Company Overview - Austal Limited (Austal) is engaged in design, manufacture and support of high performance aluminum vessels. The Company operates in four segments: Henderson Shipyard Operations (HSO), USA Operations, Service & Systems Operations and Philippines Shipyard Operations (PSO). The HSO business manufactures high performance aluminum defense vessels for markets worldwide, excluding the United States. The USA manufactures high performance aluminum defense vessels for the United States Navy. The Service business provides training and on-going support and maintenance for high performance vessels and includes the chartering of a vessel to the United States Navy’s Military Sealift Command. The PSO business manufactures high performance aluminum commercial vessels for markets worldwide, excluding the United States. In January 2014, Austal Ltd sold its land and infrastructure at its former satellite service base at Henderson.

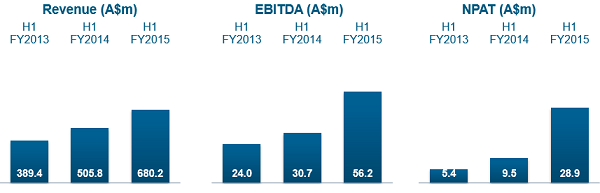

Analysis - Austal Limited (ASB), the Company engaged in designing, manufacturing and supporting high performance aluminum vessels, reported net profit after tax (NPAT) of $28.947 million for the half year ended 31 December 2014 as compared to $9.507 million of the prior corresponding period. 57% reduction in net interest expense from $4.935 million in 1H of FY14 to $2.125 million in 1H of FY15 helped achieve the increase in NPAT. Balance sheet strength improved given the reduction in net debt. At the end of 1H of FY15, ASB reported a cash balance of $142 million with gross debt of $138 million. A surge in revenue for operation segments also contributed to the profit result. The revenue in 1H of FY15 was reported to be $680.186 million indicating an increase of 34% from prior corresponding period. The profit before tax for 1H of FY15 was $42.912 million as opposed to $13.804 million of corresponding period in previous year. The market capitalization of the Company is about $544.08 million.

Revenue and Earnings Growth (Source – Company Reports)

Productivity improvements in Cape Class Patrol Boat Program in Australia, lower administration costs owing to less dependence on expatriate employees in Philippines business, better efficiencies owing to integration of Henderson shipbuilding and support activities onto one site and non cash unrealized foreign exchange gains helped in improving the earnings before interest, tax, depreciation and amortization (EBITDA). Primarily, the Company reported EBITDA of $56.164 million as opposed to $30.731 million of 1H of FY14. Mark to market of an intercompany loan to Austal USA led to a non-cash contribution to EBIT of $11.3 million. The Company reported underlying EBIT of $33.7 million in 1H of FY15, which is a significant improvement on the prior corresponding period.

From segment-wise breakdown, Australian operations contributed majorly to EBIT. The business led to a robust increase in EBIT from $3.0 million in the prior corresponding period to $14.5 million in 1H of FY15. The revenue rose 60.8% to $98.0 million over prior corresponding period with an increase in margins supported by a surge in utilisation with labor efficiency in view of the construction of the Patrol Boats. The Cape Class patrol boat contract is outstanding for completion in August 2015. Construction of two 72 m High Speed Support Vessels (HSSV) has been reportedly commenced for the Royal Navy of Oman with regards to a U$124.9 million contract. However, EBIT contribution was below par expectations from the US division owing to the delay in delivery of Littoral Combat Ship (LCS6) and expenditure to earn future sustainment work for the LCS and Joint High Speed Vessel (JHSV) programs. The revenue rose 19.2% to $498.3 million in comparison to prior corresponding year although margins dropped 98bps to 5.5% with challenges on LCS6. For Philippines, there has been a 19.6% drop reported in revenue on the prior corresponding period to $14.9 million. However, EBIT rose to $1.9 million from $0.3 million reported in 1H of FY14. ASB stated about the customization of Hull 270 for $6 million before delivery to Condor Ferries. Further, construction of two 45 metre high speed catamaran ferries with regards to a $30 million contract from Abu Dhabi National Oil Company has been reported. The delivery is expected in CY15.

Progress across Business (Source – Company Reports)

Effect from the sale of Hull 270 that contributed $54.1 million to operating cash flow is to be understood. The operating cash flow reduces to $64m if the aforementioned is left out, still indicating a 45% increase over 1H of FY14. The Company conveyed that in 1H15 operating cash flow of $118.0 million was 170% up on the prior corresponding period resulting in $84.2 million enhancement in the gearing position. The Company thus reported a net cash position of $15.6 million with declaration of dividend ever since 2H of FY11. Particularly, ASB declared a fully franked interim dividend of 1 cent per share in comparison to zero dividend in the prior corresponding period. The Company indicated some reversion of cash flow expected in 2H of FY15 with a possible net debt position of about $35 million at June 2015. Further, as the shipbuilding business is a working capital intensive kind of a business, cash levels are expected to be volatile.

Australia_High Speed Support Vessels (Source – Company Reports)

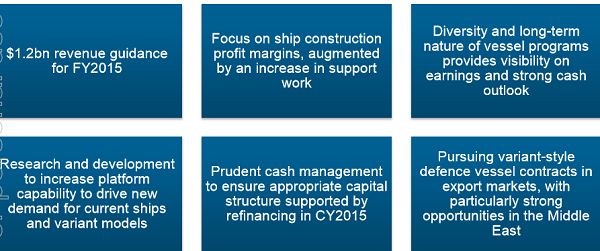

ASB restated its guidance for FY15 revenue of about $1.2 billion that appears to be achievable given the internal efforts and the expected boost from USD in 2H of FY15. The Company has a noteworthy pipeline of work amounting to about $2.6 billion which is said to be contracted in the US out to 2018. A contractual extension is expected to 2019 and ahead. ASB can in due course build about 15% of the US Navy fleet. In fact, the US is experimenting with variations of the JHSV. Extension of LCS program to 52 vessels is also predicted. At the moment, at least one more LCS vessel is expected to be funded in first quarter of CY15. Therefore, the Company mostly generates its earnings from US naval contracts with supplementary advantages emanating from commercial vessel construction and marine services. We also make a note of the fact that ASB share price has been on the forefront beating the small industrial index by about 30% since the FY14 result was released in August 2014.

Outlook (Source – Company Reports)

The attributes pertaining to lessening of debt with a focus on working capital management, and then paying of dividends speak of a good potential. It is also expected that the Company is capable of delivering higher EBIT margins in FY16 in view of productivity gains and benefits from the LCS and JHSV programs. Funding for LCS22 and other sustainment contract awards can add to the results in near term. The Company is poised to undertake opportunities to grow order book along with securing long-term revenue. With opportunities continually explored in the US and Australia, ASB is targeting markets in Middle East, Europe and Asia Pacific with support vessels, commercial vessels and work boats, as appropriate. Of course, the risks that one needs to be wary of include any currency movements, changing economic environment, operational risks, further deferrals to the delivery of LCS6, and any bottleneck for order book replenishment.

ASB Daily Chart (Source - Thomson Reuters)

Based on the foregoing, we put a BUY recommendation for this stock at the current price of $1.505.

Please wait processing your request...

Please wait processing your request...