Kalkine has a fully transformed New Avatar.

Company Overview: Computershare Limited is engaged in the operation of investor services, plan services, communication services, business services, stakeholder relationship management services and technology services. Its segments are Asia; Australia and New Zealand; Canada; Continental Europe; United Kingdom, Channel Islands, Ireland & Africa; the United States of America, and Technology and Other. The investor services operations include the provision of registry maintenance and related services. The plan services operations include the provision of administration and related services. The communication services operations include scanning and electronic delivery. The business services operations include the provision of bankruptcy and mortgage servicing activities. The stakeholder relationship management services group provides investor communication and management information services. Its technology services include the provision of software, specializing in share registry and financial services.

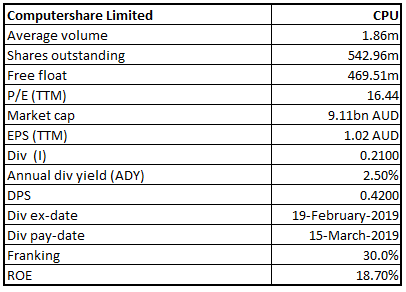

CPU Details

Growth Story Intact: Computershare Limited (ASX: CPU) is a leading global player in transfer agency & share registration, employee equity plans, mortgage servicing, proxy solicitation, and stakeholder communications. With the market capitalization of ~$9.11 billion (as of 24 May 2019), the company has a footprint in all major financial markets with more than 16,000 employee base across the globe. It operates with diversified business domains including Business Services, Register Maintenance & Corporate Actions, Employee Share Plans, Communication Services, Stakeholder Relationship Management and Corporate & Technology.

CPU, established in 1978, is an expert in high integrity data management, high volume transaction processing & reconciliations along with payments & stakeholder engagement. The company focuses on its strategic priorities including growth, profitability and capital management to continue delivering strong results. The company is deriving synergies from the acquisition of Equatex, with its early performance, capabilities and customer engagement. Along with a strong financial performance in the first half, CPU has upgraded its FY19 guidance and is confident to increase its earnings for the full year. The business is prone to several strategic & regulatory risks, operational and financial risks. However, the company is constantly looking for new ways to combat and reduce these risks.

Business Line (Source: Company Reports)

Global Footprint: The company has a consistent go-to-market strategy with an ability to leverage global best practice and local expertise to support clients. It has streamlined activities with duplication eliminated (e.g., infrastructure, development activities), along with unified solutions for international clients and participants with a consistent global toolkit. It has strong co-ordinated front office initiatives including reporting, benchmarking and analytics, product design, customer insights, and revenue opportunities derived by harnessing global data.

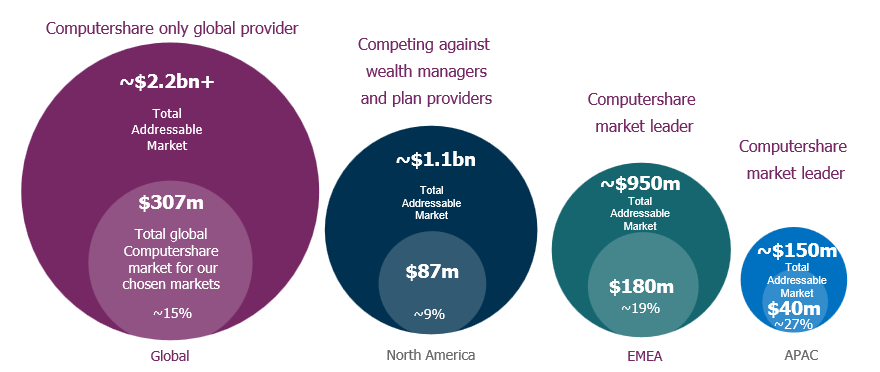

The company has a large addressable global market with scope to improve its position. The total addressable market is ~2.2 billion dollars (in terms of revenue) of which the company currently enjoys only ~15% with a total amount of $307 million. A global management structure will deliver tangible benefits. The company will benefit from global alignment, which will position it for overall growth, margin improvement, and capital deployment more efficiently.

Scope For Growth In Market Share (Source: Company Reports)

Acquisition & Ongoing Structural Growth: Equatex has successfully enhanced the technology and capabilities and has positioned CPU as a leading provider in Europe. CPU has completed the integration of Equatex and affirmed to deliver the synergies worth ~30 million along with additional revenue synergies. The Equatex six-month scorecard is on the target with a year-to-date revenue and EBITDA performance which is ahead of plan. The business integration is progressing well with the completion of EquatePlus technology review which has resulted in exceeded expectations. The market positioning is already improving with prospects interested in the enhanced solutions of CPU. There is 100% positive client response about the upgraded solution with 63% interest in buying additional new products and services.

Equatex Synergies (Source: Company Reports)

The company has seen structural growth and market opportunities and is well-placed to address the trends. Emerging factors such as cyber security, safe custody of assets, compliance and assurance are becoming more important as companies are focusing on counterparty risk. The company has enhanced its focus on user experience, desire for data driven decisions, and support in designing plans. These emerging factors can be understood as the key drivers underpinning the growth of CPU.

The Employee Share Plan administration market is expected to continue to grow at a rate in excess of GDP. The average total market growth is greater than 4.0%. The number of listed and private companies using equity as a part of remuneration is high. Moreover, with high number of participants (participation), the propensity to use equity in rewards is increasing along with a higher regulation, taxation and market practice in remuneration (penetration), which gives the company growth opportunity going forward.

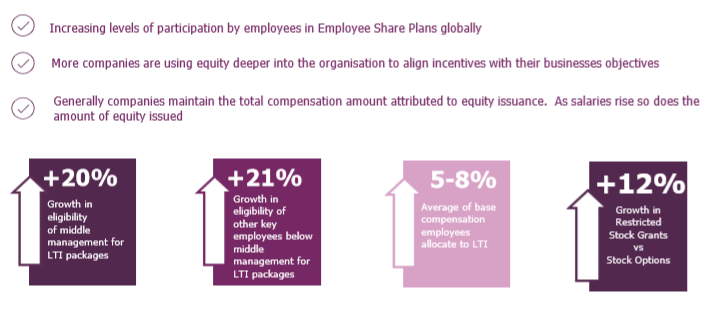

The levels of participation by employees in Employee Share Plans has increased globally. Additionally, more companies are using equity deeper into the organisation to align incentives with their business objectives. With a general trend of companies maintaining the total compensation amount attributed to equity issuance, the total amount of equity issued will see a rise with the hike in salaries.

Trend In Participation & Issuance (Source: Company Reports)

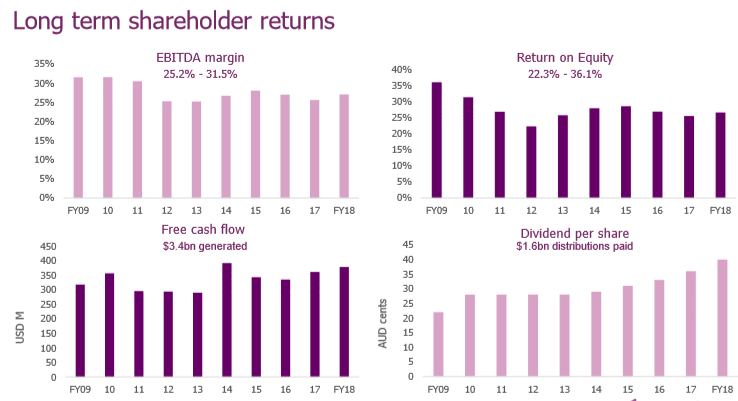

Key Performance Metrics: Among the key performance metrics, several indicators like long-term shareholders return remained stable over the past few years. The EBITDA margin stood in the range of 25.2% to 31.5% from the period of FY09 to FY18. The ROE (Return on Equity) was healthy and remained in the range of 22.3% to 36.1% over FY09 to FY18. Computershare is driven by multiple growth drivers along with US Mortgage Services, Employee Share Plans, and Issuer Services. CPU presents a high-quality business with a broad and large base of long-term customer relationships, recurring revenues and consistent margin range through the cycle along with high returns on equity.

Long Term Shareholder Returns (Source: Company Reports)

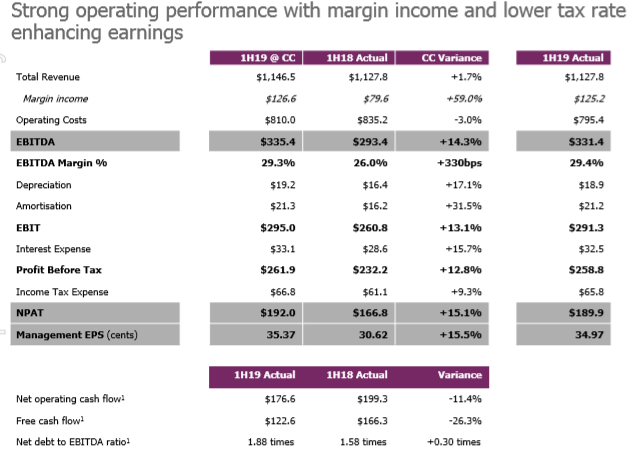

Decent Performance in 1HFY19: The company has maintained strong operating performance with lower tax rates to enhance earnings. The group revenues increased by 1.7% in 1HFY19 on PCP basis. It was mainly driven by strategic growth in Mortgage Services, additional margin income, and Equatex contribution during the same period. In-line with expectation, large event-based activities in 1HFY18 impacted Stakeholder Relationship Management, Corporate Actions and Class Actions performance as compared to $60.8 million in the prior corresponding period. EBITDA margin for the Group continued to increase 29.3%, i.e., by 330bps on PCP basis. Moreover, the cost out programs delivered savings as anticipated.

CPU maintained impressive performance from the most profitable business of Register Maintenance and Corporate Actions. The revenue increased by 5.4% with strong EBITDA growth of 16.0% and margin improvement to 36.9%, up 330bps. The company revitalised the register maintenance. New global and regional management, sales and marketing initiatives and product development re-energised the business performance and led to an improvement in results.

The company has maintained a strong balance sheet. The net debt to EBITDA leverage ratio stood at 1.88x, which is below the midpoint of the target range of 1.75x to 2.25x. The company has delivered healthy returns with ROEof 27.1%, up 40 bps and ROIC (return on invested capital) of 14.9%, down 330 bps, indicating increased investment capital..

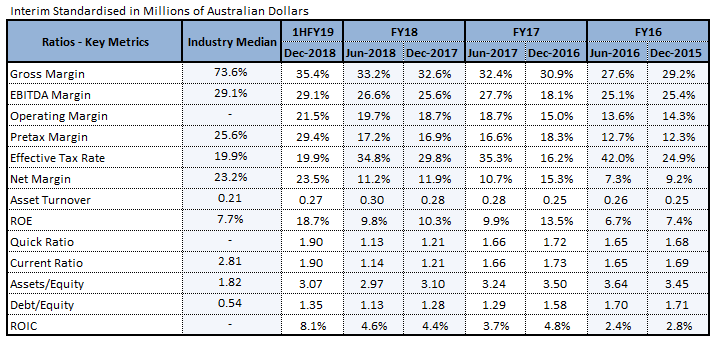

Key Ratios (Source: Thomson Reuters)

1H19 Results Summary (Source: Company Reports)

Key Risks: The business operates in highly regulated markets around the world and the success of the company can be impacted by changes to the regulatory environment and the structure of these markets. It focuses on regulatory developments globally and plays an active role in consulting with regulators on changes which might impact its business. The financial performance of the company each year is underpinned by significant annuity revenue, however, a material proportion of revenue is dependent on factors outside its control.

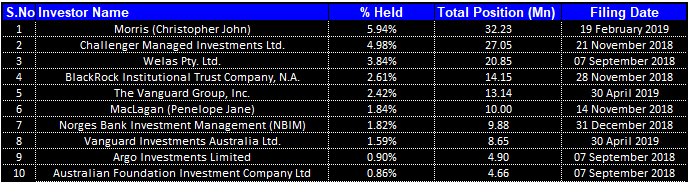

Top 10 Shareholders: Top ten shareholders of the company form around 26.80% of the total shareholding as highlighted in the below table. Morris (Christopher John) holds maximum interest in the company with a stake of 5.94% followed by Challenger Managed Investments Ltd. and Welas Pty. Ltd. with a stake of 4.98% and 3.84%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

Guidance & Outlook: During the AGM of November 2018, the company stated that it expects FY19 Management EPS in constant currency to increase by around +10% as compared to the prior year. However, given the 1H19 result, it expects Management EPS for FY19 in constant currency to increase by around +12.5% on FY18. The tax rate of the group is expected to be slightly lower in FY19 (i.e., ~27.5%) as compared to FY18 (28.3%). The revenue (excluding margin income) from Corporate Actions and event-based activities are assumed to be lower in 2H FY19 than in the prior corresponding period.

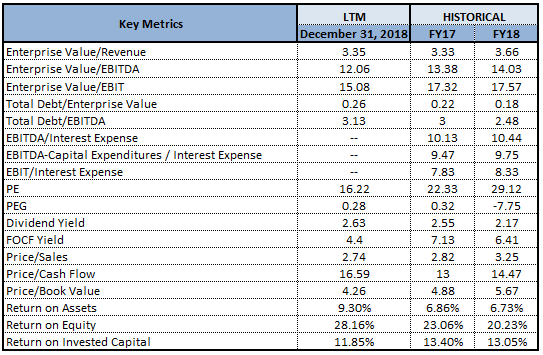

Key Valuation Metrics (Source: Thomson Reuters)

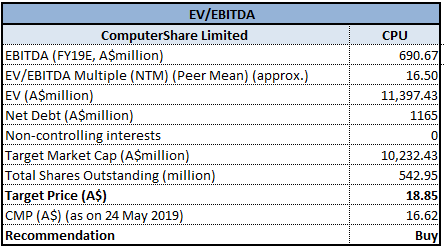

Valuation Methodology- EV/EBITDA Multiple Approach (NTM):

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: Meanwhile, CPU’s stock has fallen 4.93% in the past three months as on 23 May 2019 and is trading close to its 52-weeks low price of $16.250 with reasonable P/E multiple of 16.44x, proffering a decent opportunity for accumulation. Besides this, as a result of decent fundamentals and improving financials in 1HFY19, the company’s annual dividend yield stood at respectable levels of 2.5% as at 24 May 2019. Moreover, the company has a compliant and scalable regulatory and transactional operating model that is difficult to replicate. The company is driving growth and market expansion through the structural changes. A strong global footprint, deriving synergies from acquisitions, coupled with a strong financial performance has underpinned the robust balance sheet and a controlled leverage position. Hence, considering the aforesaid factors, we recommend a “Buy” rating on the stock at the current market price of $16.620 (down 0.894% on 24 May 2019).

.png)

CPU Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...