Company Overview - Genworth Mortgage Insurance Australia Limited (Genworth Australia) is an Australia-based company, which provides Lenders Mortgage Insurance (LMI). Genworth Australia has commercial relationships with over 100 lenders across Australia, including three banks. The Company's products include Standard LMI, which is for a range of borrowers, including first home buyers and investors wishing to access residential mortgage finance; Business Select, which is for self-employed borrowers; HomeBuyer Plus, which is for a range of borrowers, including first homebuyers, and Family Pledge, which is for borrowers, such as first homebuyers with no deposit.

.png)

GMA Dividend Details

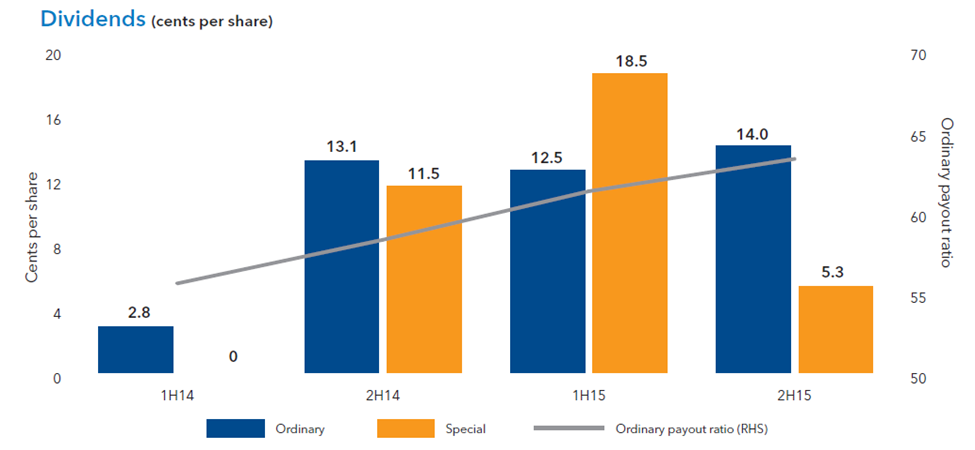

Boosting capital position: Genworth Mortgage Insurance Australia (ASX: GMA) is seeking to boost its capital position for the future growth. Accordingly, the group issued over $200 million of Tier 2 subordinated notes. GMA delivered a fully franked special dividends of over 23.8 cents per share as well as declared a total dividends of 50.3 cents per share during the year. The group reported over $150 million worth of market share buy-back as well as restructured the reinsurance program by enhancing the reinsurance to $950 million as of January 01, 2016. The group intends to pursue more capital management initiatives during 2016 to achieve the group’s target range of 1.32 to 1.44 times Prescribed Capital Amount (PCA). As per its balance sheet highlights for 2015, GMA has a regulatory capital base of $2.6 billion while the coverage ratio was 1.59 times the Prescribed Capital Amount (PCA) on a Group (Level 2) basis, which is more than the group’s estimated range of 1.32 – 1.44 times the PCA. Cash and investment portfolio reported a market value of $3.9 billion as of December 2015 having 96% of the investment portfolio in Australian dollar denominated cash, cash equivalents and fixed income securities. Moreover, 96% of the group’s portfolio was also rated A- by major rating agencies.

Standard & Poor’s Ratings Services (S&P) reiterated their credit rating of ‘A+’ and gave a ‘Stable’ outlook to the group. Meanwhile, Moody’s reaffirmed the rating of Genworth Financial Mortgage Insurance as well as Genworth Financial Mortgage Indemnity with A3 and a Negative outlook. But, Fitch Ratings reassured the group’s rating of ‘A+’ and gave a ‘Stable’ outlook.

Delivered revenue growth but weak bottom line performance: Genworth Mortgage Insurance Australia reported a soft fiscal year of 2015 performance with the underlying Net Profit after Tax (without mark-to-market movements in the investment portfolio) falling by 5.3% to $264.7 million against the same period of last year. The group’s High loan-to-value ratio (LVR) lending as a proportion of total mortgage originations decreased on the back tight lender risk appetite due to regulatory changes. Consequently, the group’s New Insurance Written (NIW) fell by 9.9% to $32.6 billion while Gross Written Premium (GWP) declined by 20.0% to $507.6 million against the prior corresponding period. On the other hand, overall revenue, as measured by Net Earned Premium (NEP), increased by 5.4% yoy to $469.9 million as the increase was contributed from the revenue recognition pattern for the group from before book years. But, Loss ratio for 2015 increased to 24% as compared to 19% in the same period of last year, due to rising borrower sales as well as decrease in number of loan arrears converting to claim in 2014. Meanwhile, the Victoria and New South Wales regions delivered a strong performance due to a steady unemployment and house price appreciation. However, the Queensland and Western Australia markets have been under pressure given the rising unemployment and house prices pressure but started recovering in the second half of 2015.

The group’s financial income decreased during the year on the back of mark-to-market losses of $52.4 million given the falling interest income from lower investment yields. Still, the group was able to marginally decrease the expense ratio to 26.2% in fiscal year of 2015 as compared to the 26.5% in FY14. Conversely, the Insurance margin declined to 58.1% during the period against the 65.8% in FY14, due to rising net claims incurred and unfavorable investment income leading from mark-to-market losses. Nevertheless, the greater financing cost was boosted by a $2.4 million one-time premium fee paid on the early redemption of the subordinated note in July 2015.

.png)

Gross written premium and Residential mortgage market (Source: Company Reports)

Built a solid customer base: Genworth Mortgage Insurance Australia built long term commercial relations with over 100 lender customers across Australia as well as entered into Supply and Service Contracts with 10 of its major customers. The group’s top three customers contributed over 72% of its overall NIW as well as 65% of GWP for fiscal year of 2015. Genworth Australia forecasts over 39% of the Australian LMI market by NIW in 2015. GMA even renewed their contract with National Australia Bank for provision of LMI for NAB Broker business in FY15. On the other hand, the group stopped writing new business with Westpac after the termination of the contract during May 2015 even though they are offering their services to Westpac’s existing business. But, GMA intends to continue to focus on building its customer relationships as well as optimize its capital structure.

Management intends to continue working on LMI recognition as well as seeking to launch more of innovating products and services to position before any future threat of disruption in the market. For the fiscal year of 2015, GMA offered the three LMI products in 2015 which are Standard LMI, Homebuyer Plus and Business Select/Low Doc. Consequently, the Standard LMI produced a major share of 99% of overall gross written premium while the other two products generated the remaining GWP. GMA underwrites LMI through flow and portfolio channels. Over 98% of the business was generated from the flow channel during fiscal year of 2015 while the remainder was from the portfolio channel.

Dividends (Source: Company Reports)

Outlook: Management gave a positive outlook for Australian residential mortgage market driven by factors like fall in unemployment, lower interest rates and an ongoing focus by regulators on lending standards. GMA believes that house price appreciation will moderate in 2016.

The group however reported that the high LVR market would be under pressure even for 2016 while estimates its GWP to fall by over 20% on the back of tough market conditions. Genworth Australia even forecasts its 2016 NEP to fall by over 5% and for the full year the loss ratio is estimated to be in the range of 25% to 35%. Management expects an ordinary dividend payout ratio range of 50% to 80%. The overall 2016 outlook has been said to be subject to market conditions. On the other hand, the group continues to decrease the risk for its lender customers and support its creditworthy borrowers to buy a property having a less deposit.

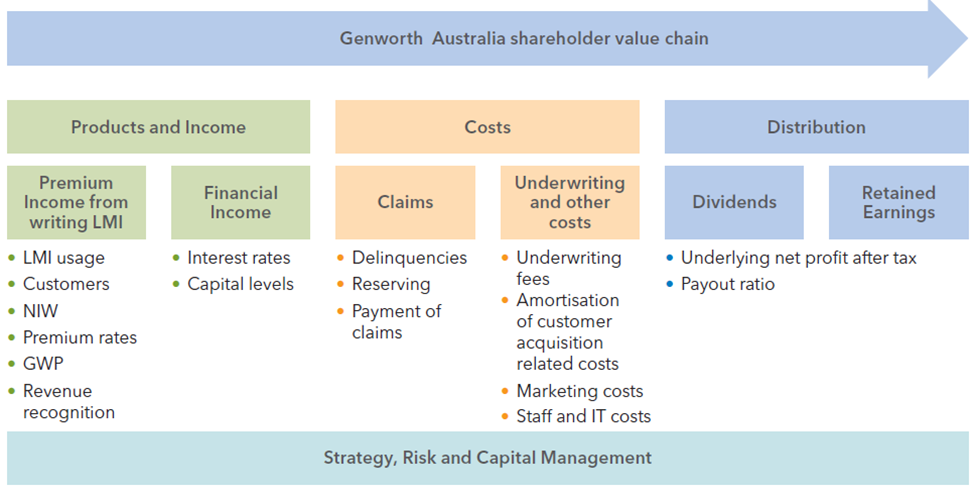

GMA business model (Source: Company Reports)

Outstanding dividend yield: Genworth Australia offers insurance for over $320 billion worth of home loans in the Australian and New Zealand mortgage markets. On the other hand, the group’s stock fell over 22.7% in the last one year and declined by 8.3% during this year to date (as of April 15, 2016) given the ongoing challenging environment across Australia. But, recently the group undertook a capital management initiative for the distribution of 34 cents per share to shareholders, leading to an overall payment of over $202 million. This move is to return a certain surplus capital to its shareholders, confirming that the group continues to uphold an efficient capital structure. Accordingly, GMA announced a security consolidation wherein every 10,000 (pre-consolidation) securities would be consolidated into 8,555. The share consolidation would decrease the number of the group’s shares on issue from 595.4 million to over 509.4 million (accounting over 14.5% decrease in the number of shares on issue).

Hence, the stock recovered by over 3.4% in the last four weeks alone (as of April 15, 2016). Moreover, the heavy correction in the stock also placed the group at attractive valuation from a long-term perspective with GMA trading at a very low P/E as compared to its peers as well as an outstanding dividend yield. Based on the foregoing, we reiterate a “BUY” recommendation on the stock at the current price of $2.42, ahead of its first quarter of 2016 results, scheduled on April 29, 2016.

.PNG)

GMA Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...