Company Overview - Beach Energy Limited (Beach) is an Australia-based company. The Company is engaged in oil and gas exploration, development and production and investment in the resources industry. As of June 30, 2012, the Company’s oil and gas reserves of 92.8 million barrels of oil equivalent and contigent resources of 466.6 million barrels of oil equivalent. As of June 30, 2012, Beach held interests in more than 300 exploration and production tenements in Australia, the United States, Egypt, Tanzania and Papua New Guinea. During the year ended June 30, 2012, the drilling program consisted of 89 wells, 83 of which were drilled in the Cooper/Eromanga Basins. The Company's subsidiaries include Beach Petroleum (NZ) Pty Ltd, Beach Oil and Gas Pty Ltd, Beach Production Services Pty Ltd, Beach Petroleum Pty Ltd and Beach Petroleum (Cooper Basin) Pty Ltd. In June 2013, Beach Energy Ltd raised its stake to 46.9% from 42% by acquiring a further 4.9% stake in the ATP 855.

Analysis – We note that FY15 production guidance is down (on FY14) and we suggest BPT has a tendency to be conservative in its forecasts and outlook commentary. We note the company has indicated there could be upside potential to guidance. The Western Flank oil play continues to deliver strong production performance, which we suggest could drive upside to production gui dance. A strong FY14 but eyes now focus on FY15 where we see upside potential above guidance and the next phase of the extensive unconventional drilling and evaluation program.

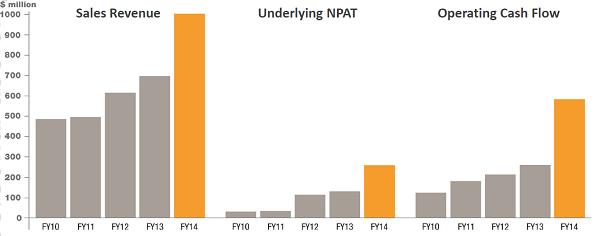

Sales Revenue + NPAT (Source - Company Reports)

Sales Revenue + NPAT (Source - Company Reports)

BPT released record results on 25

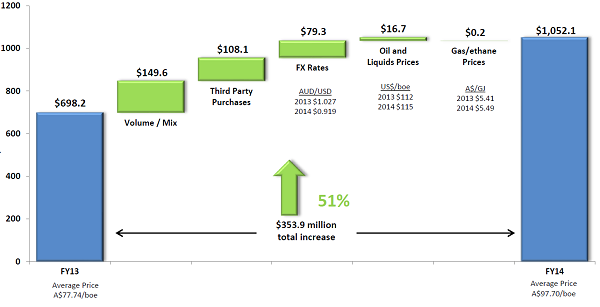

th August for FY2014 booking underlying NPAT of $259m and up 84% on FY2013 of $141m. NPAT was 20% down to $102m after non cash impairments of $162m, predominantly for the Egyptian exploration assets. The strong underlying result was driven by record production of 9.6mmboe and sales volumes of 10.8mmboe, up 20% on FY13 of 9.0 mmboe and record sales revenue of $1,052m, up 51% on FY13 of $698m. BPT finished the period in a strong position with cash of $411m and $300m in undrawn debt. BPT released its updated reserves with 1P, 2P and 3P reserves all lower at 33.4mmboe, 85.6mmboe and 181.7mmboe but increased 2C contingent resources on the back of drilling and completion activity at its Nappamerri Trough Natural Gas (NTNG) project.

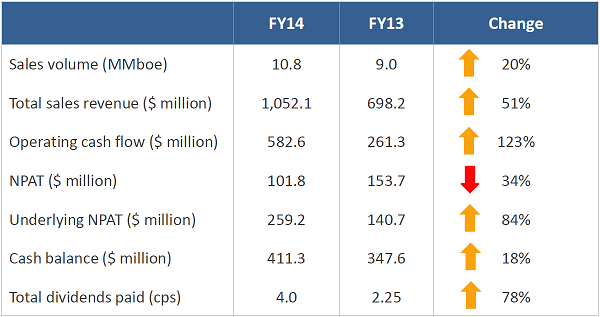

Financial Highlights (Source - Company Reports)

Financial Highlights (Source - Company Reports)

The strong performance was underpinned by the Western Flank which averaged over 10,000bopd through FY14 and maintaining sustained rates will be a key driver in the short term. BPT participated in the drilling of 122 wells during the year with a success rate of 85%. Key exploration highlights included Stunsail-1, Pennington North-1 and encouraging results from the early stage onshore Otway drilling program.

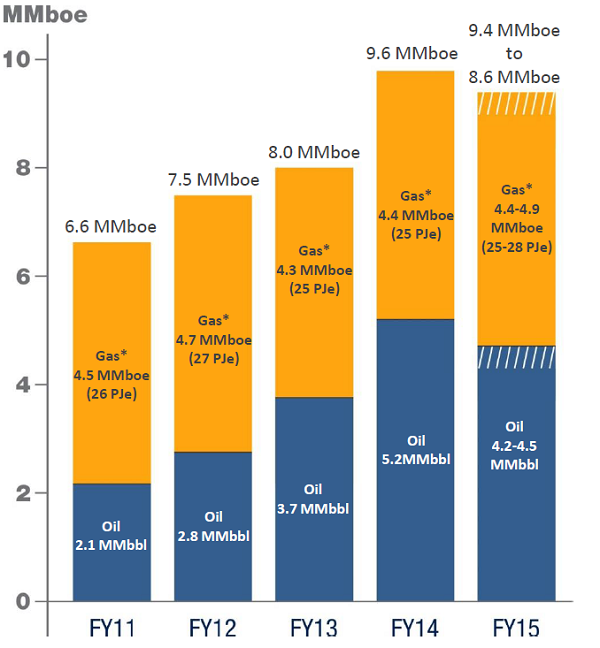

Actual Production + Forecast (Source - Company Reports)

Actual Production + Forecast (Source - Company Reports)

The strong performance was reflected in the operating cash flow of $583m, up 123% on FY13. BPT finished the period in a strong position with cash of $411m to fund forecast capex through to the end of FY16. Other key highlights for the period included exploration success in PEL 91, the granting of a series of retention licenses providing security of tenure over PEL 92 and PEL 218, early stage results from the onshore Otway program and subsequent to the period , the execution of a farm-out agreement with Woodside Petroleum over its Lake Tanganyika South block in Tanzania and the securing of additional prospective oil exploration acreage via a farm out agreement with Drillsearch over ATP 924.

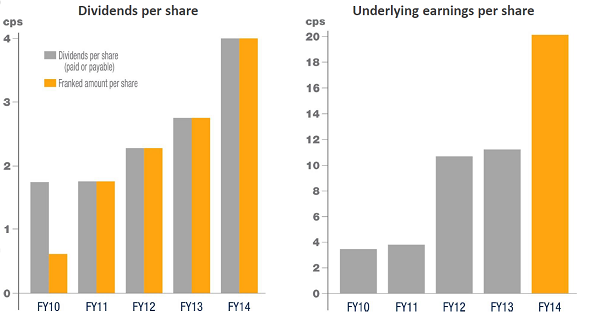

BPT Dividends (Source - Company Reports)

BPT Dividends (Source - Company Reports)

BPT released its updated reserves assessment as at June 30

th 2014 with 1P reserves, 2P and 3P reserves all lower at 33.4mmboe, 85.6mmboe and 181.7mmboe, respectively after record oil production. The reserves included the impact of recent successes at Stunsail and Pennington however overall failed to offset oil production of 5.2mmbbls with the oil down from 22.0 to 19.3 mmbbls. 2C contingent resources were increased overall from 449mmboe to 467mmboe on the back of drilling and completion activity at its NTNG project, offsetting adjustments to 2C oil and conventional gas.

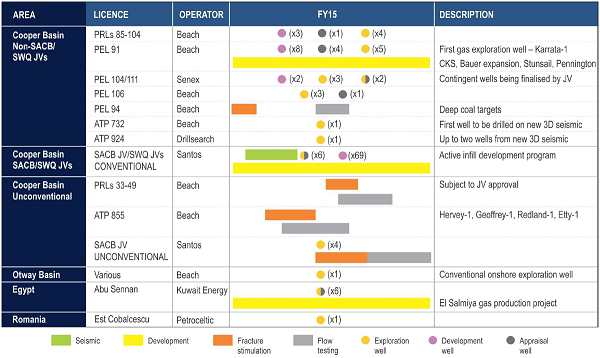

Key Activities (Source - Company Reports)

Key Activities (Source - Company Reports)

Production guidance for FY2015 has been provided in a fairly broad range of 8.6 to 9.4mmboe, reflecting uncertainty regarding the timing of new production tie-in in the western flank and natural decline of the Bauer oil field plus the timing of ramp up from the SACB JV. In our view the ability to sustain production from the Western Flank and to realize an increase in SACB JV production will be the key determinants for BPT over the coming year with its strong momentum to date corner stoned by the outperformance of the Bauer oil field. Production decline will be offset by the recent expansion of fluid handling capacity to 50,000bbls/d and by the tie on of Chiton-3, Bauer-12 with the June 2015 Q tie in of the KCS, Pennington and Stunsail fields to support FY16 production.

BPT Sales Revenue (Source - Company Reports)

BPT Sales Revenue (Source - Company Reports)

The ability to sustain Western Flank oil production will be a key determinant for BPT through FY15 with development activity focused on additional development drilling at Bauer, tie in of existing discoveries at KCS, Stunsail and Pennington towards the end of the year. Exploration will be the key in proving additional reserves and providing insight into the longer term productivity of the acreage with four exploration wells in PEL 92, five wells in PEL 91 and three wells in the Senex Energy operated PELs 104/111. We eagerly await the commencement of exploration drilling in the QLD Cooper Basin with wells planned in ATP 732 and in ATP 924 under farm in agreements with Bengal Energy and Drill search. Success could open up a new area of focus for expansion of BPT’s oil business.

BPT Daily Chart (Source - Company Reports)

BPT Daily Chart (Source - Company Reports)

With an outstanding FY14 performance driven by the Beach operated oil business and a very strong balance sheet with the potential to fund capex until the end of FY16 we believe FY15 should be a good year for BPT. Also Nappamerri Trough Natural Gas (NTNG) exploration program is on track for completion of Stage 1 exploration phase at the end of Q1 2015. There is a review of all international assets currently underway to refocus capital allocation over medium term. We put a BUY recommendation on the stock at the current price of $1.63.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...