Kalkine has a fully transformed New Avatar.

Company Overview - Cooper Energy Limited is an upstream oil and gas exploration and production company whose primary purpose is to secure, find, develop, produce and sell hydrocarbons. The Company's operations consist of oil production in the Cooper Basin (onshore Australia) and the South Sumatra Basin (onshore Indonesia); pre-development activities associated with the Sole and Manta gas fields in the offshore Gippsland Basin, and exploration for oil and gas in the Cooper, Otway and Gippsland basins. The Company's Australian Business Unit includes exploration and evaluation for oil and gas, development, production and sale of crude oil in various areas in the Cooper Basin, Gippsland Basin and Otway Basin. It holds interests in approximately three exploration licenses, over 30 retention licenses and approximately 10 production licenses in the South Australian Cooper Basin. The Company holds interests in over four exploration licenses and a retention license in the onshore Otway Basin.

.PNG)

COE Details

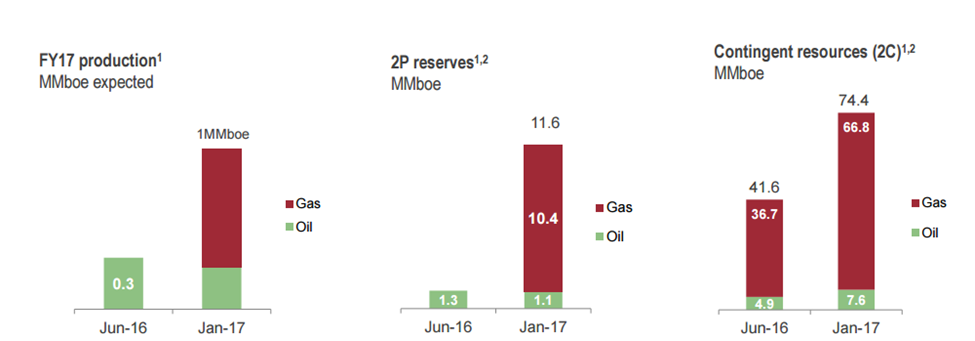

Approved Sole gas project: Cooper Energy Ltd.’s (ASX: COE) Board of directors has approved Sole gas project while the finalization of financing has started with a fully underwritten equity raising of over $151 million. Sole gas project would develop the Sole gas field located in VIC/ L32 in the Gippsland Basin offshore Victoria to supply 25 PJ per annum to gas users in south-east Australia. Cooper Energy has the 100% interest holder in the Sole gas field. The Gas produced from the Sole gas field will be piped to the Orbost Gas Plant (formerly known as Patricia Baleen gas plant), from where the gas will be supplied to customers through the Eastern Gas Pipeline. Meanwhile, the group got a long-term gas sales contract with a portfolio of customers (including AGL, EnergyAustralia, Alinta Energy and O-I Australia) to support the development of the field while retaining a significant share of annual output for availability to supply shorter term sales. Moreover, APA Group is expected to acquire and undertake all the capital expenditure related with the Orbost Gas Plant. APA Group and COE have executed a non-binding Heads of Agreement in February 2017, according to which COE and APA Group have been in advanced negotiations to conclude the arrangements pursuant to which APA Group would acquire, upgrade and operate the Orbost Gas Plant. Additionally, COE would solely undertake the upstream development, which has an expected capital expenditure of $355 million. For this, the fully underwritten equity raising of over $151 million has been expected to mostly cover the equity funding requirement for the Sole gas project. In addition, COE is highly confident of securing debt finance for the remaining funding requirement of the Sole gas project during the June quarter 2017. The first gas from the Sole gas project is planned to be delivered to the Orbost Gas Plant in the March quarter of 2019. Furthermore, the finalization of funding and Final Investment Decision (FID) of the Sole gas project would speed-up the 43 million barrel of oil equivalent (boe) uplift to COE 2P reserves, which represents an increment of nearly 400% to prove and probable reserves as at January 01, 2017 of 11.6 million boe. The first full year of operation from the Sole gas project is expected to lift COE’s annual production to more than 6 million boe that compares 5 times to guidance for FY17 of 1 million boe.

.png)

Sole Gas Project (Source: Company Reports)

Raising of fund through equity: The groupundertook a move to raising $151 million for financing Sole gas project which comprised an institutional placement of 150 million new fully paid ordinary shares in COE to raise approximately $47 million and a 1 for 2 accelerated non-renounceable entitlement offer of new shares. Further, the entitlement offer comprised of an accelerated institutional component and a retail component, which opened on April 05, 2017, and is to close around April 21, 2017. Both the Institutional Placement and Entitlement Offer were priced at $0.315 per new share. Moreover, Cooper Energy has raised $116 million from the completion of placement and institutional entitlement offer. Now, the fully underwritten retail entitlement offer will raise approximately $35 million. There was full participation from eligible shareholders in institutional entitlement offer and the placement got multiple times oversubscribed.

.png)

Use of Proceeds (Source: Company Reports)

Incurred loss after tax in 1H 2017: Cooper Energy has reported underlying loss after tax of $3.5 million in the first half 2017 ended December 31, 2016 while the statutory loss after tax was $8.2 million, reduced from FY16 H1 loss of $34.1 million. The statutory result was posted after significant non-operating items of $(4.7) million, primarily due to a provision associated with exit from Tunisian exploration licenses and impairments to Indonesian oil properties, the sale of which is due to complete imminently. Therefore, the company had reported loss in 1H FY17 due to the lower oil sales volumes and additional costs related with the acquisition and integration of gas assets during the period. Moreover, the statutory loss is accompanied by the transformational change that has delivered substantial upgrades to the group’s expected production, reserves and the company’s scope of operations for this year. The changes have included the Cooper Energy’s acquisition of Santos’ Victorian gas assets, and the near completion of COE’s withdrawal from international operations in February 2017. The group’s portfolio is now concentrated on Australia and, from January, with the large majority of the company’s revenue generated by the production of gas for south-east Australia. Cooper Energy’s production for the current year has been upgraded by more than three times to 1 million boe and the Australian reserves have risen more than eight times to exceed 11 million boe. In addition, Cooper Energy is expecting significant growth this year, with a 6-year growth trajectory offered by the existing assets. Based on the current plans and equity interests, this can take COE’s production from last year’s output of 0.3 million boe to exceed 10 million boe by 2022.

.png)

First half of 2017 Financial Performance (Source: Company Reports)

Improving outlook: The group had also announced about adding Otway gas production during January 2017 to June 2017 period which would rapidly boost their gas portfolio. Accordingly, the group’s Gas would constitute 75% of expected production in fiscal year of 2017. The group would be adding 60 PJ of Otway Basin gas 2P leading to the Gas comprising 90% of 11.6 MMboe. The group’s Australian 2C contingent resources is expected to rise by 79%. The group would be adding 128 PJ gas contingent resources (2C) from Gippsland. The Sole FID could lead to 43 MMboe rise in gas reserves. The group is translating HoA with APA to formal agreement. As per the Uncontracted Otway gas, the group believes the contracting gas would supply from March 2018. COE believes to get more new agreements by winter 2017. The group is working to appointment as Operator for Gippsland and Otway. Meanwhile, the group is working to focus on its cost efficiencies while intends to divest certain part of Gippsland Basin portfolio. Apart from this, the group intends to pursue Manta exploration.

Projections for 2017 (Source: Company Reports)

Stock Performance: Cooper Energy is planning for a six-year growth trajectory with a potential capacity for production for over 20 times as compared to the FY16 levels. Accordingly, the group would now derive a major Gas production. Meanwhile, the group’s new assets and production would lead to a more than two times growth in fiscal year of 2017 production as compared to the FY16 production. The group forecasts FY19 production to grow more than five times against FY16 production. Cooper Energy expects their FY22 production to be more than twenty times as compared to FY16 production. For the half year ended at June 17, the group intends to achieve several milestones which would support their potential targets and value transformation. Meanwhile, the share price of COE has risen over 14.39% in the last six months (as of April 04, 2017) and we believe this momentum could continue on the coming months. The stock was in the trading halt session state until March 31, 2017. COE returned to trading with the announcement of completion of its institutional offer ($116 million raised with full participation of shareholders) and retail offer booklet has now been dispatched. COE stock has recently been added to All Ordinaries Index, effective March 20, 2017. We give a “Speculative Buy” recommendation on the stock at the current price of – $ 0.35

.png)

COE Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...