Company Overview - Bank of Queensland Limited (BOQ) is an Australia-based financial company. The Company's segments include Banking and Insurance. The Banking segment includes retail banking, commercial, personal, small business loans, equipment, debtor finance, treasury, savings and transaction accounts. The Insurance segment includes customer credit insurance, life insurance, accidental death insurance, funeral insurance and motor vehicle gap insurance. The Company's online banking services include Internet banking, mobile banking, BOQ property application, online applications and BOQ money. The Company's personal banking offering includes everyday banking, savings and investment, credit cards, personal loans, home loans, insurance, international services, investing, private bank and account switching among others. Its business banking includes transaction accounts, investment accounts, statutory trust accounts, investment trust accounts, business loans, cash flow finance and equipment finance.

.png)

BOQ Details

Improved FY 16 Financial Performance despite the challenging environment:Bank of Queensland Limited (ASX: BOQ) reported a 6% growth in the statutory net profit after tax to $338 million in the fiscal year of 2016 and a 1% growth in the cash earnings after tax to $360 million for the year. BOQ has posted increased cash earnings after tax for the fourth consecutive year, despite facing a volatile environment of low interest rates and intense competition. The growth in the cash earnings is due to the continuing focus on the niche businesses, further improvement in the loan impairment expense and has included the one-off $15 million investment to refine BOQ’s operating model. On the other hand, the basic earnings per share fell 2% to 95.6 cents in fiscal year of 2016 and the return on equity has decreased 40 basis points to 10.3 per cent.

.png)

Fiscal year of 2016 performance highlights (Source: Company Reports)

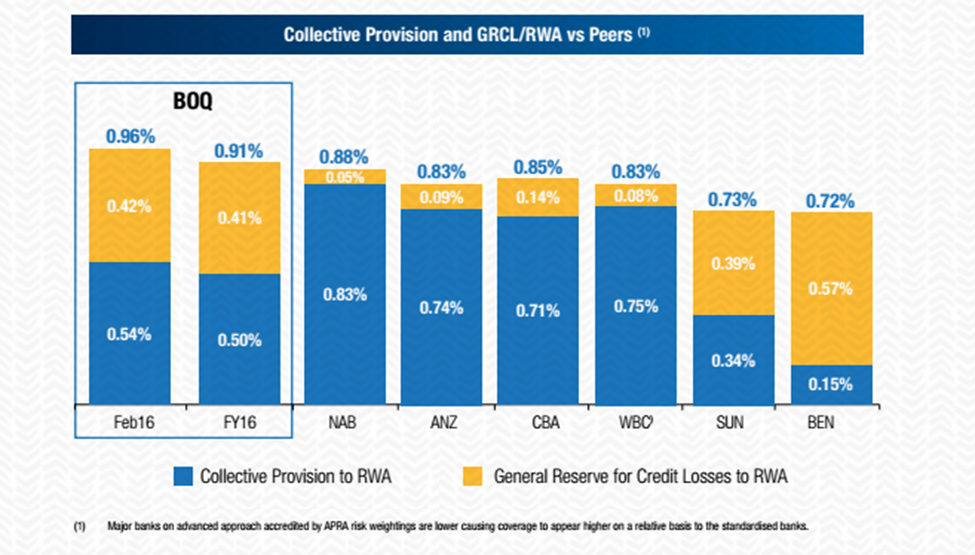

Strategic Steps taken to manage growth: The environment of lower interest rates in Australia for longer time led to lower rate of return on capital and low cost deposits. Further, the widening of spreads in term deposits and other liabilities has also led to competition for deposits and pricing for new lending. To combat the situation, BOQ took strategic steps and slowed the asset growth in the second half of FY 16, after the strong period of growth in the first half of FY 16. Additionally, BOQ has focused more on the deposit gathering for the second half of 2016 and growing the niche segments to deliver superior returns. As a result, the total lending grew 5% for fiscal year of 2016 to $2.2 billion. Bank of Queensland deposit to loan ratio grew from 66 per cent to 68 per cent. The bank’s coverage fell 4 basis points over the half as collective provisions fell by $8 million (5%).

Collective provisions and GRCL to RWA against the current peer levels (Source: Company Reports)

Ongoing focus on cost reduction:Bank of Queensland is focusing to control costs for fiscal year of 2016 and has kept the underlying expense growth to 4% and continued to invest in the business. BOQ had announced the one-off $15 million restructuring cost in February 2016 to deliver above its payback target in a year. The 12-month payback is ahead of the schedule.

Moreover, BOQ has taken a number of further efficiency initiatives underway, such as reducing duplicate processes across the business by creating centralized hubs to post a more efficient operating structure. This would also generate a further expense savings in the years ahead. In addition, Bank of Queensland forecasts to keep the underlying expense growth to 1 per cent in 2017, and continues to build the multi-channel and niche segment market strategy.

Investment Payback, cost control is on track (Source: Company Reports)

Niche specialist businesses delivered strong results:In fiscal year of 2016, BOQ’s niche businesses, including BOQ Specialist and BOQ Finance contributed strongly for the increased results. BOQ Specialist has posted solid sustainable returns and commercial loan grew 13% over the year, while maintaining good margins and low loss rates. Moreover, the mortgage portfolio grew $1.5 billion of growth over the year. Additionally, BOQ Finance gave good returns with the asset growth of 3 per cent in a low growth and the challenging market, and the loss rates moved in line with the company’s expectations. Further there were growth in other niche segments like the growth in the other Business Banking niche segments was above system. Other niche business segments also gave positive results from the retirement living, hospitality and agribusiness. In addition, BOQ’s Virgin Money has launched its Reward Me home loan product and had received $100 million worth of loan applications since the launch in May 2016.

BOQ extended their Business Banking services to Hospitality & Tourism, Agribusiness, Retirement Living, Medical & Dental, and Franchising while maintaining credit quality across the portfolio. The bank’s digitized mortgage origination platform implementation helped 30% of mortgage applications leading to better service for customers, declining operational risk while enhance lender productivity. Similarly, the group’s Commercial Lending Origination Environment (‘CLOE’) would enhance SME / Commercial portfolio.

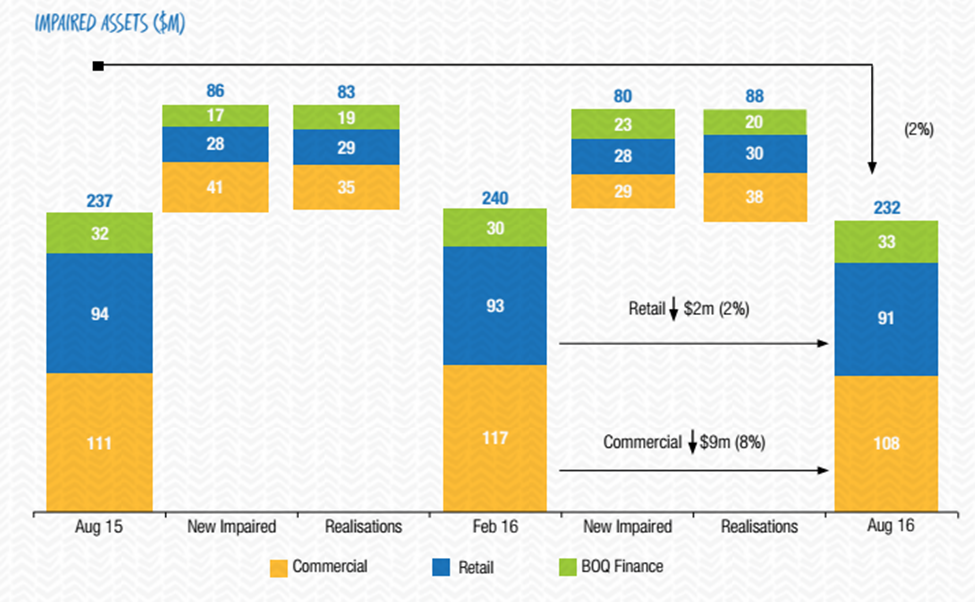

Strong asset quality across all portfolios:Bank of Queensland enhanced asset quality across all the portfolios in fiscal year of 2016 as the loan impairment expense reduced 9 per cent to $67 million, and the impaired assets declined by 2 per cent to $232 million. The Commercial portfolio performance in second half of 2016 was good and no new impaired assets was less than $5m and the retail portfolio benefitted from the mix impact of new BOQ Specialist housing loans. Moreover, BOQ has diversified the portfolio away from Queensland. BOQ now comprises of 48 per cent of total loans, which is down from 56 per cent from three years ago, and the broker channel and BOQ Specialist contributed the diversification. Bank of Queensland has taken the disciplined approach for the risk management since 2012. The bank was able to cut their Loan impairment expense by 9% to $67 million during the year, which is a control of 2bps to 16bps of gross loans and advances. For the second half, the group improved further to 14bps of gross loans and advances.

The bank delivered a Lending growth of 5% or $2.2 billion during the 2016 fiscal year, driven by their strategic shift to preserve margin and target deposit acquisition through retail channels. Lending growth was totally funded by the 8% growth in customer deposits, leading to a 2% rise to the deposit to loan ratio to 68%.

Focus on impaired assets control (Source: Company Reports)

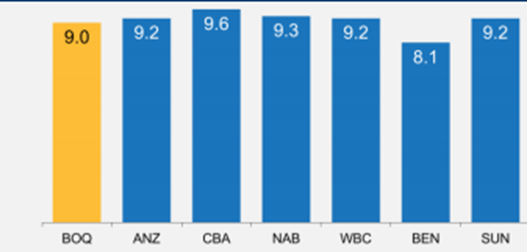

Strengthening the capital position:Bank of Queensland has further strengthened its capital ratios in fiscal year of 2016 as the CET1 ratio grew 9 basis points to 9 per cent. BOQ’s capital position compares well against peers, particularly given the company’s more conservative risk weightings. Moreover, the Basel 4 should level the playing field further and there is potential upside in SME lending.

In addition, Bank of Queensland has made good progress towards advanced accreditation if the size of the prize warrants accelerating the step. Bank of Queensland has been looking forward in getting clarity on a number of global regulatory reforms later this calendar year, and is optimistic that changes will improve BOQ’s competitive position.

Peer CET1 Comparison (Source: Company Reports)

Priorities for fiscal year of 2017: Bank of Queensland is looking for the expansion of mortgage aggregators for Virgin Money, enhance the digital customer experience and the ongoing branch network optimization. Additionally, BOQ will optimize the deposit pricing using data analytics, develop the specialist niche capability in franchising and hospitality, and focusing the investment in high margin businesses.

In addition, Bank of Queensland would finish the roll out of new origination & leasing systems, deliver the return on investment in efficiency programs and implementing the centralized mortgage hub. Overall, Bank of Queensland is focusing on the niche segments for the outperformance of sector EPS growth.

Solid dividend yield:The shares of Bank of Queensland fell over 4.8% in the last four weeks (as of November 11, 2016) due to volatile environment. On the other hand, the stock fall placed them at attractive levels which is trading at a good dividend yield and a cheap P/E. Moreover, BOQ’s focus on personalized customer experience, control over impairment charges and focus on asset quality could further drive the stock higher.

The Bank is positioning itself to fight competition while continues the cost control efforts. The bank is conducting its AGM on November 30, 2016. We give a “Buy” recommendation on the stock at the current price of $10.78

.PNG)

BOQ Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...