Kalkine has a fully transformed New Avatar.

Company Overview: Coronado Global Resources, Inc. is an Australia-based company that produces, markets and exports a range of metallurgical coals. The Company owns a portfolio of metallurgical coal mines in Queensland, Australia and in the states of Pennsylvania, Virginia and West Virginia in the United States. It operates four segments: Curragh, Buchanan, Logan and Greenbrier. Curragh segment consists of mining assets and operations located in Central Queensland, Australia, produces a variety of metallurgical coal. Greenbrier segment consists of coal mining facilities in the south-eastern region of West Virginia, produces hard coking coal, specifically mid-volatility coal. Logan segment consists of mining interests, coal reserves, and facilities located in Logan County, West Virginia, produces hard coking coal, specifically high-volatility coal. Buchanan segment consists of mining assets and operations located in Buchanan County, Virginia, produces hard coking coal, specifically low-volatility coal.

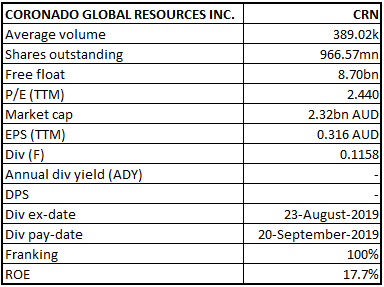

CRN Details

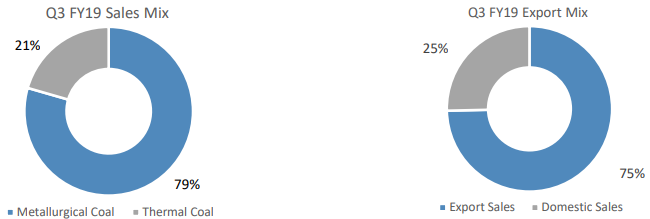

Saleable Production for YTD FY19, up 4.9% on pcp: Coronado Global Resources Inc. (ASX: CRN) is involved in the development and operation of premium quality metallurgical coal mines in Queensland, Australia (Curragh) and in the states of Pennsylvania, Virginia and West Virginia (Buchanan, Logan, Greenbrier) in the United States of America. It is one of the largest metallurgical coal producers globally by export volumes and the largest metallurgical coal producer in the United States by production volumes. Looking at the past performance over H1FY17 to H1FY19, total revenue of the company has grown from $396.2 Mn in H1FY17 to $1,234.3 Mn in H1FY19. Group’s profit after tax grew from $90.9 Mn in H1FY17 to $214.3 Mn in H1FY19. Group’s total debt reduced from $674.9 Mn in H1FY18 to $18.9 Mn in H1FY19. Company’s metallurgical coal sales proportion stood at 79% of the total sales mix in September’19 Quarter, consistent with the previous quarter. Out of total sales, export sales stood at 75%, a decrease of 4.1% than the previous quarter.

The company has achieved significant operating efficiencies at its Curragh mine since its acquisition in March 2018 and will continue to benefit from reduced operating costs. The Buchanan mine ranks amongst the lowest cost metallurgical mines in the U.S., and its management team has a track record of operating these assets efficiently. With a competitive and low-cost operating structure, low gearing and suite of highly sought-after, quality metallurgical coal products from the US domestic and global seaborne markets, the company remains optimistic for its long-term growth prospects.

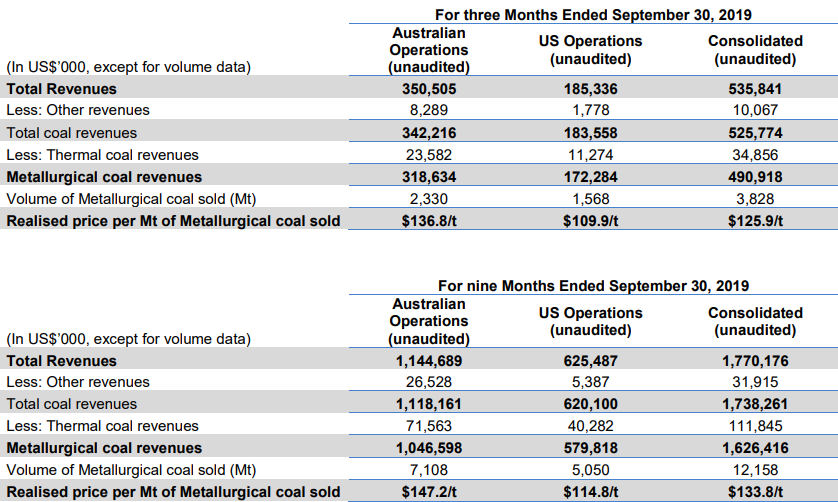

Key Highlights of September’19 Quarter: Revenue for the period was reported at $536 Mn (unaudited), and revenue for the last nine months stood at $1,770 Mn (unaudited). Year-to-date mining cost per tonne sold was reported at $52.2 per tonne (unaudited). Mining costs per tonne sold increased on a year-to-date basis due to lower group saleable production in the third quarter of CY19. Year-to-date capital expenditure for the period was reported at $117.4 Mn (unaudited).

Q3FY19 Sales and Export Mix Figures (Source: Company Reports)

Net debt as on September 30, 2019 was reported at $276 Mn, following the payment of the interim distribution of $0.41 per CDI (Chess Depository Instrument), which included dividend of $0.112 per CDI and capital return of $0.298 per CDI. The interim distribution amounted to $396.3 Mn and was paid to shareholder on September 20, 2019. The company successfully increased syndicated facility agreement (SFA) from $350 Mn to $550 Mn and extended maturity by an additional 12 months to February 2023.

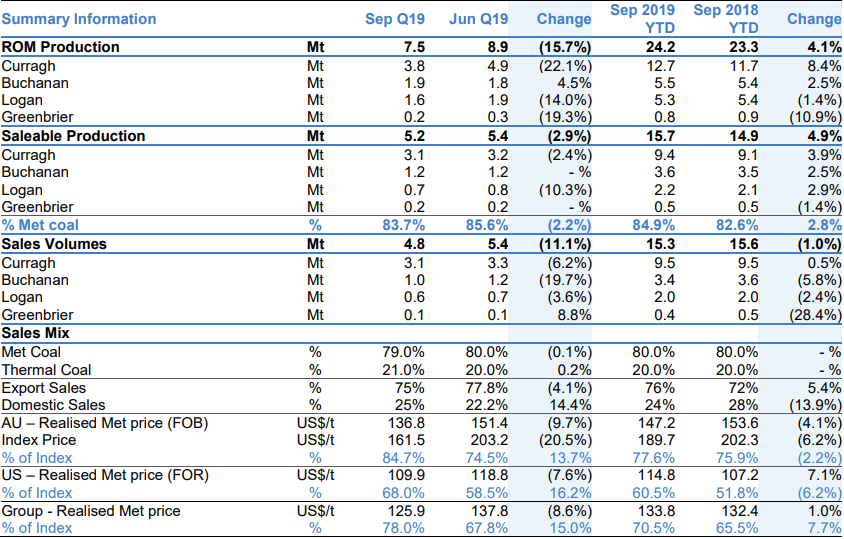

September’19 Quarter Key Metrics (Source: Company Reports)

Sep Qtr ROM Production at Buchanan Increased By 4.5% than Previous Qtr: Run-On-Mine (ROM) coal production decreased by 15.7% to 7.5 Mt as compared to the previous quarter. This was due to the scheduled maintenance shutdown of a dragline at Curragh and build of in-pit inventory. There is a significant raw coal inventory to support saleable production in the December quarter. ROM production at Buchanan stood at 1.9 Mt, 4.5% higher than the previous quarter, mainly due to favourable underground mining conditions, while Logan’s ROM production stood at 1.6 Mt, a decline of 14% than the previous quarter, mainly due to the suspension of thermal coal surface mining operations at Toney Fork.

In the quarter, Group’s saleable coal production decreased by 2.9% to 5.2 Mt as compared to the previous quarter. Saleable production at Curragh decreased by 2.4% to 3.1 Mt, due to planned maintenance at the Coal Handling Preparation Plant (CHPP). Saleable production at Buchanan for the period was reported at 1.2 Mt, consistent with the previous quarter, whereas Saleable production at Logan decreased by 10.3% than the previous quarter.

Group’s sales volume for the period was reported at 4.8 Mt, a decrease of 11.1% than the previous quarter. Sales volume at Curragh decreased by 6.2% to 3.1 Mt, as compared to the previous quarter, mainly due to the scheduled mine maintenance activities and lower train availability because of planned track and port facilities maintenance by the respective operators. Sales volume at Buchanan decreased by 19.7% to 1 Mt as compared to the previous quarter, mainly driven by a slowdown in demand in Europe, Brazil and the impact of the trade tariffs on exports to China. Sales volume at Logan decreased by 3.6% to 0.6 Mt than the previous quarter on the back of suspension of operations at the Toney Fork surface mine.

Realized metallurgical coal price for Curragh decreased by 9.7% to $136.8 per tonne (Free on Board (FOB)), as compared to the previous quarter. For the US operations, realized metallurgical coal price decreased by 7.6% to $109.9 per tonne (Free Onboard Rail (FOR)) as compared to the previous quarter.

In safety terms, the Group has outperformed the national average in both Australia and the US. Company’s Total Reportable Injury Frequency Rate (TRIFR) in Australia at the end of the quarter was reported at 5.46. Total Reportable Incident Rate (TRIR) in the US for 12 months rolling average period was reported at 1.34.

Data for Quarterly Production and Sales Performance (Unaudited) (Source: Company Reports)

Recent Update:

On September 25, 2019, the company provided an update to the market about its CY19 profit guidance. The company reaffirmed its production, operating cost and capital expenditure guidance for CY19, based on its ongoing improvements in the operating performance of its assets. Due to correction in the metallurgical coal price, the company has revised its EBITDA guidance range to $687 Mn - $737 Mn from the earlier guidance of $737 - $807 million. The assumption for this revision includes spot price of ~$140 per tonne (average) for the remaining period of CY19, which is below the spot price of $160 per tonne in the first half of CY19. The assumption also included higher than normal inventory levels in the US as reserves to gain margin in times of coal price recovery.

FY19 Guidance Data (Source: Company Reports)

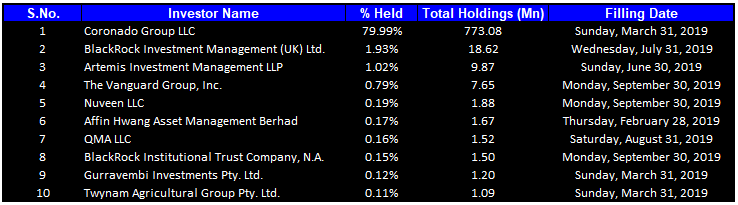

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 84.64% of the total shareholding. Coronado Group LLCand BlackRock Investment Management (UK) Ltd. hold maximum interests in the company at 79.99% and 1.93%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

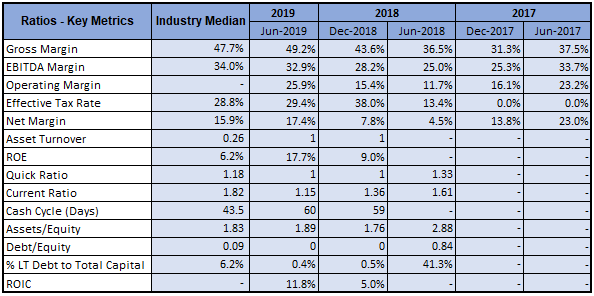

A Quick Look at Key Metrics: Its gross margin and net margin for H1FY19 stood at 49.2% and 17.4%, better than the industry median of 47.7% and 15.9%, respectively, implying decent fundamentals for the company. Its ROE for H1FY19 stood at 17.7%, better than the industry median of 6.2%, which implies that the company has generated better returns for its shareholders than its peer group. Its long-term debt to total capital for H1FY19 stood at 0.4%, lower than the industry median of 6.2%.

Key Metrics (Source: Thomson Reuters)

Key Risks: The company has no control over uncertainties, especially external factors such as general economic conditions, international events and circumstances, competitor actions, government actions and regulations, fluctuation in commodity prices, etc.

What to Expect: As per the release, a drilling and seismic exploration program was approved during the first half of CY19 to identify potential underground resource at Curragh. In the September quarter, exploration work commenced. Additional core hole drilling at Pangburn-Shaner-Fallowfield (PSF) has been scheduled for the last quarter of CY19.

Coal Production Outlook: During the September’19 Quarter, the Platts PLV coking coal price declined from $195 per tonne to around $137 per tonne, however, the price rebounded to $150 per tonne in the early October. Despite port restrictions affecting Australian coal exports to China, demand for high grade Australian coking coal is expected to remain high. Steel producers in markets such as Japan, Korea, India, Brazil and Europe were impacted by a slowdown in the demand for steel. Due to oversupply, spot coal inventory remains at higher side at Atlantic and Pacific basins. In order to balance the demand-supply gap, production is expected to reduce in order to arrest the coal price fall.

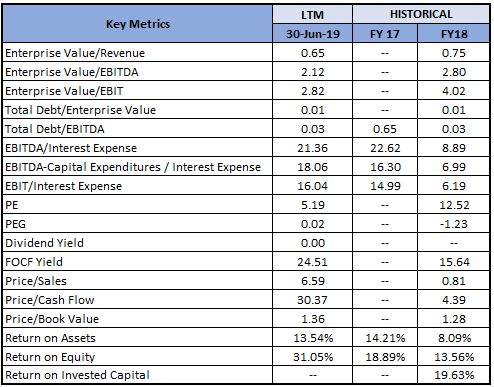

Key Valuation Metrics (Source: Thomson Reuters)

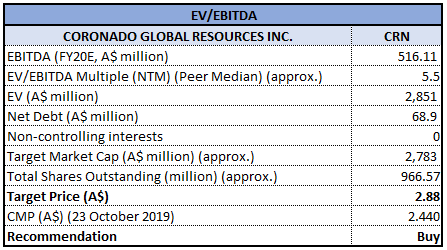

Valuation Methodology: EV/EBITDA Multiple Approach

EV/EBITDA Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The stock price fell by 2.43% in the past six months, however, the stock has delivered a positive YTD return of 2.44%. With low-cost operating structure and balance sheet capacity, company is well positioned compared to many of its peers to tolerate lower prices for longer period and pursue accretive acquisitions. Moreover, the macro-economic concerns especially the USA-China trade war, are expected to cool-off in the coming times. With this, the fundamental factors that support continued growth in demand for high-quality metallurgical coal in the long-term are expected to help coal producers in boosting their earnings, while risks related to commodities will still prevail to an extent. Looking at the business prospects over the long-term, we have valued the stock using a relative valuation method, i.e., Enterprise Value to EBITDA multiple, and arrived at a target price of low double-digit growth (in % term). Hence, we give a “Buy” recommendation on the stock at the current market price of A$2.440 per share, up 1.667% on October 23, 2019.

.jpg)

CRN Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...