainable profitability.

In the release, it was mentioned that Leigh Ann Fisher, who is presently Executive Vice President and Chief Administrative Officer, has been named as the Executive Vice President and Chief Human Resources Officer. Fisher would be focusing exclusively towards people, including talent management and recruitment, compensation and benefits, training & development and the industrial relations. Jeffrey Heeter, Executive Vice President, General Counsel and Secretary, would continue to be accountable for the legal, corporate secretary, ethics and compliance and global security functions. Benjamin Kahrs, who is a Senior Vice President and Manufacturing Excellence and R&D, has been named as the Executive Vice President and Chief Innovation Officer.

It was also added that Michelle O’Neill, who is presently the Senior Vice President, Global Government Affairs and Sustainability, has been named as the Executive Vice President and Chief External Affairs Officer. William F. Oplinger, Executive Vice President and Chief Financial Officer, would continue to be responsible for finance functions and transformation assets, with added responsibility for corporate development. Timothy Reyes, who is presently Executive Vice President and President, Aluminum, has been named as the Executive Vice President and Chief Commercial Officer. The release also stated that John Slaven, who is presently the Executive Vice President and Chief Strategy Officer, has been named as the Executive Vice President and Chief Operations Officer.

Review of AWAC Operations: In 1H FY19, AWAC’s earnings and cash flows had been affected by the lower alumina prices. However, AWAC’s low position with respect to the cost curve and operational stability, continue to support the robust cash flows and profitability even in the surplus alumina market. AWAC operated mines increased production by 4% which is because of production creep at Huntly mine as well as a capacity increase to 6.5 million bone dry tonnes (BDT) per annum at Juruti mine that was completed in 2H FY18.

.png)

Diagram of AWAC Value Chain (Source: Company Reports)

Property, Plant and Equipment Increased in AWAC’s Balance Sheet: The following picture provides a brief overview of AWAC’s balance sheet and the movement in value of the assets and liabilities includes effect of the weaker AUS against the USD as at June 30, 2019. The rise in the property, plant and equipment was mainly because of the Pinjarra press filtration construction, other capital projects, and capitalisation of the operating leases following the adoption of new accounting standard.

.png)

AWAC Balance Sheet (US GAAP) (Source: Company Reports)

There was an increase in other assets mainly because of the changes in fair value of the derivative assets associated with the Portland’s hedging arrangements.

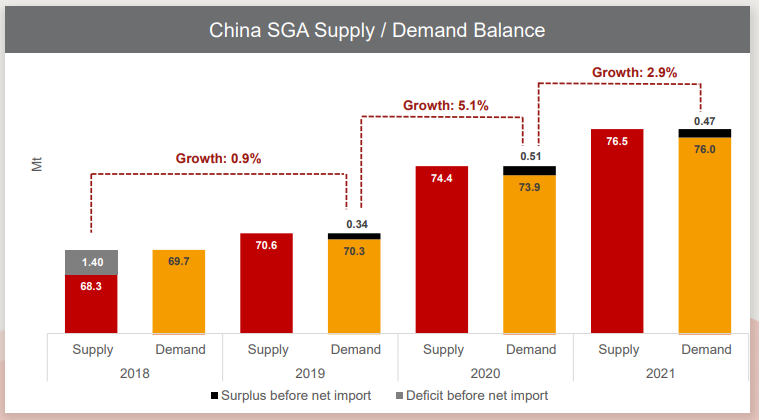

What to Expect Moving Forward: During 1H FY19, alumina price indices ranged in the ambit of $418 and $321 per tonne and averaged $375. This compares to 2018 range of $357 and $710 per tonne and an average of around $473. It was stated that the lower prices were because of supply and demand factors. As was anticipated, the full alumina production resumed at 50% curtailed Alunorte refinery in Brazil, production at Friguia refinery in Guinea continued to ramp-up after it re-started in the last year, and Al Taweelah greenfields refinery in the United Arab Emirates produced the first alumina in 2019. The following image has been extracted from the half-yearly result presentation:

China’s Forecast Production (Source: Company Reports)

It was mentioned that, towards the end of 2019, there are expectations about Winter heating season related cuts to alumina and aluminium production, although, they are not anticipated to be significant, mainly because of the curtailments resulting from lower prices and forced closures because of environmental compliance audits. Whilst a modest alumina surplus is forecast in China this year, over the medium to longer-term there are expectations that China would be broadly balanced with respect to alumina, on the basis of the Chinese Government’s supply-side reform focus and its environmental and cleaner energy goals.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

Stock Recommendation: The stock of Alumina Limited has fallen 10.20% in the span of previous 6 months, while in the time frame of previous one month, the stock has delivered the return of 1.33%. Currently, the stock is trading slightly below the average of 52 weeks low and high levels of $2.070 to $3.20 with reasonable PE multiple of 8.08x, indicating a decent opportunity for accumulation. On the other hand, the company’s total revenues have witnessed an improvement between FY14- FY18 and, thus, it can be said that AWC is possessing decent capabilities to generate revenues which might help it in achieving long-term growth potential. Hence, in view of aforesaid facts coupled with decent outlook and current trading levels, we give a “Buy” recommendation on the stock at the current market price of A$2.390 per share (up 4.367% on 11 September 2019), and expect single-digit growth in the next 12 months backed by decent financials, operational stability, and adoption of new operating model by Alcoa Corporation.

AWC Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...