Kalkine has a fully transformed New Avatar.

Company Overview: Dacian Gold Limited (ASX: DCN) is an Australian gold mining company focused on optimising production to maximise cash flow while aggressively exploring its large tenement package in pursuit of organic growth opportunities. The company has a highly prospective land package in Western Australia, including the Mt Morgans operation, a very highly endowed gold field with numerous multi-million-ounce gold deposits. The company’s overall goal is to be the next Australian mid-tier gold producer and it intends to expand its production profile and increase scale while adding incremental mine life..png)

DCN Details

.png)

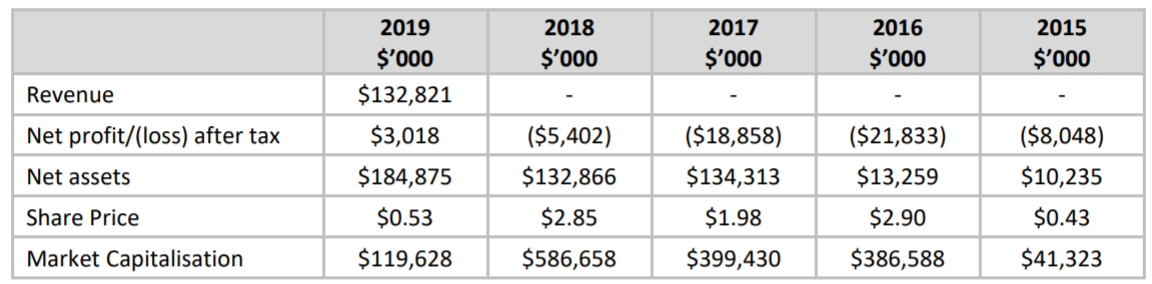

Transitioning into High Margin Gold Producer: Dacian Gold Limited (ASX: DCN) is an Australian mid-tier gold producer with a highly prospective land package in Western Australia. The company’s Mt Morgans Gold Operation (MMGO), located 750km northeast of Perth in Western Australia, is amongst a very highly endowed gold field with numerous multi-million ounce gold deposits. The company’s operation comprises a 2.5 Mtpa CIL treatment plant, the Westralia underground and the Jupiter open pit mining areas. DCN’s growth strategy is focused on optimising production to maximise cash flow while aggressively exploring its large tenement package in pursuit of organic growth opportunities. In the past few months, the company has made several material decisions to transition itself into a de-risked, sustainable, high margin gold producer. These decisions include the appointment of new CEO, implementation of the revised operating plan, and recapitalising itself via equity capital raising. Over the past few years, the company has significantly improved its bottom-line from a net loss of $8.05 million in FY15 to a net profit of $3.02 million in FY19.

Financial Overview (Source: Company Reports)

The company is now moving towards a more measured and staged approach at Westralia, whilst accelerating ore production from the open pits which will allow the company to further optimise the strategy to unlock maximum value for the company and shareholders. The company’s next three-year outlook will be underpinned by open pit ore sources, with the continuation of production from Jupiter and mining of the Mt Marven open pit. Moving forward, the company's exploration expenditure will be focussed on low risk, well-understood opportunities to supplement and extend a three-year outlook.

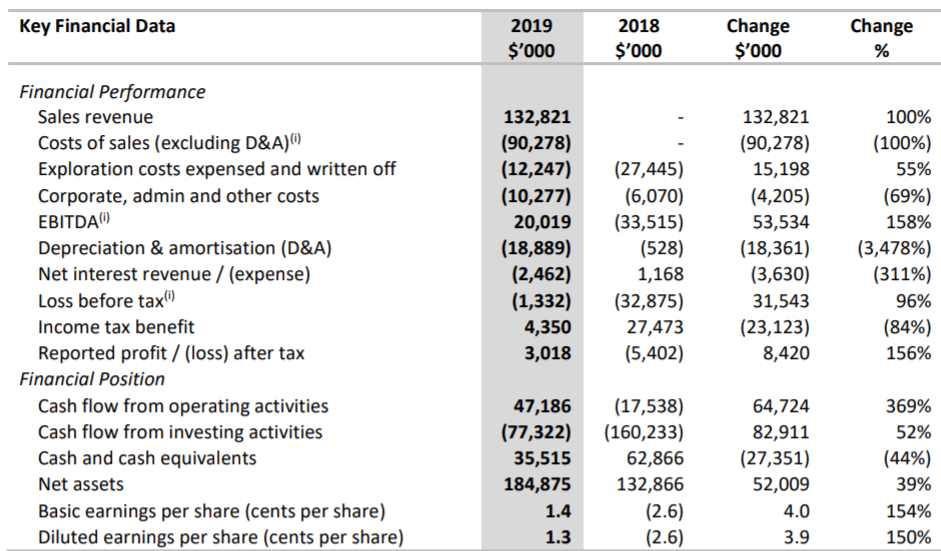

FY19 Performance Highlights: The company has been listed on ASX for seven years now and the financial year 2019 was its first full year as a gold producer as it produced 138,911 ounces of gold during the year, the highest level of annual production yet recorded from the Mt Morgans gold field which first produced gold in the late 1890s. During the year, the Westralia underground produced over 830,000 tonnes of ore for 85,000 ounces of gold mined and the Jupiter open pit mined 2 million tonnes of ore for 65,000 ounces of gold mined.

For FY19, the company reported gold sales revenue of $132.6 million, generated from the sale of 75,000 ounces at an average gold price of A$1,767. During the year MMGO Ore Reserves increased by 16% to 1.4Moz and Measured and Indicated Resources increased by 11% to 2.5Moz. For FY19, the company reported a net profit after tax of $3.02 million, as compared to the net loss of $5.4 million recorded in FY18.

FY19- Key Financial Data (Source: Company Reports)

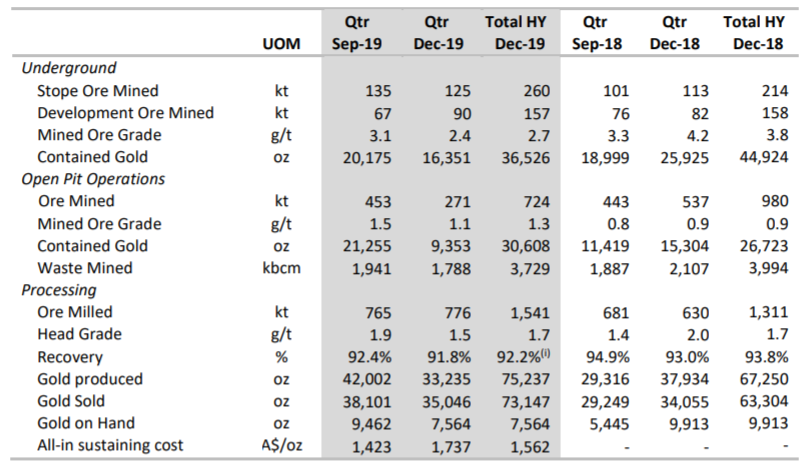

H1FY20 Performance Highlights: In the first half of FY20, the company reported production of 75,237 ounces of gold at an AISC of $1,562 per ounce. The company reported gold sales revenue of $141.8 million, generated from the sale of 73,147 ounces at an average gold price of A$1,938. The underground mine production at Westralia totalled 417kt at 2.7 g/t for 36,526 ounces of contained gold and the mine production at the Jupiter open pit for the half-year totalled 724kt at 1.3 g/t for 30,608 ounces of contained gold.

For the half-year period, the company reported a net loss after tax of $78.5 million, impacted by $68.5 million of MMGO asset impairments and a net tax expense of $18.1 million. At the end of half-year, the company had cash on hand of $28.1 million.

Production Summary (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 39.49%. Franklin Advisers, Inc. and Invesco Advisers, Inc. hold the maximum interest in the company at 7.66% and 5.07%, respectively.

Top 10 Shareholders (Source: Refinitiv, Thomson Reuters)

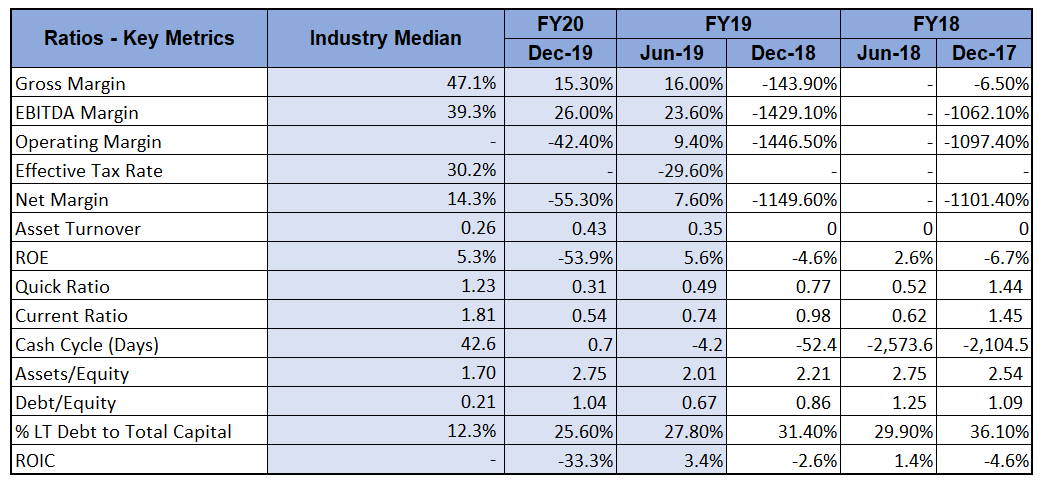

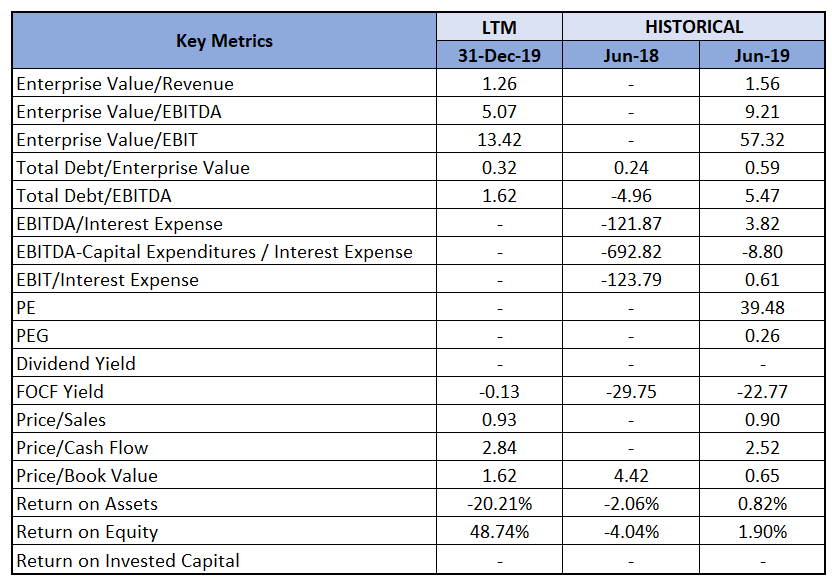

A Quick look at Key Margins: Over the last one year, the company has significantly improved its profitability margins. The company’s asset turnover ratio currently stands at 0.43x, higher than the industry median of 0.26x. the company’s debt to equity ratio is currently at 1.04x, lower than the industry median of 0.21x.

Key Metrics (Source: Refinitiv, Thomson Reuters)

Covid-19 Update: The company has been proactive in responding to Covid-19 pandemic. It has implemented several proactive measures to prevent its staff, people and operations from the pandemic. To reduce exposure, the company has directed the non-essential site-based personnel to work remotely. Till now, the Mt Morgans Gold Operation is continuing to operate unimpacted by the pandemic. In a situation where DCN is required to scale back its operations, the company has multiple levers it can engage including the processing of stockpile material totalling 4.4Mt @ 0.6 g/t for 79,000oz.

Three Year Outlook (FY2021-2023): DCN has already set its three-year outlook, as per which it expects its average annual gold production from FY2021-2023 to be around 110,000oz at AISC of $1,350/oz. The outlook prioritises high-margin, open-pit production while significantly reducing Dacian’s operating risk. Further, it is underpinned by open pit ore sources (96%), with continuation of production from Jupiter and mining of the Mt Marven open pit. In the financial year 2021, the company expects its production to be in the range of 120,000-130,000oz at an AISC $1,250-$1,350/oz.

Three Year Operating Profile (Source: Company Reports)

March 2020 Quarter Update: During the March 2020 quarter, the company produced 31,695 ounces of gold, in line with the guidance, positioning the company favourably to meet its full-year production guidance of between 138,000-144,000 ounces. Over the period, the Jupiter open pit mined 475,380t @ 1.0 g/t gold for 14,849 contained ounce. The Westralia underground mined 200,775t @ 2.9 g/t gold for 18,409 contained ounces during the March quarter.

At the end of the March quarter, the company had total cash and unsold gold of $14.1 million and total debt of $94.7 million. As at 31 March 2020, the total forward hedge position was at 115,455 ounces at an average of A$1,978/oz.

Recapitalisation via Equity Raising: In order to deliver on its three-year outlook, the company recently recapitalized itself via equity raising. On 8th April 2020, the company announced that it is conducting the Offer to raise up to approximately $98 million, comprising an institutional placement of up to 99.4 million new fully paid ordinary shares in Dacian and a 1 for 1 accelerated pro rata non-renounceable entitlement offer of up to 228.4 million New Shares. Till now, the company has completed the bookbuild of the Placement and the Institutional Entitlement Offer to raise approximately $70 million. In addition, it has also completed the retail component of its 1 for 1 fully underwritten accelerated non-renounceable pro-rata entitlement offer, taking Dacian’s total equity raised to approximately $98 million (before transaction costs).

This equity raising resets capital structure, providing the flexibility to pursue high-margin production, particularly following the run-off of hedges. This equity raising also provides the opportunity to invest at a substantial discount to fundamental value and immediate peers.

What to expect: With the company now recapitalised, it can focus now its full attention on delivering its three-year production outlook, with potential upside beyond that to come from its targeted near-mine exploration program, regional consolidation opportunities and the Westralia underground.

For the June 2020 quarter, the company expects the AISC for MMGO to trend lower relative to the March quarter as mining activities are focused mainly in ore within the Heffernans open pit, as well as further reductions in underground expenditure that began late in the March quarter. For FY20, the company expects its production to be between 138,000-144,000oz at MMGO AISC of $1,550-$1,650/oz. Moving forward, the company intends to test a number of advanced exploration targets during FY2021 including Phoenix Ridge, Cameron Well, Mt McKenzie, McKenzie Well, Southern BIF, and other exploration targets.

On 16 June 2020, the company is going to hold its Extraordinary General Meeting.

Key Valuation Metrics (Source: Refinitiv, Thomson Reuters)

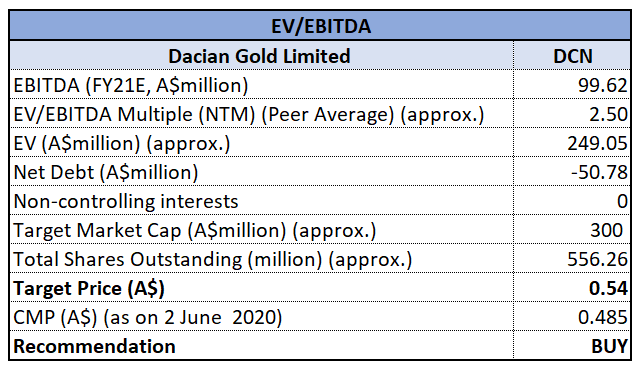

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative)

EV/EBITDA Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Following the recent equity raising, the company’s balance sheet is now strengthened to underpin its three-year business plan. In the past six months, the stock of DCN has corrected by 46.26% on ASX and is inclined towards its 52-week low of $0.228, offering investors a decent opportunity for accumulation. We have valued the stock using an EV to EBITDA multiple based illustrative relative valuation method and have arrived at a target price with lower double-digit upside (in % terms). Considering the company’s recent capital raising, its decent March quarter performance, its three-year outlook, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $0.485, up by 5.435% on 2 June 2020.

.png)

DCN Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...