Company Description - Buru Energy Limited (Buru) is engaged in oil and gas exploration and production in the Canning Superbasin, in the northwest of Western Australia. The Company’s Yulleroo 3 well is located in Exploration Permit EP 391 some 80 kilometers to the east of Broome. The Asgard 1 well is located in Exploration Permit EP 371 some 180 kilometers to the southeast of Derby, and 30 kilometers northeast of Noonkanbah Station. The Ungani North 1 well is located in Exploration Permit EP 391 some 100 kilometers to the east of Broome, and lies some six kilometers north of the Ungani Production Facility. The Yulleroo 4 well is located in Exploration Permit EP 436.

Analysis - With this report we bring our focus back to Australia’s largest acreage holder in the Canning Basin and operator of majority of its exploration permits, i.e., Buru Energy (‘BRU’, Australian S&P/ASX 300 listed oil and gas exploration and production company).

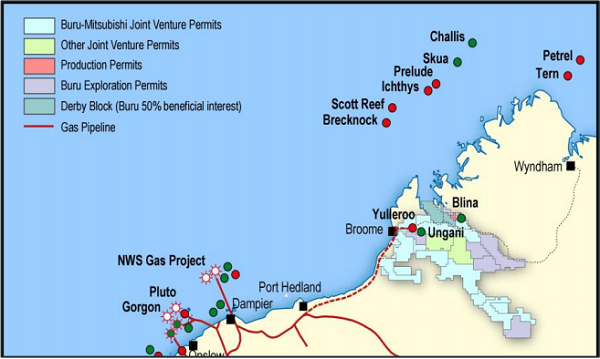

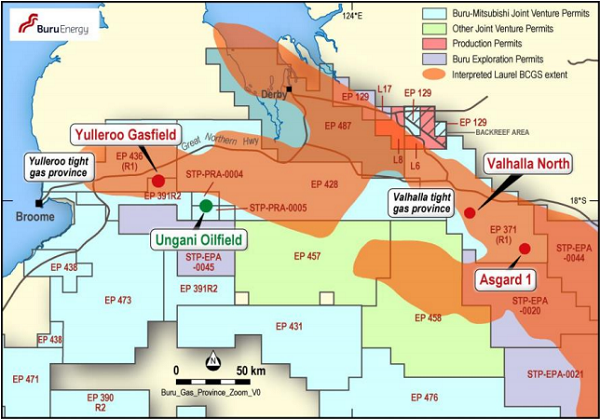

Acreage Position (Source - Company Reports)

Acreage Position (Source - Company Reports)

Buru set the foundation for a progressive first quarter 2014 with the outstanding performance from the production tests at Ungani-2 well and the 2014 Laurel Tight Gas Program setting. However, the recent below-par drilling results of Buru’s Ungani-3 well, paring back of the earlier four wells for the Ungani near-field exploration in 2014 to one well, and delays with respect to the highly prospective Laurel formation frac testing program coupled with the recent management/board change, have got all eyes on Buru. Although the excitement that shook our spines earlier in CY11 and CY12 appears to be a little murkier at present in view of the sloth in the earlier anticipated ‘on-track’ oil & gas programs mainly due to washing away of the profits made in the past three years to salvage Buru’s share price, the Laurel testing program that is now set to commence in the CY15 dry season brings a ray of hope.

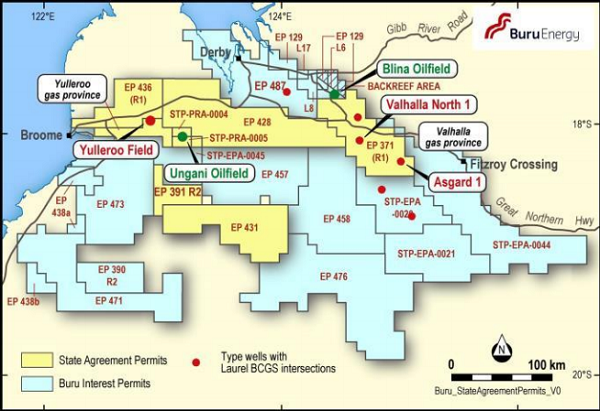

Active Acreage Management (Source - Company Reports)

Active Acreage Management (Source - Company Reports)

More importantly, Buru’s announcement on the above disappointing operations updates (ending Jun 2014) may indicate some uncertainty in the stock, following the sudden departure of MD Keiran Wulff. Additionally, Buru's recent experience with the Ungani-1 & -3 wells suggests execution of Canning Basin opportunities to be more challenging than previously considered.

Conventional Oil Exploration (Source - Company Reports)

Conventional Oil Exploration (Source - Company Reports)

From financial support standpoint, Buru is fully funded through to 2H15 even after looking at a heavy CY15 CAPEX program and gloomy response with respect to the Ungani oil cash flows. It is expected that the Ungani development CAPEX will be funded out of the Mitsubishi $27.5m accelerated carry and a significant portion of the Laurel formation frac testing program will be covered out of the A$20m released from the Alcoa escrow account. A$50m oil reserve based debt facility in 2H15 is being forecasted to assist funding the CAPEX program. However, this may be dependent upon Ungani full field Final Investment Decision, which suggests some level of inaccessibility to the entire funding.

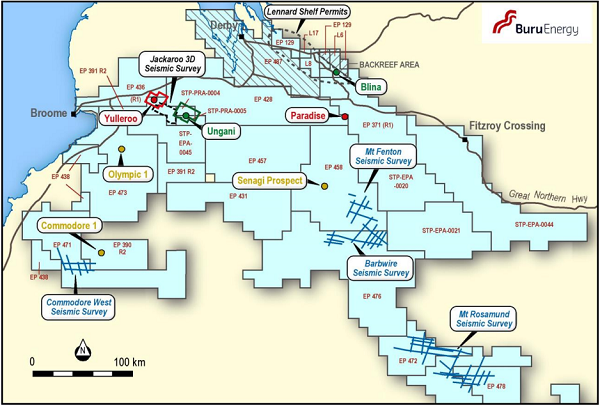

Exploration & Appraisal Program (Source - Company Reports)

Exploration & Appraisal Program (Source - Company Reports)

In view of thedelay in Ungani oil production ramp-up,earnings estimates for CY14 and CY15 have been relegated to some extent. The current and average quarterly production rates of ~1,000bopd (gross) are supported by Ungani-2 well, where water cut remains <1% despite phase 2 of the Exploration and Production. The production test phase 1 (May 2012 to Mar 2013) yielded 101,278 bbls; and the production test phase 2 (Dec 2013 to Jun 2014) yielded 172,535 bbls. During the interim, four shipments totaling 143, 317 bbls were made from the Port of Wyndham and the fifth shipment of 34,170 bbls has been sold in Jul 2014. The oil has been sold into Asian refineries under the marketing agreement between Buru and Mitsubishi. Further, the upgrade of the facilities for permanent production is being reviewed to facilitate “fit for purpose” Ungani facilities completed at lowest possible cost. This is specifically in view of the work-over required for Ungani-1 well in 2H14. It is assessed that production may not increase from the current 1,200bopd to 1,500bopd on testing until another development well is drilled in 2Q15. The estimate target of 5,000bopd production appears to be met only by the end CY15.

Laurel Gas (Source - Company Reports)

Laurel Gas (Source - Company Reports)

BRU is exploring the prospects of having at least one shallow oil across the Ungani trend drilled by either the DCA7 rig or the rig to be used to drill the Olympus & Commodore prospects in the Coastal permits in 2H14, considering further seismic activities.

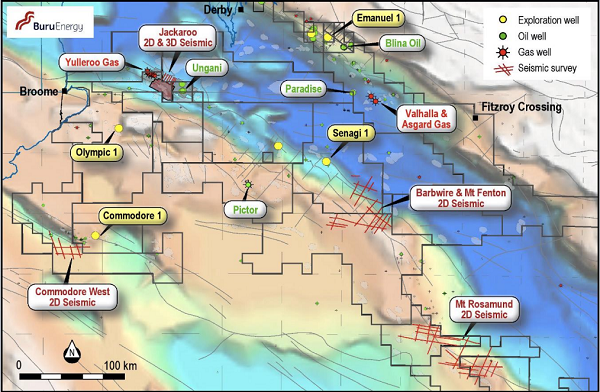

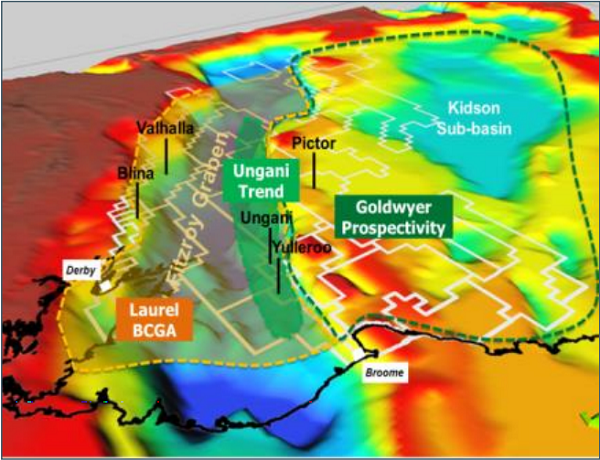

Three major petroleum systems (Source - Company Reports)

Three major petroleum systems (Source - Company Reports)

With regards to the Laurel tight gas program (covering the Valhalla and Yulleroo regions), theenvironmental approvals were secured in late June 2014; however, the results from respective fracture stimulation program are delayed until the 2015 dry season. Nonetheless, the revised total cost of A$40m is ~25% lower than the original budget and the delay will allow BRU to take a methodical approach for decision-making. In addition, Buru has obtained support from the Yungngora Community at Noonkanbah Station for this Exploration Program. It has also informed the Yawuru community and has agreed to meet the environmental, cultural, social and economic conditions set by the community if going ahead with fracking. Further, Buru has well-recognized the need for seeking approvals on its proposed work from joint venture parties, traditional owners and appropriate regulatory authorities to ensure seamless operations.

Ungani Field Facility (Source - Company Reports)

Ungani Field Facility (Source - Company Reports)

In view of the aforementioned, Buru still remains to be of interest as its Canning Basin pure play latches over the conventional oil plays and tight wet gas plays in tandem, come CY15. Specifically, Ungani oil development drilling over CY14/15; flow testing of Ungani North-1 oil & gas discoveries and the frac program which are expected to commence in mid CY15; and additional oil exploration wells, will lead to a share price thrust.

BRU Daily Chart (Source - Thomson Reuters)

BRU Daily Chart (Source - Thomson Reuters)

Nonetheless, it is prudent to understand that the risk to price target would further be dependent on decrease in oil price, or strengthening of the AUD/USD FX rate; failures on either wet gas exploration/appraisal or conventional oil targets; and deferment or adjournment of mining/resources related projects in Western Australia which could lower gas pricing and demand. Such factors contributing to changing global economic conditions with/ without introduction of improved products or service offerings by competitors may affect Buru’s operations, which may lead to entry into transactions, including transactions in derivative instruments, to mitigate any risks due to said exposure(s). Further, any delays in the development of Canning Basin resource base could also adversely affect revenue generation and therefore impact Buru’s ability to realize value from its acreage position.

To overcome most of the above-stated challenges being encountered by Buru, the company has confirmed exploration wells Olympus & Commodore planned for 3Q (funded by Apache) and rig tenders being assessed and contracted; and scheduling of 2D & 3D seismic programs to be focused on Ungani Trend & high-graded areas, which will be followed by multi-well program 2015 onwards. These programs will help improve the ability to predict stratigraphy, provide greater predictability while de-risking the drilling options, and key to understand the structure and reservoir controls.

The stock of the company was A$0.91 for the 52 weeks ending 5th Sep 2014. During the 12 months ending 31 Dec 2013, the company has experienced losses totaling A$0.10 per share. The company is currently trading at 133.74 times sales as opposed to its competitors, and more particularly, it is trading at 2.06 times book value. The company recorded a net cash outflow of A$15.5 million from operating activities & a net cash outflow of A$7.5 million from investing activities for the 1H14; and at the end of 1H14, Buru had a net decrease in cash & cash equivalents of A$22.5 million.

Based on the Buru’s Corporate Updates vide its Sep ‘14 report, one can very well appreciate that Buru has, (1) Sweeping basin wide acreage spread and hefty oil & gas potential with oil production from Ungani field. (2) Three major petroleum systems – Ungani Oil, Laurel tight gas program and Goldwyer/Acacia. (3) Association with major international partners (Mitsubishi and Apache (4) High equities and operatorship

We also note that the screws have been further tightened by restructuring the company’s board to reflect significant change in its operational focus after the exit of Buru’s MD.

In addition, the very recent updates indicate Buru in a positive light with the continuous high production from the Ungani-2 well, successful first stage of the Ungani-1 well work-over, planning of the work-over for the Ungani-3 well, up-gradation of production facilities to improve operability and up-time, lower cost fixed price exploration drilling, and healthier funding status which entails Ungani development being strongly cash flow positive in production rather than exploration mode & Mitsubishi Funding agreement resetting under negotiation ($27.5 million).

There appears to be a surge in how Buru is re-emerging by virtue of its 1H14 results. 1H14 normalized net loss of -A$8m was in line with the earlier mentioned -A$7m forecast. Net cash as at 30th June of A$38m was as per the earlier forecasts.

Holistically, Buru’s long-term growth profile is featured on the results from the upcoming exploration across its acreage in the Ungani oil trend and the progress of the Laurel tight gas plays, which at the moment appear to be positive. We thus put a BUY recommendation on the stock at the current price of $0.765.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...