Kalkine has a fully transformed New Avatar.

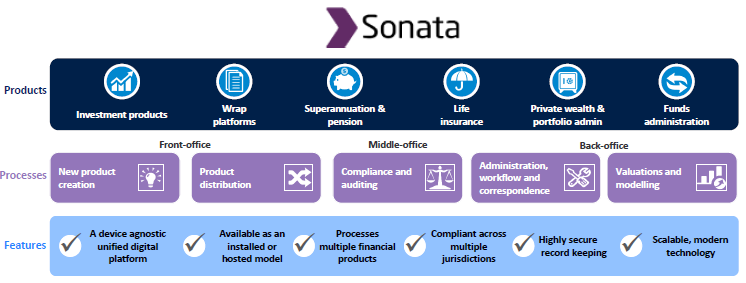

Company Overview: Bravura Solutions Limited provides software products and services to clients operating in the wealth management and funds administration industries in the Asia-Pacific and Europe, Middle East and Africa regions. The Company's software products and services support the front-office, middle-office and back-office functions needed to manage and administer financial products across investment products and wrap platforms, superannuation, pension and retirement products, life insurance, private wealth and portfolio administration. It operates across two segments: Wealth Management, which provides software and services that support back-office functions relating to the management of investment products and wrap platforms, superannuation, pension and retirement products, and life insurance, and Funds Administration, which supports back-office administration requirements for a range of investment managers, custodians and third-party administrators for both retail and institutional customers.

BVS Details

Bravura Solutions Limited (ASX: BVS) is a leading software solutions provider. The company provides services in managing superannuation, pensions, life insurance, investments, fund administration, etc. It has a flagship software product called ‘Sonata’ which is used by several financial institutions across the globe. The company operates in key business segments including Wealth Management and Fund Administration. It has a market capitalization of circa $1.19 billion (as on 7th June 2019). Since its inception in the year 2004, the company has accumulated many achievements and milestones. It has completed several acquisitions and launched new products. Bravura has expanded its operations to become a leading global supplier of professional services and software solutions. It has a huge client base across the world and has offices across Australia, New Zealand, United Kingdom, Europe, Africa and Asia. The company has an objective to create agile solutions to provide a competitive advantage to its clients. However, it is exposed to several material business risks including increased competition, foreign exchange risks, etc., and uses several risks mitigation techniques to combat these. Robust fundamental parameters including, strong recurring revenue growth, strong sales pipelines, etc., have strengthened the company’s position among its peers in its segment.

Large Addressable Market: The company provides a range of services which includes pensions, life insurance, investment products platform, etc., across key markets located in the UK, Australia, New Zealand, and South Africa. These include several blue-chip financial services companies. The industry in which the company operates is represented by high-cost structure as several organisations in these markets have multiple legacy or competitor systems. Hence, there is a less product flexibility, with difficulty in responding quickly to changes in regulatory regimes, while meeting the emerging requirements of the current digital world. On the analysis front, the company reported strong 1H19 financial results across all key financial metrics. The revenue for 1H19 stood at $127.4 million, an increase of 23.8% over the prior comparative period, mainly driven by significant new business, continuing project work, expansion of managed and cloud services, and increasing demand from existing clients. The EBITDA of the company has increased to $23.8 million, an increase of 28.4% above than the prior comparative period. However, the net profit after tax was up by 14.7% to A$16.3 million as compared to A$14.2 million in 1H18, equating an 18% effective tax rate in 1H19, with the prior comparative period impacted by a $1.8 million deferred tax asset.

.png)

Strong Revenue & Earnings Growth (Source: Company Reports)

The wealth management revenue increased by 24.2% to $90.4 million. Two new Sonata contracts were achieved by the segment during 1HFY19. The funds administration revenue increased by 22.9% to $37.0 million. Increased implementation & development work arising from a renewed and enhanced contract with a significant global client benefitted the segment. Moreover, the company’s top line has been witnessing favourable momentum in the past few years which reflects that it is having strong revenue generation capabilities. We expect that top-line growth might be continued in years ahead as it had witnessed a CAGR growth of 13.3% between FY15-FY18.

Strong Pipeline of Opportunities: The sales pipeline of the company remained robust driven by the demand from its key markets and across its geographic regions, which include several established financial institutions who are evaluating the suitability of the products of the company and its digital offerings to replace their legacy or competitor systems. The strong pipeline is on the back of sales opportunities from new clients and significant project activities from existing clients as well. The company has good visibility of its strong sales pipeline over a period of twelve to eighteen months.

Prudent Investment in Sonata Supporting the Business Growth: The strong revenue growth of the company continued with increasing operating leverage. Bravura attained strong growth driven by investment in Sonata along with achieving two new Sonata contracts during the first half of FY19. The company started several additional projects for new and existing clients along with the implementation of several successful clients. Moreover, the attractive value proposition of Sonata which supports clients with managing a new regulation, digital & cost pressures have been a primary driver in the significant growth of the company’s revenue which currently makes up a substantial part of the Wealth Management business of the company.

About Sonata (Source: Company Reports)

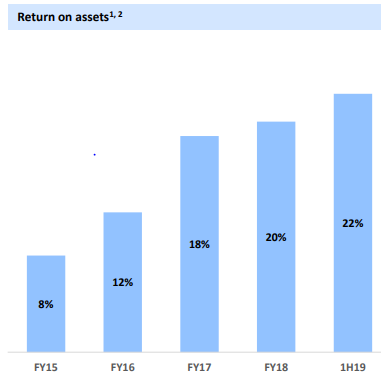

Delivering Attractive Shareholder’s Returns: The strong business performance of the company is delivering attractive returns to the shareholder. Bravura has declared an interim dividend of 5.3 cents per share, which represents 70 per cent of the earnings per share in the first half of FY19. The Return on equity (which is based on annualised NPAT over average total equity) for the company stood at 28% in 1H19 as compared to 26.0% in the prior corresponding period of 1H18. Improvement in ROE was on the back of consistent and long-term investment by the company in product development, deep market knowledge & expertise, sound business model and driving significant operating leverage. The ROA stood at 22% as compared to 20% in FY18.

Return on assets (Source: Company Reports)

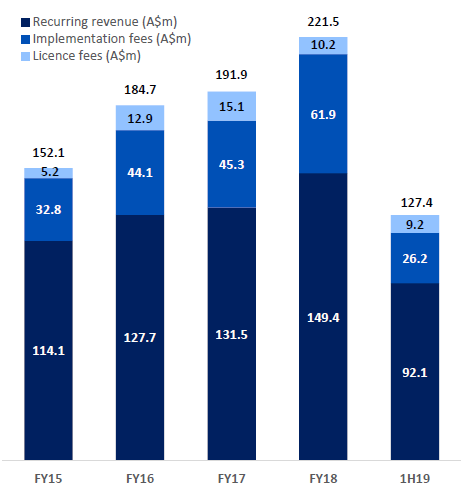

Strong Growth In Recurring Revenue: The recurring revenue for the company was up by 31% in 1H19 as compared to the prior corresponding period, and it was comprised of 72% of the total revenue. The recurring revenue of the company increased in 1HFY19 due to the addition of new clients and with the enhanced use of functionality by the existing clients, supported by the long-term nature of the client contracts of the company.

The significant recurring revenue base of the company supports the long-term earnings profile along with future cash flow expectations. The new contract wins attracted implementation fees over the initial phase of two to three years, as clients deeply embed Bravura’s solutions into their business’s core operating model. Demand of maintenance, managed services, and in-production professional services from the ongoing client forms a substantial part of the recurring revenue for the company.

Strong Recurring Revenue Growth (Source: Company Reports)

Decent Cashflow Position: The company has witnessed a decent financial position, with a net cash balance of A$14.0 million. At balance date, A$12.0 million was drawn down on the working capital facility. The company has a significant investment capacity to take advantage of organic and acquisitive growth opportunities. The operating cash flow stood at A$8.0 million during the period, reflecting a cash conversion of 34%, arising partly from significant tax payments which amounted to A$2.7 million, and from previously disclosed cash receipts prepaid in the second half of 2018. The 2H18 cash conversion was 158%. The management expects a cash conversion in the range of ~70-80% over a period. The long-term cash flow is supported by predictable, long-term, client contracts of the company.

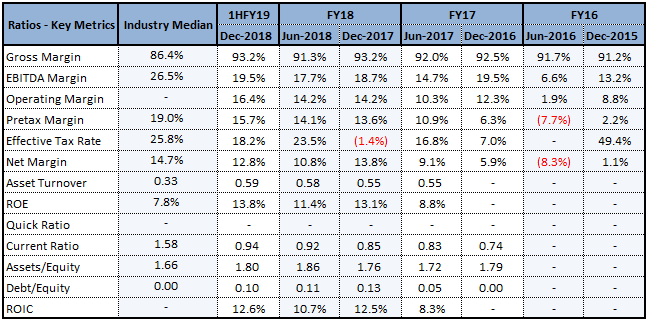

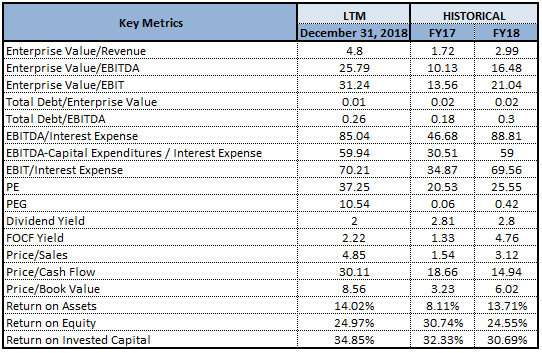

Key Ratios (Source: Thomson Reuters)

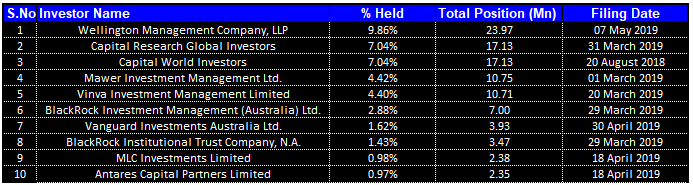

Top 10 Shareholders: Top ten shareholders form around 40.63% of the total shareholding as highlighted in the below table. Wellington Management Company, LLP holds maximum interest in the company with a stake of 9.86% followed by Capital Research Global Investors. and Capital World Investors both with 7.04% each.

Top Ten Shareholders (Source: Thomson Reuters)

Key Risks & Threats: The company is exposed to several material business risks. The company is exposed to factors including increased competition from specialist software vendors, foreign exchange risks, economic climate and information security breach and failure of critical systems. However, it mitigates its risks through several factors like investing in sonata development to enhance the core platform, implementing several employee incentives to attract and retain key personnel. The company has expanded its business to several jurisdictions to diversify the risks arising out of an uncertain economic environment.

Outlook Ahead: The company has a strong pipeline with sales opportunities from new clients and significant project activity from the existing clients. The company is well positioned and can take advantage of strong demand in several countries including the UK, Australia, New Zealand, South Africa, and Asia. The strong demand is driven by the need of the clients to quickly market for new products, digital capabilities, navigating maturing & evolving regulation and extracting operational efficiencies.

Robust growth along with increasing scale and greater efficiency are driving increased operating leverage. The increasing investment in Sonata continues to support client demand and deepen product functionality.

The large range of the product is complemented, by enhanced digital and cloud solutions. It strengthens the position of the company to be a market leader in its established markets. The company has revised upward its full-year 2019 guidance on the back of strong demand resulting in forecast EPS growth in the mid to high-teens.

Key Valuation Metrics (Source: Thomson Reuters)

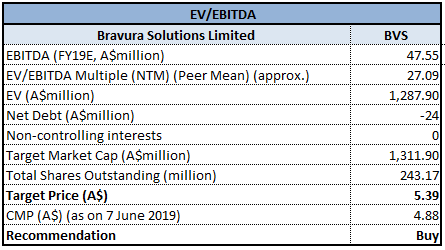

EV/EBITDA Multiple Approach (NTM):

EV/EBITDA Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

Stock Recommendation: Meanwhile, the stock of Bravura has yielded a YTD return of 29.21% (as of 7 June 2019) and is trading at a P/E multiple of 35.17x. From the technical analysis standpoint, the stock is currently taking the support of 200-days exponential moving average which is at $4.676. The prices previously rose post taking the support of 200-days exponential moving average from the level of A$3.470 (Day’s low on 10th December 2018). With the current scenario of the large addressable market, strong pipelines, support from investment in Sonata places, the company is positioned to reap the benefits, going forward, among its peers. Along with strong operating and financial results, the company is well poised to capitalize on its key and core revenue drivers to boost the stream of revenues, going ahead. Further, the core financials of the company look strong with robust growth across its business segments. By looking at its positive outlook and decent guidance of the company, we have valued the stock using a relative valuation method, EV/EBITDA multiple and arrived at the target price of $5.3 (single digit upside (%)). Hence, we recommend a “Buy” rating on the stock at the current market price of $4.88 per share (down, 0.611% on 07 June 2019).

.png)

BVS Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...