Kalkine has a fully transformed New Avatar.

Company Overview: Coronado Global Resources Inc. (ASX: CRN) is a leading metallurgical coal producer, involved in the development and operation of premium quality metallurgical coal mines in Queensland, Australia (Curragh), and Virginia and West Virginia in the United States of America (Logan, Buchanan and Greenbrier). Several of the CRN’s mines are located near transportation infrastructure, allowing it to be a low-cost and reliable source of coal products for steelmakers globally. The company is committed to develop and introduce new coal production and energy generation technologies, that help reduce the environmental impact of its operations while continuing to meet global energy and steel demands.

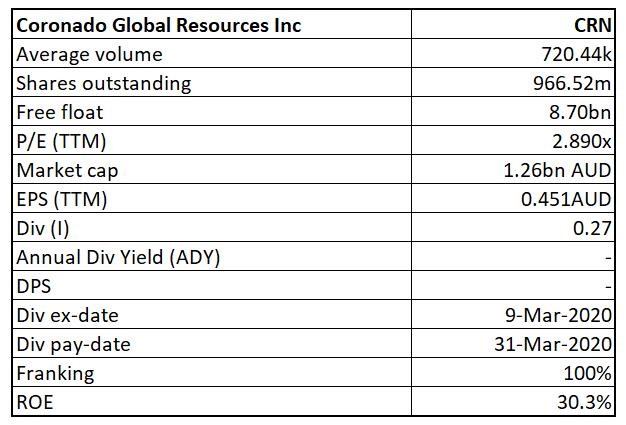

CRN Details

.png)

Diversified production base and significant Reserves and Resources: Coronado Global Resources Inc. (ASX: CRN) is a global producer, marketer and exporter of a full range of metallurgical coal. In Australia, the company’s operations consist of the 100%-owned Curragh producing mining property. CRN’s operations in the U.S. consist of three producing mining properties (Buchanan, Logan and Greenbrier), two development mining properties (Pangburn-Shaner-Fallowfield and Russell County) and one idle mining property (Amonate). The company was founded in 2011 with the intention of evaluating, acquiring and developing metallurgical coal properties. Over the years, the company has established itself as the largest metallurgical coal producer in the United States by production volume and the fifth largest metallurgical coal producer globally by export volume.

During 2015-2019, the company’s revenue increased at a CAGR of 76.62%. In the same time span, the company’s net income also witnessed a significant improvement, rising from a loss of US$55.25 million in 2015 to a profit of US$305.47 million in 2019..png)

Performance Summary (Source: Company Reports)

Currently, the company is mainly focused on the production of metallurgical coal for the North American and seaborne export markets. To support its operations, it has a proven and probable coal reserve totaling 680 MMt as of December 31, 2019.

CRN is focused on being a leading metallurgical company to supply the growth of the steel sector globally. In FY20, the company is putting a special emphasis on the implementation of the new Curragh mine plan which is targeted to increase Curragh’s saleable production to 15 Mt by 2023. Going forward, the company expects to generate sufficient cash from its operations together with available borrowing facilities to meet the needs of its existing operations, service its debt obligations and fund potential dividends. The company enjoys a diversified production base and significant Reserves and Resources, which position it well to grow organically over many years to come.

FY19 Performance Highlights: For FY19 or the year ended 31 December 2019, the company reported sales volume of 19.9 MMt (million metric tonnes), up 2.5 MMt higher than FY18, mainly due to the acquisition of Curragh on March 29, 2018 and realizing a full year of operations in 2019 from Curragh. In FY19, the coal revenue increased by $228.7 million to US$2,174.3 million, which includes a contribution of US$294.1 million from Curragh.

During the year, the company’s net income increased by US$190.9 million or 80.9% to US$305.5 million, driven by the increase in operating income, lower interest expense, lower selling, general and administrative and other expenses, and full-year operation of Curragh. Cash generated from operating activities totaled at US$477.4 million in FY19, up US$112.6 million from FY18, predominately due to the full twelve-month contribution of earnings from Curragh.

In FY19, the company increased the Syndicated Facility Agreement (SFA) from US$350 million to US$550 million extended the term of the facility by 12 months to February 2023. As at 31 December 2019, the company had a net debt of US$303.4 million which included US$26.6 million of cash and US$330.0 million of debt. During FY19, the company paid US$696.1 million in dividends and other distributions to stockholders. On 25 February 2020, the company declared a fully franked ordinary dividend of 2.5 cents per share..png)

FY19 Financial Performance (Source: Company reports)

Completion of New Curragh Mine Plan: One of the major achievements of the company during FY19 is the Completion new Curragh mine plan which is targeting 15 Mt of production per annum by 2023, providing an additional 6Mt of production above the Prospectus five-year forecast. From Curragh, the company reported an EBITDA increase of US$42.7 million in FY19, as compared to FY19, driven by higher sales volume and lower operating costs.

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 84.74%. Coronado Group LLC and BlackRock Investment Management (UK) Ltd. hold the maximum interest in the company at 79.99% and 1.96%, respectively..png)

Top 10 Shareholders (Source: Thomson Reuters)

Coal Market Outlook: Although the impact of Coronavirus situation on steel production is yet to be quantified, it is expected that the steel production in China will be curbed in the near-term as demand from the residential and infrastructure construction sectors is subdued due to the containment process implemented by the Government of China. In Australia and the US, the underlying demand for high-quality, low-impurity hard coking coal is expected to be continued as steel and coke makers in China continue to face tight environmental controls. In India, due to the several monetary initiatives in late 2019, the construction activities and investment in infrastructure are expected to rise. Along with this, the demand for steel-making raw materials is also anticipated to increase. Overall, the fundamental long-term demand for metallurgical coal in India remains sound.

Outlook: In FY20, the company is focused on implementing a new Curragh mine plan which will increase the Curragh’s saleable production to 15 Mt by 2023 and deliver incremental production growth of 2.0Mt in Curragh in the near term. The company has already executed the infrastructure contracts relating to rail and near-term port capacity. In addition to this, CRN also intends to improve the dragline performance and CHPP reliability at Curragh to further enhance the operations. For FY20, the company is expecting its Saleable Production to be in the range of 19.7 – 20.2 Mt and its capital expenditure to be between US$190 million – US$210 million. In FY20, the company expects to generate sufficient cash from its operations to meet the needs of its existing operations, service its debt obligations and fund potential dividends..png)

FY20 Guidance (Source: Company Reports)

A Quick look at Key Margin: In FY19, the company reported gross margin and net margin of 45.6% and 14.5%, respectively, both higher than the margins of prior year, demonstrating CRN’s improving profitability. The company currently has an asset turnover ratio of 1x, higher than the industry median of 0.58x. In FY19, CRN reported Return of Equity (ROE) of 30.3%, higher than the industry median of 9.3%..png)

Key Metrics (Source: Thomson Reuters)

Covid-19 Update: Recently on 30 March 2020, CRN informed that in response to the COVID-19 induced economic downturn in Europe, Brazil and the United States, it is temporarily pausing its U.S. operations, however, it will continue shipments to these regions from existing inventories of approximately 750,000 tonnes. The Curragh mine continues to operate to accommodate metallurgical coal export requirements of its key customers in India and the Asia Pacific. The company has assured that it has designed prudent measures to ensure that it remains in a solid financial position during the current challenging environment. The temporary halt to production at the U.S. mines might impact the saleable production guidance for FY20. However, the company is taking effective measures to reduce non-essential capital expenditure and preserve capital. Due to the significant stockpile of U.S. inventories and continued production from Curragh, the company’s operating cash flows are expected to remain positive.

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation(25).png)

Price to Earnings Multiple Based Approach (Source: Thomson Reuters), *1USD = ~1.58 AUD

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: In the last three months, the stock price of CRN corrected by 43.26% on ASX and it is currently trading near to its 52-week low price of A$0.935, providing a decent opportunity to investors for accumulation. The company currently enjoys a strong balance sheet coupled with a disciplined approach to capital allocation, positioning it well to deliver sustainable growth in the future. We have valued the stock using the price to earnings multiple based illustrative relative valuation method and arrived at a target price with double-digit upside (in % terms). For the purpose, we have taken peers like New Hope Corporation Ltd (ASX: NHC), Yancoal Australia Ltd (ASX: YAL), and Stanmore Coal Ltd (ASX: SMR), etc. Considering, the company’s decent FY19 performance, strong balance sheet, disciplined capital allocation approach, decent outlook, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of A$1.410, up by 8.046% on 15 April 2020.

CRN Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...