Kalkine has a fully transformed New Avatar.

Company Overview - Cooper Energy Limited is an upstream oil and gas exploration and production company whose primary purpose is to secure, find, develop, produce and sell hydrocarbons. The Company's operations consist of oil production in the Cooper Basin (onshore Australia) and the South Sumatra Basin (onshore Indonesia); pre-development activities associated with the Sole and Manta gas fields in the offshore Gippsland Basin, and exploration for oil and gas in the Cooper, Otway and Gippsland basins. The Company's Australian Business Unit includes exploration and evaluation for oil and gas, development, production and sale of crude oil in various areas in the Cooper Basin, Gippsland Basin and Otway Basin. It holds interests in approximately three exploration licenses, over 30 retention licenses and approximately 10 production licenses in the South Australian Cooper Basin. The Company holds interests in over four exploration licenses and a retention license in the onshore Otway Basin.

COE Details

Agreement on Tunisia operations: Cooper Energy Ltd (ASX: COE) has finalised the process and agreements for completing their operations in Tunisia, complying with their earlier announced strategy of concentrating on the gas growth projects in Australia. For this, Cooper Energy has elected not to renew the Bargou permit and transferred its 30% interest (sole remaining Tunisian interest) and operatorship effective from 7th November to joint venture partner Dragon Oil Ltd, via a deed of assignment. COE would continue to perform the operator responsibilities under contract until the Hammamet West well abandonment is completed, which is expected by end of January 2017. COE’s share of the abandonment cost as per the FY16 accounts is expected to be less than US$200,000. But, this would not involve any cash payment by either party. Moreover, COE has agreed to the terms of the settlement of the Hammamet Joint Venture dispute. The settlement resolves the dispute between the COE’s wholly owned subsidiary CE Hammamet Ltd and the Hammamet Joint Venture, related to any ongoing liability to pay for work obligations that may be undertaken during the extension period of the permit after COE’s withdrawal. Meanwhile, as per the settlement deed, if Hammamet Joint Venture chooses to withdraw from the permit, COE will fund a 35% share of any agreed exit fee up to an agreed, undisclosed, ceiling, but COE does not require any immediate or firm cash payment. After the settlement, there is no outstanding matter left regarding the Hammamet permit. Additionally, COE would stop all the operations in Tunisia in January after finishing the Hammamet West.

Agreement with EnergyAustralia: COE has signed a binding gas sales agreement with EnergyAustralia for supplying 5 Petajoules (PJ) per annum from the Sole gas field for a minimum of 5 years. The agreement also has a provision for a 3-year extension which is subject to the parties' agreement. The agreement is upon the condition which requires the finishing of the transaction for COE to acquire Santos Ltd.’s Victorian Gas assets and an affirmative final investment decision (FID) for Sole. Moreover, the acquisition of Santos’ share in Sole would lead to COE having Contingent Resources (2C) of 2411 PJ of gas. The agreement with EnergyAustralia is the fourth one signed by COE for the field and would take the annual contracted quantity to 14.6 PJ of the 25 PJ annual production which is expected from the field for the first 8 years. COE is expected to commit up to 85% of the annual volume prior to FID and is in discussions with gas buyers on sale agreements for the remaining quantity. Additionally, COE has shown keen interest in contracting gas from Sole and expects to finalize additional off-take contracts within the next few months. COE has received commitments from major energy retailers and industrial users, and is close to finalizing a quality gas contract portfolio ahead of FID for the Sole project. Overall, Sole FID is expected to occur in the March quarter 2017, and the first gas from the project is scheduled by March 2019. The supply to EnergyAustralia under the agreement would start from January 2020.

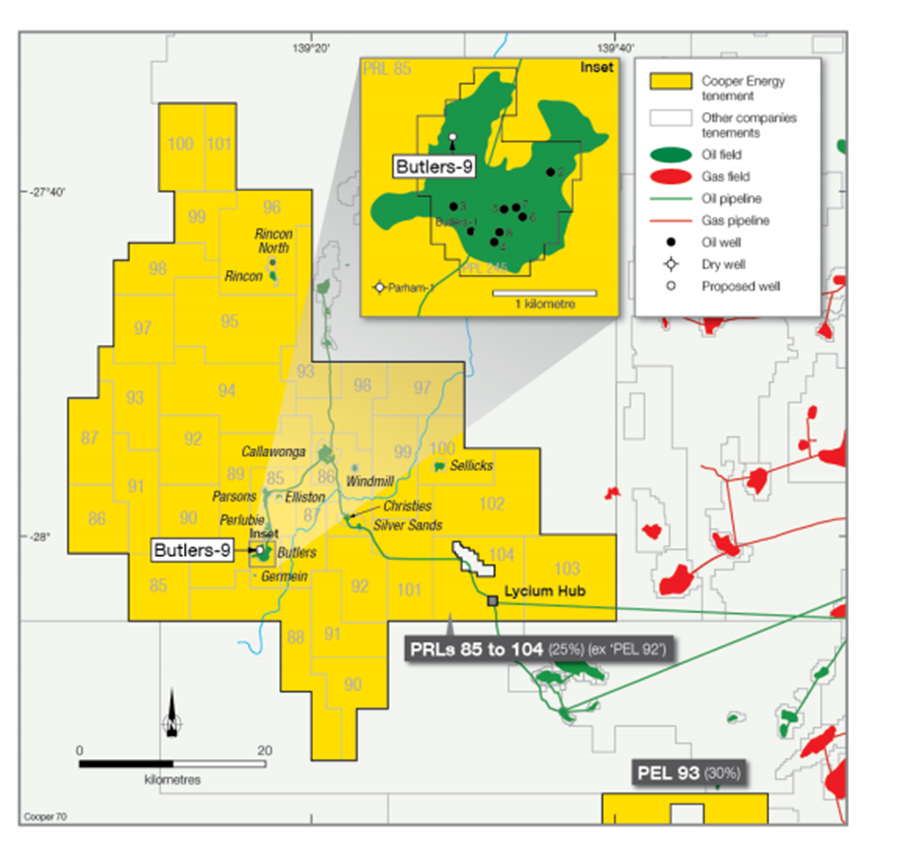

Butlers-9 highlights: COE has recently posted that Butlers-9, an oil appraisal well located in PPL 245 Cooper Basin, South Australia, in which COE has 25% interest, is being plugged and abandoned after reaching a total depth of 1,810 metres in the Merrimelia Formation. Minor hydrocarbon shows are also recorded in the well. Major target from Butlers-9 is the Namur Sandstone, which is the main oil-producing reservoir in this field, as well as in the Callawonga, Parsons, Perlubie and Christies fields.

Butlers-9 in PPL 245 Cooper Basin, South Australia (Source: Company Reports)

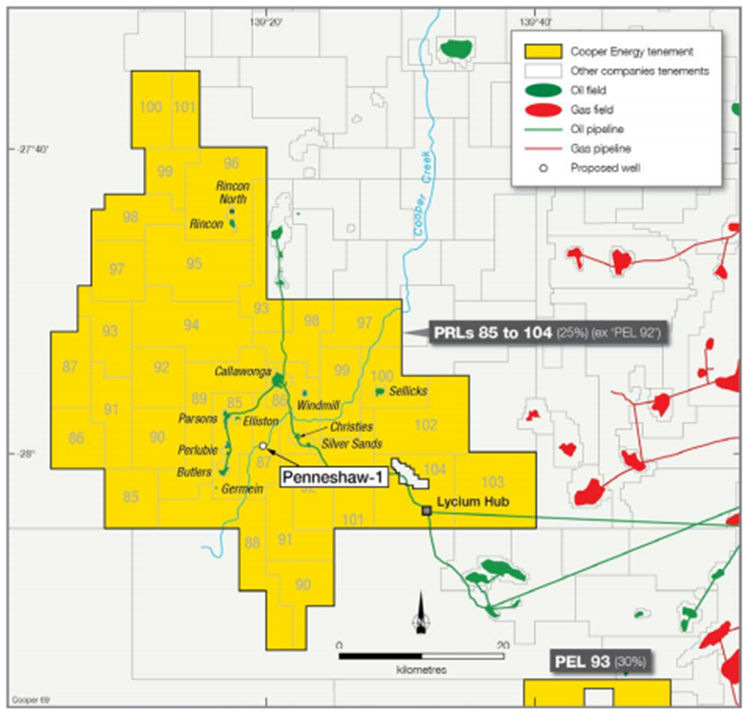

Penneshaw-1 been spudded: COE has spudded Penneshaw-1, an oil exploration well located at PRL 87 on the western flank of the Cooper Basin, South Australia (COE has 25% interest in PRL 87) and the rig drilling is ahead at 62 meters in 12- ¼ inch surface hole. Moreover, the primary target of Penneshaw-1 is the Namur Sandstone, which is the oil producing reservoir in several adjacent fields (Butlers, Callawonga, Parsons, Perlubie and Christies). The secondary targets of Penneshaw-1 are the Mid-Namur Sandstone, Birkhead Formation and Hutton Sandstone, which are oil-bearing in the Christies and Silver Sands fields. Further, after Penneshaw-1, the rig will move to drill Butlers-9 that has the appraisal potential oil volume in the undrilled north-west quadrant of the Butlers oil field.

Location of Penneshaw-1, PRL 87, Cooper Basin (Source: Company Reports)

Funds raised through Retail Entitlement Offer: COE has raised funds of over $62.6 million via Retail Entitlement Offer and the same will be used to partly fund COE’s acquisition of the Victorian Gas Assets from Santos. This is done after COE had raised over $41.1 million via institutional component of the Entitlement Offer.

Subdued FY 16 Financial Performance: COE in FY 16 has reported a statutory net loss of $34.8 million and an underlying net loss after tax of $2.8 million due to the impact on asset valuations and weaker revenue on the back of lower oil prices. On the other hand, COE reported for the direct operating cash costs of A$29.71 per barrel, and cash generated from operating activities of $7.9 million indicating for group’s strength of Cooper Basin oil operations despite low oil prices.

Strategies after finishing Victorian gas asset acquisition: After completing Victorian gas asset acquisition (scheduled to occur by early 2017), COE aims to generate the major share of its revenue from the sale of gas under stable long-term contracts, instead of the current sole reliance on oil. This would mainly cut the dependence to the oil price volatility. There is an expectation that the production for FY17 would enhance from over 0.3 million barrels of oil equivalent to 1 million barrels of oil equivalent, 70% of which is expected to be gas. Moreover, the total Australian proved and probable reserves would rise from the 1.3 million barrels as at 30 June 2016 to about 10 million barrels of oil equivalent. COE is expected to acquire proved and probable gas reserves estimated to be 54 petajoules at completion as well as an additional 121 petajoules of 2C Contingent Resources of Gas.

Production Outlook (Source: Company Reports)

Commercialization of Gippsland Basin gas resources: The Gippsland Basin interests comprise the Orbost Gas Plant, Sole gas field, the Basker and Manta resources and, on completion of the Santos asset acquisition, the Patricia Baleen gas field and associated infrastructure. COE has plans to develop Sole to supply gas from the March quarter of 2019.

Portfolio Adjustment: In FY 16, COE has divested its Indonesian exploration assets and, in Tunisia, the group withdrew from the Hammamet Joint Venture and agreed terms to exit the Nabeul permit. Subsequently, COE has signed the agreement with Bass Strait Oil Company for the divestment of its remaining Indonesian interest, the Tangai-Sukananti KSO with a completion date in January 2017. Lately Bass updated that acquisition of COE’s 55% operated interest in Tangai-Sukananti production assets will transform Bass into SE Asia-focused oil & gas production company.

Stock Performance: COE stock price rose 74.3% in the last six months (as of December 20, 2016). The effective date for the COE acquisition of Santos’ Victorian gas assets is 01 January 2017, which would substantially add value to the company. Other latest moves are also expected to boost the performance. For instance, Casino/Henry is expected to bring in value considering COE’s 45PJ of uncontracted 2P gas. Then, EnergyAustralia has a strong credit rating with a positive outlook and COE’s move on binding gas sales agreement indicates for de-risking a project from a debt funding perspective. We believe the bullish momentum in the stock would continue in the coming months as the recent development on production cut from OPEC and non-OPEC member is driving the oil prices. We give a “Buy” recommendation on the stock at the current price of – $ 0.35

COE Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...