Company Overview - Cooper Energy Limited is a petroleum exploration and production company. The Company produces oil from the Cooper Basin, Australia and the South Sumatra Basin, Indonesia. The Company operates through four geographical segments. Australian Business Unit, which includes Exploration and evaluation for oil and gas, development, production and sale of crude oil in a number of areas in the Cooper Basin located in South Australia; African Business Unit, which include exploration and evaluation for oil and gas in the Bargou, Nabeul and Hammamet permit area off the coast of Tunisia; Asian Business Unit, which include Asian business unit involved the production and sale of crude oil from the Tangai-Sukananti KSP, and European Business Unit. Effective May 15, 2014, the Company acquired a 65% interest in Basker Manta Gummy field.

Analysis – Cooper Energy is an ASX listed exploration and production company producing approximately 0.6Mb of oil per annum. The asset portfolio covers acreage in the Cooper, Otway and Gippsland basins of Australia, South Sumatra, Indonesia and the Gulf of Hammamet, Tunisia. Production is underpinned by prospective Western Flank developments in the SA Cooper Basin, where success rates and operating margins are high. Although COE is not exposed to the big field upside event immediately to the north, the acreage contains extensive incremental opportunities in both oil and gas particularly at the Worrior field where recent development and appraisal drilling has been successful to the upside.

Cooper Basin Exploration & Development (Source - Company Reports)

Cooper Basin Exploration & Development (Source - Company Reports)

The most immediate catalyst is the potential sale of Tunisian assets with a divestment process now underway. The assets are non-core and have existing discoveries subject to appraisal and definition. We suggest a look through value could be as high as $60 million and that value would be an excellent outcome in terms of expectations and adding to cash. The recent Gippsland Basin acquisition provides the company with an appraisal and development opportunity, building on its southern state gas strategy. We suggest first production may be delivered in FY17 however we feel there is some potential to accelerate work programmes here should the commercial opportunities warrant it. The company has an elephant on the register with Beach Energy holding 18%. At this stage we don’t see a rationale for this evolving into a takeover opportunity, however the company is aligned across the southern assets, especially in the Otway Basin where drilling success could be the corporate catalyst.

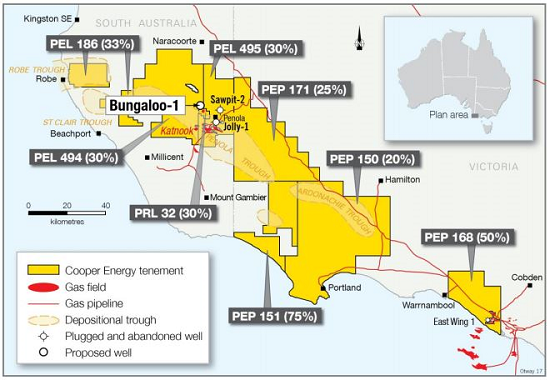

Otway Basin (Source - Company Reports)

Otway Basin (Source - Company Reports)

Beach currently holds an 18.41% interest in Cooper energy at an average entry price of $0.455 per share. Notwithstanding the potential positives, we see a takeover as unlikely at this stage. We can see reasons for Beach seeking control of cooper energy: 1- Common assets in the Otway, Gippsland and Cooper Basins with ongoing drilling activity. 2-The sell down of the Tunisian assets could deliver a significant increase in the cash backing of the shares. 3 – Continued strong oil production performance from PEL 92 (Cooper Basin). Cooper Energy has carried a high cash balance for some years at 30 – 40% of its market capitalization. In the last three years, the cash balance has been as high as $89mn and divestment in Tunisia could revisit these high cash levels. We note expenditure opportunities upcoming in the Otway Basin but see it as unlikely to utilize a large percentage of the cash. There is no specific historical evidence to suggest COE will be actively seeking transactions although cash balances do offer capacity to expand the asset base. Any deal will need to be evaluated on its merits but the company may feel some pressure to put its cash to work. The recent Basker acquisition may point to a growing corporate strategy.

Gippsland Basin (Source - company Reports)

Gippsland Basin (Source - company Reports)

We see material Cooper Basin upside coming from PEL93 (COE 30%) where Worrior – 8 recently tested 0.7MMscfd and over 800bpd of oil. An emerging southern gas position through South Australia and Victoria could deliver a significant growth play leveraging the continuing supply squeeze and rising gas prices. We see latent value in the Otway Basin assets, whilst the recent Basker acquisition could drive some medium term commercial opportunities; however these plays are early stage options.

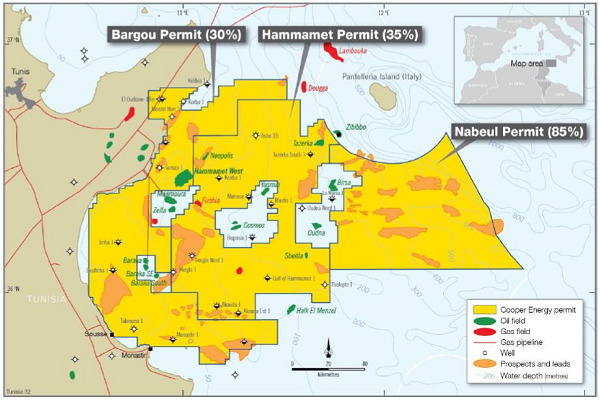

Tunisian Assets (Source - Company Reports)

Tunisian Assets (Source - Company Reports)

COE offers investors a predictable earnings base from its PEL92 permit held in joint venture with Beach Energy. We see the company’s Worrior oil and gas field opportunity as undervalued and Hammamet West in Tunisia as deeply discounted by the domestic market. To realize the value of its Tunisian plays, COE has opened a data room to aid in the divestment of these assets, which could deliver a $60 - $70mn cash injection on our estimates. The current share price suggests the market is ascribing no value to this opportunity. Whilst COE is perhaps less leveraged to cooper basin upside than its peers, PEL 92 has delivered reliable production and further discoveries since a 5,000bd pipeline was installed in late 2007.

COE Daily Chart (Source - Company Reports)

COE Daily Chart (Source - Company Reports)

We believe Beach’s position is to block unwanted Western Flank partners or simply a trading position. We draw this conclusion through analysis of Beach’s stake in Drillsearch and Beach having previously invested and divested in the equity of peers. With an enterprise value of $135mn, COE is well within BPT’s funding capacity even allowing for a control premium. However, just because a deal can happen does not mean it will. The corporate attraction may reside in the southern gas plays, particularly the Otway Basin where COE does offer a largely contiguous acreage exposure along a continuous trend through SA and Victoria.

We highlight upside potential to volumes from the Worrior Field given the exceptional productivity of the reservoir. Production growth beyond Worrior will require exploration success or additional PEL92 infrastructure. Whilst we are bullish on the Worrior/PEL93 prospectivity, we need to see further drilling success to lift production forecasts. We forecast strong earnings growth in 2014 driven by strong production and high pipeline utilization on the western flank. COE has run a significant cash balance since FY12, which we project to continue. In addition, the Tunisian divestment could deliver substantial upside. The company has also put in place a bilateral facility agreement with a domestic bank for funds totaling $40mn.

As per the quarterly report for March 2014 quarter the YTD production was up 35% to 456 kbbl and sales revenue of $56 million already higher than FY13 full year sales revenue of $53 million. Sales revenue is up 3% on the previous quarter and up 47% on the March 2013 quarter. Production is up 1% on the previous quarter and up 23% on the March 2013 quarter. FY14 production range increased to 575 kbbl to 600kbbl (previously 540kbbl to 580 kbbl). Financial assets rose 20% over the quarter to $79.7 million at 31

st March 2014. We like the Cooper Energy story and reiterate our buy on the stock at the current price of $0.49.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Please wait processing your request...

Please wait processing your request...