Company Profile - Buru Energy Limited (Buru) is engaged in oil and gas exploration and production in the Canning Superbasin, in the northwest of Western Australia. The Company’s Yulleroo 3 well is located in Exploration Permit EP 391 some 80 kilometres to the east of Broome. The Asgard 1 well is located in Exploration Permit EP 371 some 180 kilometres to the southeast of Derby, and 30 kilometres northeast of Noonkanbah Station. The Ungani North 1 well is located in Exploration Permit EP 391 some 100 kilometres to the east of Broome, and lies some six kilometres north of the Ungani Production Facility. The Yulleroo 4 well is located in Exploration Permit EP 436.The Company’s subsidiaries include Terratek Drilling Tools Pty Limited, Royalty Holding Company Pty Limited, Buru Energy (Acacia) Pty Limited, Buru Operations Pty Limited and Yakka Munga Pastoral Company Pty Limited.

Analysis – During the quarter, the first load out of Ungani crude oil from the Port of Wyndham was made. Two crude export shipments have now been made from Wyndham totalling 71,270 barrels. The first two cargoes were sold to a refinery in Thailand and the third 38,000bbl shipment will be delivered to a Singapore refinery, which reduces shipping distance and turnaround time. Ungani crude is being well received in the Asian markets ahead of the planned field development later in 2014. The Ungani well was brought on production during the quarter to clean the well up after the workover conducted in late 2013. The well has produced at rates of up to 1,000 barrels of fluid per day but the production results indicate that the workover has not completely isolated the deeper water zone as planned and further work would be required to isolate the deeper zone, as was successfully undertaken in Ungani 2.

Ungani Development (Source - Company Reports)

Ungani Development (Source - Company Reports)

The ungani 3 appraisal well was drilled during the quarter some 700 metres to the east currently producing wells, to appraise the eastern structural lobe of the central field. The well encountered an oil saturated Ungani Dolomite section but unfortunately the reservoir quality appears poor, without the highly developed vugular porosity seen in other two wells in the field. The recently completed Ungani-3 well was targeting an Eastern lobe of the Ungani Field, sitting on one side of an interpreted fault. Oil was discovered near to prognosis depth however the reservoir quality is relatively poor in that t is much tighter than that observed at Ungani -1 and 2. We understand that Ungani-3 lobe was hoped to be around 3-4mmbbls. We have lowered our forecast of recoverable oil from the Ungani field to 10mmbbls from the 20mmbbls we had assumed previously.

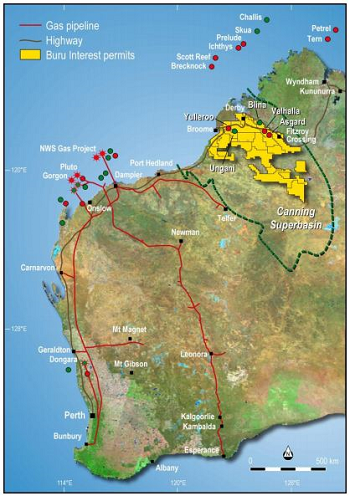

Buru Interest Permits (Source - Company Reports)

Buru Interest Permits (Source - Company Reports)

A dramatic improvement in the seismic data quality of the 2013 Ungani 3D survey was achieved during the quarter from a trial by a specialist processing centre in the US and as a result the entire 3D data suite over the Ungani Central Field will now be reprocessed to better define the structure and stratigraphy within the Ungani Field. The full set of reprocessed data is expected to be received this month.

Ungani Oilfield Progressing To Export (Source - company Reports)

Ungani Oilfield Progressing To Export (Source - company Reports)

Significant progress was made on the 2014 Laurel tight gas testing preparations and approvals in March Quarter. The operations plan was submitted to the DMP for approval and the Environmental Management Plan was reviewed by the DMP and the EPA and deemed not to need independent review by the EPA due to the low impact and limited scope of work. During the quarter the company also undertook extensive community consultation and supported the Traditional Owners in access to independent experts to review the proposed program. Based on discussions to date the company expects to receive formal regulatory approval in the second quarter and commence operations in the third quarter.

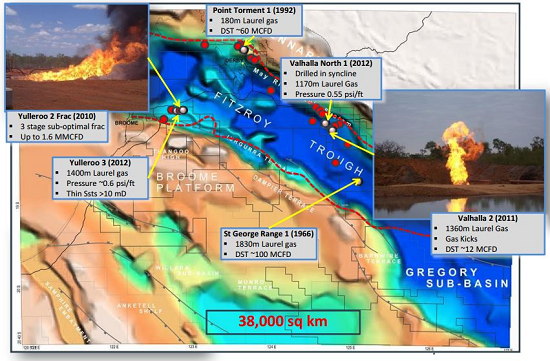

Laurel Gas Project (Source - Company Reports)

Laurel Gas Project (Source - Company Reports)

The combined outcomes of the unexpected Ungani 3 result necessitating a re-evaluation of the Ungani reservoir distribution, the dramatic improvement in the data quality from the reprocessing of the Ungani 3D, together with better than expected performance of Ungani 2 in the Ungani Central field and the decision to acquire large scale 3D seismic surveys along trend from the Ungani Central Field has led BRU to make a operationally prudent decision to demobilise the Crusader 405 rig.

The company recorded a net cash outflow of $15.5 million for the quarter and at the end of the quarter had net cash reserves of $44.7 million. Exploration expenditure of $2.7 million for the quarter. Ungani development expenditure of $9.0 million, the majority of which were cost associated with the drilling of the Ungani 3 Well. The company is forecasting a net cash outflow of some $4.5 million in the June 2014 quarter.

Despite heavy seasonal rainfall in the Ungani area during the wet season, the EPT continued to perform well with 48,400 barrels of oil produced during the quarter. There were periods during which the wet weather necessitated the closure of roads for safety and operational reasons and these closures restricted production during January and February. However rainfall was significant lower in March, leading to good access track availability. Four road trains are currently transporting crude from Ungani To Wyndham with production avergaing1200 bopd with no water cut and now evident pressure depletion. The reservoir performance is significantly exceeding modelled technical expectations. A fifth road train commenced operation in April which will further increase the transport capacity to Wyndham Port, with oil sales only constrained by vessel availability from the export route through Wyndham Port.

The Ungani 3 result highlighted the fact that advanced processing of 3D seismic data is necessary to ensure optimal well locations. The Ungani trend is highly prospective for additional oil discoveries but additional seismic data to constrain and optimise future drilling programs is required. The Ungani North 1 test will be undertaken in conjunction with the mobilisation of equipment for the Laurel tight gas program. The Laurel tight gas evaluation program is progressing as planned, with field activities expected to commence in August subject to final approvals. Good progress has been made with the regulatory process and community consultation. Contracts for the program are currently being finalised to allow implementation upon receipt of all the require approvals.

The March quarter has been a challenging period for Buru. The commencement of test production and subsequent excellent performance from the extended production test at Ungani 2, which is performing well above expectations, the significant progress on the 2014 Laurel tight gas program preparation and approvals, the commencement of crude export and the delineation of new prospectivity from the 2013 2D Frome Rocks survey set the foundation for a positive quarter and the year ahead. This was disappointingly offset in the short term by Ungani 3 appraisal well resulting in the need to reinterpret the Ungani field area with the reprocessed 3D seismic data. The share price reaction to the poor result at Ungani – 3 appears overly harsh. That said BRU will have to deliver oil exploration success or further news on the gas appraisal to see further performance from here. CY14 is shaping up as a critical year for the Canning Basin pure play as it progresses the conventional oil plays and tight wet gas plays in tandem. We think the Canning Basin is one of the most prospective basins in Australia and Buru offers a pure play on both the oil and tight wet gas plays in the canning. We reiterate a BUY on the stock at the current price of $1.125.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Please wait processing your request...

Please wait processing your request...