Kalkine has a fully transformed New Avatar.

Company Overview: Base Resources Limited (ASX: BSE) is an Australian-based, African-focused mineral sands producer with a high-quality asset portfolio. Base Resources Limited was founded in 2008 to enrich its people and shareholders through the creative development of mineral resources. The company operates the established Kwale Operation in Kenya. The company is also engaged with a world-class mineral sands development project in the Toliara Project in Madagascar. The company has a strong history of excellence in safety and operations, environmental stewardship and community engagement.

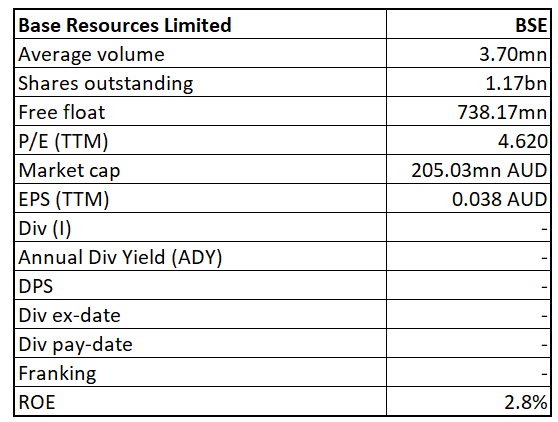

BSE Details

(15).png)

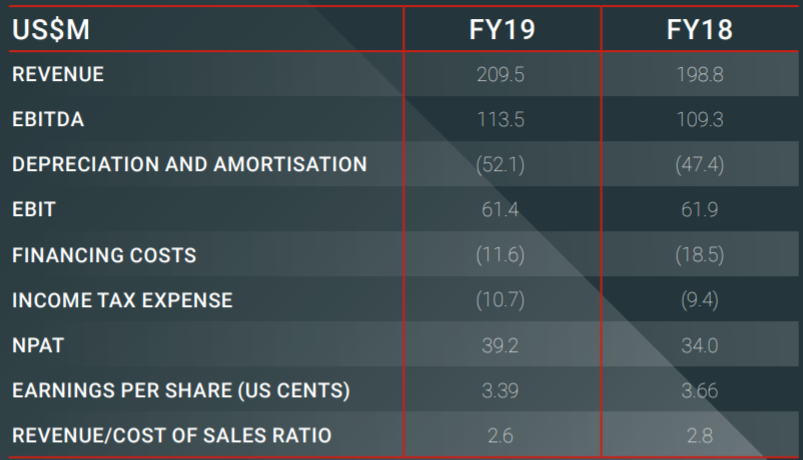

Robust Financial Platform: Base Resources Limited (ASX: BSE) is an Australian-based, African-focused, mineral sands producer, primarily involved in the operation of the Kwale Mineral Sands Operation (Kwale Operation) in Kenya and the development of the Toliara Project in Madagascar. With its high-quality asset portfolio and a track record of excellence in safety and operations, community engagement and environmental stewardship, the company seeks to build a truly unique mineral sands company. Over the last few years, the company saw significant improvement in its top-line as well as bottom-line. From 2016-2019, the company’s total revenue and gross profit have increased at a CAGR of 19.42% and 44.41%, respectively. Over the same period, the company’s net income has also improved significantly, rising from the net loss of $15.2 million in 2016 to $39.2 million in FY19. (27).png)

Financial Overview (Source: Refinitiv, Thomson Reuters)

Benefitting from the consistent production at Kwale Operations, the company has established a robust financial platform from which it intends to grow the business and create a truly unique mineral sands company. Moving forward, the company is focused on Kwale mine life extension to maximise value creation for employees, the community, the nation of Kenya and shareholders. Even during the Covid-19 situation, the operations at Kwale Operations are continuing uninterrupted, demonstrating the resilience of the company’s operations. As a result of this, the company has maintained its FY20 production guidance levels for Rutile, Ilmenite and Zircon, despite the current challenging environment.

FY19 Performance Highlights: In the financial year 2019 or FY19, the company saw a strong operational performance and a healthy pricing environment, which allowed the company to achieve record revenue of US$209.5 million, up 5% on the previous year. For FY19, the company recorded a net profit after tax of US$39.2 million, up 15% on last year. In FY19, the company produced 402,698 tonnes of ilmenite, 92,393 tonnes of rutile and 31,941 tonnes of zircon. Over the year, the company’s net tangible assets increased to US$204.7 million, from US$184.10 million in 2018.

During the year, the company made significant progress in the development of the Toliara Project in Madagascar. Following the acquisition of the project in January 2018, an accelerated study phase saw the release of the pre-feasibility study (PFS) in March 2019. With a NPV10 of US$671 million, annual free cash flow generation of US$133 million and a sector leading average revenue to cost ratio of 3.06, the PFS confirmed the company’s view that the Toliara Project is a world-class mineral sands development opportunity.

FY19 Results Snapshot (Source: Company Reports)

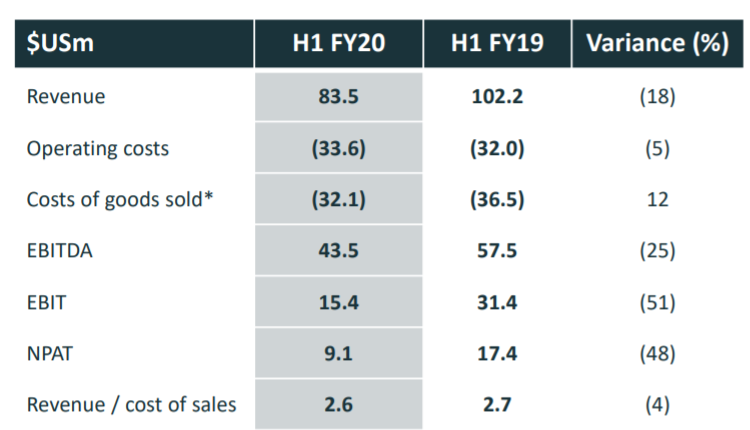

H1FY20 Performance Highlights: For the six-month period ended 31 December 2019 or H1FY20, the company reported production of 36,201 tonnes of rutile, 165,214 tonnes of ilmenite and 14,904 tonnes of zircon. The production was impacted by the lower grade of the South Dune orebody and the ramp-up of operations. Over the half-year period, the company saw a continued strengthening of rutile and ilmenite prices.

During the period, the company progressed with the Kwale Operations mine life extension opportunities and completed the definitive feasibility study (DFS) for Toliara Project and concluded that Toliara Project is a world-class mineral sands project.

The company’s sales revenue decreased by 18% to US$83.5 million in H1FY20, due to lower production and timing of rutile shipments. Operating costs over the half-year period were relatively higher in H1FY20, compared to pcp, due to higher power consumption associated with increased pumping distance from South Dune. Over the period, the company reported revenue to cash cost ratio of 2.6:1.

H1FY20 Results Snapshot (Source: Company Reports)

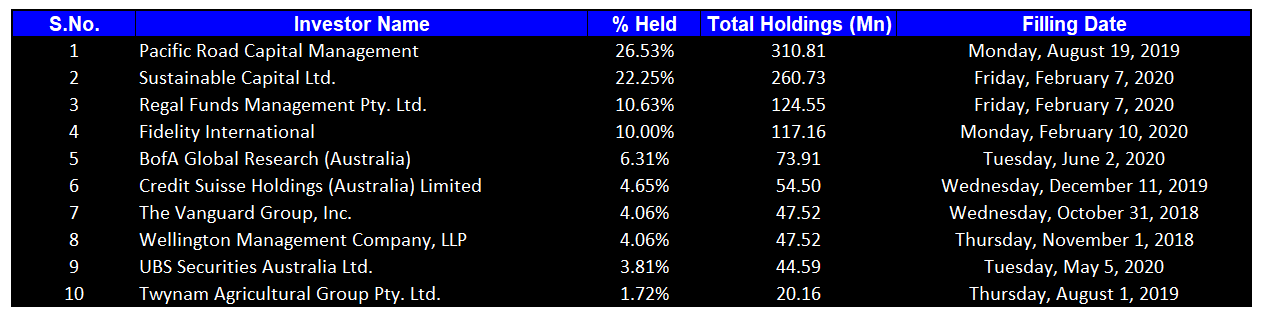

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 94.01% of the total shareholding. Pacific Road Capital Management and Sustainable Capital Ltd. hold maximum interest in the company at 26.53% and 22.25%, respectively.

Top 10 Shareholders (Source: Refinitiv, Thomson Reuters)

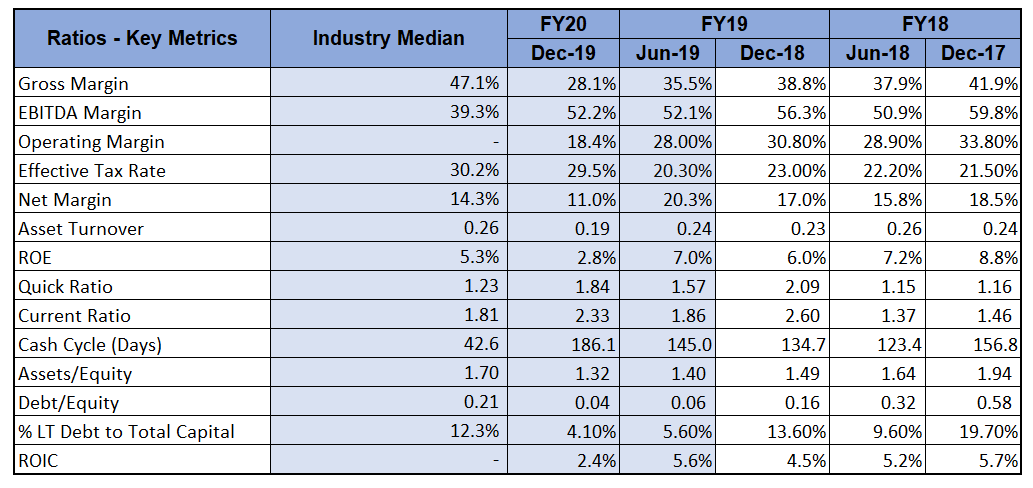

A Quick look at Key Margins: For H1FY20, the company’s gross margin and net margin stood at 28.1% and 11%, respectively. The company’s current ratio stood at 2.33x, higher than the industry median of 1.81x, demonstrating that the company is well-equipped to pay its short-term obligations. The company’s asset to Equity ratio stood at 1.32x, lower than the industry median of 1.7x.

Key Metrics (Source: Refinitiv, Thomson Reuters)

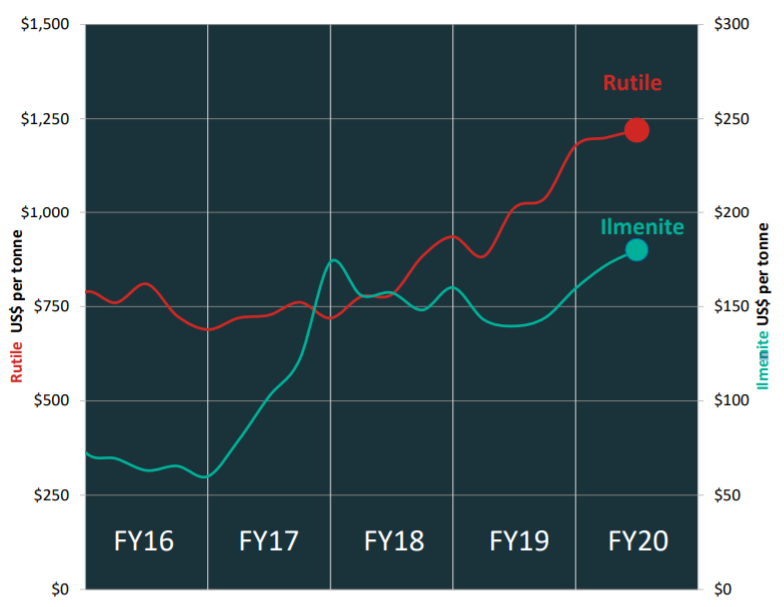

Continued Strengthening of Rutile and Ilmenite Prices: During FY19 as well as H1FY20, the company witnessed improvement in rutile and ilment prices, mainly due to strong global demand and restricted supply. As a result of this, the medium and long-term dynamics for the company’s products were encouraging.

Price Chart for Rutile and Ilmenite (Source: Company Reports)

March Quarter Highlights: During the March quarter, the company’s reported higher production from the prior quarter across all products. In the March quarter, the company produced 105,035 tonnes of Ilmenite, 23,683 tonnes of Rutile and 9,163 tonnes of zircon.

Despite the seasonal factors and the Covid-19 situation, the demand for all the products during the March quarter was firm and was at normal levels with regular orders received from their customers. Over the quarter, the company sold 87,819 tonnes of Ilmenite, 25,280 tonnes of Rutile and 7,377 tonnes of Zircon. As at 31 March 2020, the company has cash and cash equivalents of US$119.4 million and Revolving Credit Facility drawn to US$75.0 million.

March Quarter Production Summary (Source: Company Reports)

UBS Group AG Becoming a Substantial Holder: Recently, UBS Group AG and its related bodies corporate became a substantial holder of the company by holding 65,591,302 ordinary shares in the company. UBS Group AG now holds 5.60% voting power in the company.

Covid-19 Update: In response to Covid-19, the company has implemented several health and safety procedures to minimise the risk of virus to personnel and surrounding communities. The company’s operations at Kenya continued uninterrupted during this period. Although the company has maintained its FY2020 production guidance, the company has warned that due to the inherent uncertainties associated with the COVID-19 pandemic, a halt to, or curtailment of, operations at some point in the future is possible.

What to expect: The medium, as well as the long-term dynamics for the company’s products, continue to be encouraging with strong global demand and restricted supply. In FY19 and H1FY20, these market conditions supported steady price improvement for rutile and ilmenite. In the longer term, structural supply shortfalls require new projects to be developed in the coming years and present exciting strategic opportunities for Base Resources as an established and experienced mineral sands producer.

As a result of improved separation efficiency and higher recoveries for all products in the mineral separation plant, the company recently increased the FY20 production guidance range. As per the updated guidance range, the company expects FY20 Rutile production to be in the range of 75,000 to 81,000 tonnes, Ilmenite production to be between 335,000 to 355,000 tonnes and the production for Zircon to be in between 29,000 to 32,000 tonnes.

FY20 Production Guidance (Source: Company Reports)

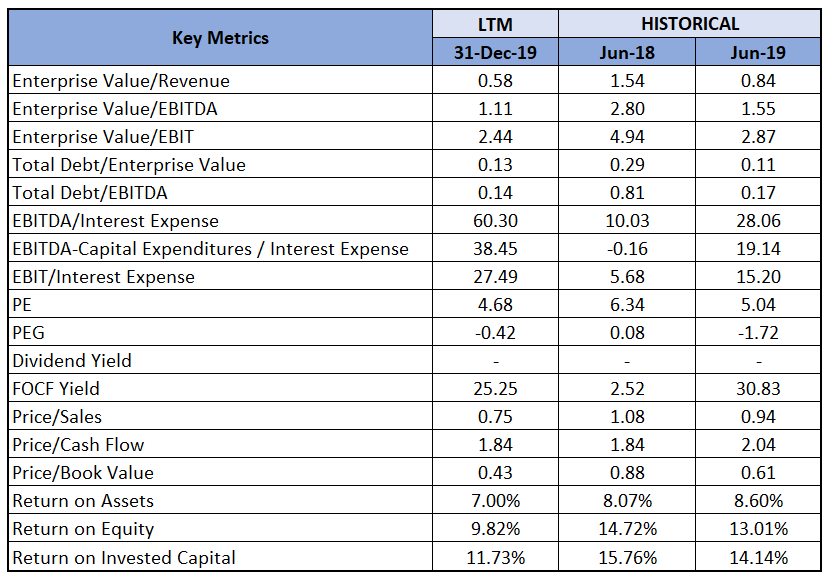

Key Valuation Metrics (Source: Refinitiv, Thomson Reuters)

Valuation Methodology: P/E Multiple Based Relative Valuation (Illustrative).png)

P/E Multiple Based Relative Valuation Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Over the past six months, the stock of BSE has declined by 23.91% on ASX, and is inclined towards its 52-week low price, offering a decent opportunity for accumulation. As at 31 March 2020, the company was in a sound financial position with a net cash position of US$44.4 million which includes cash and cash equivalents of US$119.4 million and Revolving Credit Facility drawn to US$75.0 million. We have valued the stock using the price to earnings multiple based illustrative relative valuation method and have arrived at a target price with lower double-digit upside (in % terms). For the purpose, we have taken peers like Western Areas Ltd (ASX: WSA), Jupiter Mines Ltd (ASX: JMS) and Lynas Corporation Ltd (ASX: LYC). Considering the ongoing sound demand from customers, the company’s resilient performance amid Covid-19, its improved FY20 guidance, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $0.180, up by 2.857% on 10 June 2020.

BSE Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...