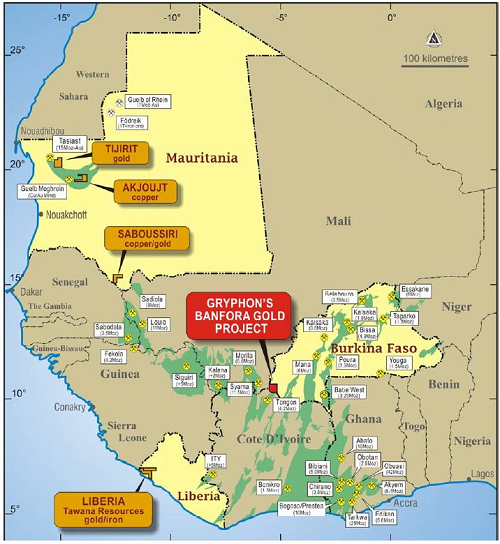

Company Overview - Gryphon Minerals (ASX:GRY) is developing the 4.9Moz Resource Banfora Gold Project, Burkina Faso as well as its pipeline of new and exciting projects in West Africa. The Banfora Project area covers 1,200km2 and mineralisation drilled so far is shallow with 90% less than 150 meters from surface and with scope to extend this considerably deeper with further drilling. The Banfora Project is in a major gold producing district, host to such world class gold deposits as Randgold’s Tongon (4.2Moz), Resolute’s Syama (5 Million oz Au mined & 6.5 Million oz Au in resources) and Randgold/Anglo Ashanti’s Morila (6.5Moz).

Analysis – In light of the current gold price, GRY has completed a number of optimisation studies to tailor the Banfora project to a lower gold price environment. The study concludes a 2Mtpa heap leach offers the best performance at gold prices between US$900 – US$1400/oz. Assuming a US$1200/oz base case the study envisages production of 71kozpa over a 9 year mine life for an initial cost of US$95m. Gryphon has A$48m in cash on hand at the end of December 2013 and in our view the company is sufficiently funded through to a development decision where it will likely need to raise additional equity. We assume 60% debt funding and forecast A$25m in additional equity.

In the context of the falling gold price last year, we believe many producers may be forced to reassess internal growth projects against those owned by developers which have recently finished studies. We have seen M&A activity in West Africa pick up recently with two ASX listed gold developers, PMI Gold and Ampella being acquired by Asanko and Centamin respectively. We believe that Gryphon may also be a logical target given its promising exploration upside. Our upside scenario is based on an expansion at Banfora with higher throughput and production levels as well as a higher gold price environment.

GRY Daily Chart (Source - Thomson Reuters)

GRY Daily Chart (Source - Thomson Reuters)

Gryphon has released a scoping study for a heap leach operation at its Banfora gold project in Burkina Faso. We estimate a post-tax unlevered Internal Rate of Return (IRR) of 39% for the 2mtpa heap leach project at US$1,300/oz gold. While studies are at an early stage we believe this represents a credible development option. In our view the US$95m capex estimate for the heap leach operation is more digestible in the context of the company’s A$64m market cap. Considering the project’s preliminary economics and the company’s A$48m cash balance at the end of DEC-13, we believe the project has a realistic chance of obtaining the necessary funding.

The study also considered expansion options in a higher price gold enviorment. At $1400/oz, the operation could be expanded to 4Mtpa for an additional capital cost of$34m. An expanded operation would process lower grade material at 1.2g/t producing 108kozpa over a similar mine life. Furthermore in gold price scenarios of over US$1400/oz, the addition of a Carbon-in leach (CIL) circuit to process primary material has the potential to add further value. As part of the optimisation study GRY has revised the Banfora resource estimate. The revisison was completed to take into account a lower gold price, an improved estimation technique (Multiple Indicator Kriging and ordinary Kriging), incorporation of mining dilution in the resource model rather than the mine design and reduced wireframe depths to account for lower gold price along with low heap leach recoveries in the primary material.

Banfora Gold Project, Burkina Faso (Source – Company Reports)

Banfora Gold Project, Burkina Faso (Source – Company Reports)

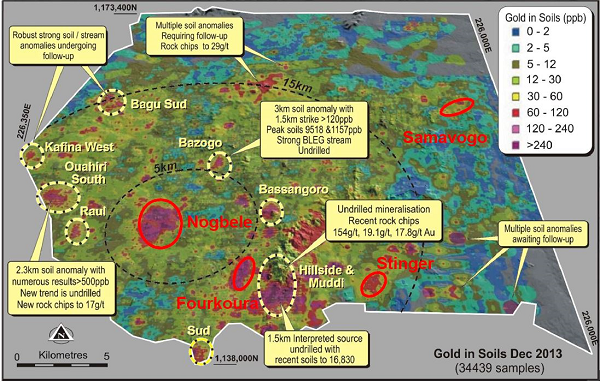

We believe the Banfora project still offers significant exploration potential. Soil sampling has identified a large number of targets. Recent rock chip sampling has highlighted the prospectivity of some of these targets with the gold values of up to 154 Grams per tonne (g/t) which have to be drill tested. In our view it is likely that oxide material with a grade of 1.5g/t and within a 15km radius of the propsed plant at Nogbele would be economic. We maintain the view that there is a good chance that the Banfora project could be a large scale project than that envisaged by the scoping study.

Banfora – Gold in soils (Source – Company Reports)

Banfora – Gold in soils (Source – Company Reports)

The heap leach option has considerably lower and manageable capital requirements, low operating costs, resilience in a low gold price environment and easily expandable. With a 2Mtpa Heap Leach operation at Banfora we see much improved economics albeit with some technical risk associated with Heap Leach recoveries. With the mining permit expected to be granted in the coming months and a potential funding arrangement in place by the end og Q1 2014 we see GRY continuing to outperform. We are putting a BUY recommendation on the stock at today’s closing price of $0.185.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Please wait processing your request...

Please wait processing your request...