Company Profile – BHP Billiton is the world’s largest diversified resources company. Key businesses are coal (Coking and Thermal), base metals, iron ore, aluminium, stainless steel and petroleum. BHP’s strategy focuses on building, acquiring and expanding tier one assets across its diversified commodity suite. Tier 1 assets are long life, low cost and expandable. BHP has got operations in Australia, United States, Africa, Asia and South America. BHP generally operates through customer sector groups (CSG’s). BHP is headquartered in Melbourne and employs more than 45000 people. The group recorded revenue of more than $65, 968 Million in FY2013.

Analysis – BHP Billiton has a healthy share of the world’s largest and lowest cost mines. These are readily expandable and BHP has been investing billions of dollars to that end. It has increased iron ore production by about 50% during the past three years. Most recently the firm approved expenditure, including Rapid Growth Project 6 that will increase Western Australian capacity 10% to 240 million tons per year by 2016. Mining companies are largely producers of undifferentiated commodities. In the long run they have been price takers and not price makers. But firms such as BHP have gained more say with growing concentration because of takeovers and mergers. The breakdown of the traditional iron ore contract pricing system in favour of an index based mechanism; reflective of industry fundamentals is a boon to miners and evidence of the not so subtle shift in power.

Iron Ore Production (Source - company Reports)

Iron Ore Production (Source - company Reports)

Despite China accounting for lion’s share of the global consumption of many commodity staples, its per capita usage remains well below those of industrialised nations – the difference being china’s vast population. India’s near equivalent numbers portend a lagged reinvigoration of commodity price support. Yet after more than a decade of growth the current resource boom is likely drawing to a close. Geographic and product diversification give BHP more stable cash flow and lower operating risk than most of its mining peers. Most revenue comes from the relative safe havens of Australia/New Zealand, North America and Europe. A geographically diversified customer base allows BHP to benefit from economic growth and development in any part of the world. When all major economies are growing strongly, BHP’s revenues and profits can benefit materially. With growth in demand for most of its products softening because of the maturing Asian economies and worldwide economic malaise, BHP has been recording softer earnings following peak fiscal 2011 levels at USD 21.7 billion. It will likely be mid-decade before volume growth again has the company within sights of this earnings peak.

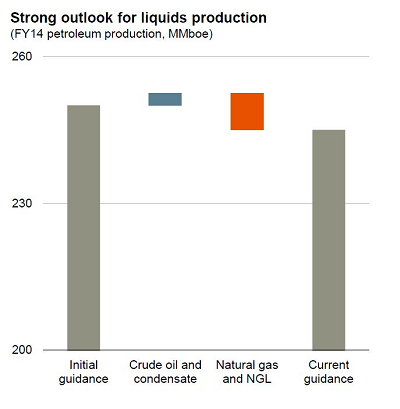

Petroleum Production (Source - Company Reports)

Petroleum Production (Source - Company Reports)

The good times have fortified the balance sheet. Some cash has been returned to shareholders, but the bulk of the windfall financed growth. With commodities peaked and capital costs still high, focus has shifted to fiscal discipline and grinding costs down in order to eke gains. The approach is likely also to yield increased distributions to shareholders. It is difficult to create and protect competitive advantages while focusing on multiple commodities. With the exception of iron ore we think BHP lacks real pricing power in its products. There is a risk that expanding at near peak market conditions will result in lower than optimal returns on investment.

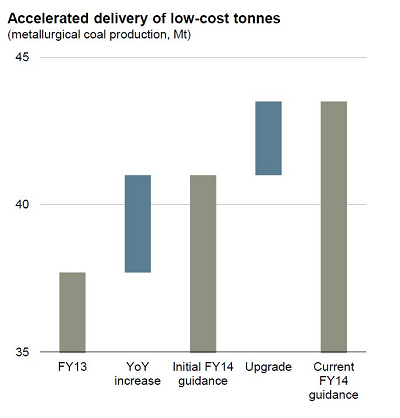

Metallurgical Coal Production (Source - Company Reports)

Metallurgical Coal Production (Source - Company Reports)

BHP Billiton owns a very substantial portion of the planet’s long life, low cost, export oriented, expandable mining assets. Many of these are effectively irreplaceable, with low sovereign risk and proximity to key Asian markets. The assets can grow to meet the world’s long term increase in demand for natural resources. A combination of excellent management, boom time commodity prices and a good deal of luck delivered BHP a very strong balance sheet. Investing throughout the cycle BHP leapt ahead while others floundered. The company is on strong financial footing. Returns on invested capital have averaged 18% during the past five years and remained greater than 20% during the global financial crisis. The worth of BHP Billiton’s diversified earnings stream was tested and proved. The company has reinvested throughout the cycle. Net interest coverage has averaged 25 times during the past five years. At the end of December 2013 BHP Billiton had USD 27.1 billion in net debt, reduced following strong cash flow from the reined in capital expenditure. The balance sheet is manageable leveraged at 33% net debt to equity. Tax-effective share buy backs have been a feature of recent years and may remerge given strong cash flow.

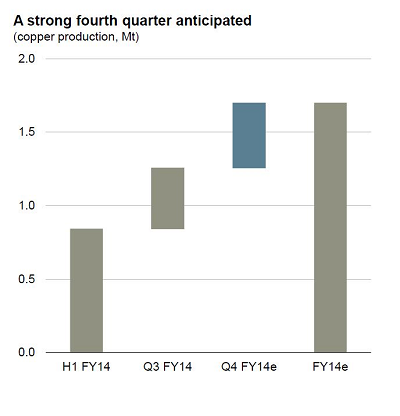

Copper Production (Source - Company Reports)

Copper Production (Source - Company Reports)

We maintain our BUY recommendation on BHP Billiton. We believe that commodity prices will oscillate (but not appreciate much) on the back of Chinese stimulus/tightening cycles and supply growth from completion of projects started several years ago. Against that backdrop BHP Billiton is the most balanced investment case combining returns of cash with reinvestment for growth at a reasonable valuation. BHP Billiton offers a dividend yield of 3.55% which is fully covered by free cash flow using spot commodity prices, in contrast to many peers. Furthermore the probability of additional capital returns via buy back or special dividend at BHP Billiton’s full year results in August 2014 are high in our view. The group can also return up to US$10bn in additional payments to shareholders over 2 years and simultaneously invest for growth. BHP Billiton has embedded the focus on productivity in the organisation. We see potential for upside beyond its US$5.5bn target either via lower unit costs or lower capex.

BHP Daily Chart (Source - Company Reports)

BHP Daily Chart (Source - Company Reports)

There has been media speculation that BHP Billiton can spin off non-core assets to accelerate simplifying its portfolio. In response BHP Billiton confirmed it continues to look at structural solutions to its non-core operations. This does demonstrate that BHP Billiton is taking decisive steps. This could give the market more confidence on BHP Billiton’s re investment plans and potential for more productivity gains. Petroleum accounts for around 24% of EBIT in the next three years, we estimate. In periods of volatility in metals and minerals, where prices are mainly driven by Chinese demand, this serves as a buffer that few of its peers can offer. Under CEO Andrew Mackenzie BHP Billiton has changed its approach to reinvestments. It has capped total investments at US$15bn per year for the moment. This automatically limits the number of projects it can pursue and raises the probability of successful execution. BHP Billiton has changed its capital allocation with a focus on far fewer projects and assets. These are assets BHP Billiton has been mining for a long time with known characteristics, established government relations and in relatively stable jurisdictions like Chile, Australia, the US and Canada.

Over the 18 months to December 2013, BHP Billiton has delivered US$4.9 bn of pre-tax productivity gains or around US$0.58 per share post tax. Relatively easy cuts in exploration spending accounted for 32%. Operational savings accounted for 37% with the remaining 31% from capacity creep. The reduction in ordinary operating expenditure amounts to a 3% annual productivity gain of US$5.5 billion by year end FY14 and we think the equity markets have fully discounted this after the BHP Billiton’s first half results and guidance.

CEO Andrew Mackenzie has embedded the focus on productivity across BHP Billiton’s organisation. The group has also stated it expects there to be further upside to the target of US$5.5bn but has not provided any further objectives. BHP is currently focusing on removing costs from the business, focusing on operating performance, productivity simplification, expanding margins and the generation of free cash flow. BHP Billiton is encouraging internal competition for capital to ensure the absolute best return investments are being made. BHP had US$5bn of divestments announced in FY13 in an attempt to simplify the portfolio. We believe BHP’s initiatives for 2014 are positive for shareholders and expect BHP to consider a share buyback in relation to FY14 financial result. We reiterate our BUY recommendation on the stock at the current price of $36.16.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Please wait processing your request...

Please wait processing your request...