Kalkine has a fully transformed New Avatar.

Company Overview: Hansen Technologies Limited is a global customer care and billing solutions provider that develops, implements and supports software, and delivers data center, application and implementation services for the energy, pay television and telecommunications industries. The Company's segments include Billing, which represents the sale of billing applications and the provision of consulting services in regard to billing systems; IT outsourcing, which represents the provision of various information technology (IT) outsourced services covering facilities management, systems and operations support, network services and business continuity support, and Other, which represents software and service provision in superannuation administration. Its geographical segments include APAC, which includes sales and services across Australia and Asia; Americas, which includes sales and services across the Americas, and EMEA, which includes sales and services across Europe, the Middle East and Africa.

.png)

HSN Details

Strong Revenue Model with Strategic Acquisitions: Hansen Technologies Limited (ASX: HSN) is a small-cap information technology systems and services provider with the market capitalization of ~$718.1 Mn as of May 10, 2019. The company provides its services to the energy or utilities, telecommunications, and pay-TV industries. The diversification of business comes in the form of delivering proprietary solutions across a range of geographies and industry sectors, ensuring stability in business revenues. The diversification is supported along with the services of the company being used by the clients for an extended period of time, and this ensures that it will continue to enjoy a strong recurring revenue stream. It focuses on growing its foothold in new and existing markets by delivering into these markets either directly or through a partnership with a local industry partner.

The company has a strong track record of effective acquisitions, including the largest acquisition of Enoro. In FY18, the company has strategically decided to go to market with its new unifying brand, HansenCX. In existing and new markets across the globe, HansenCX will be a common brand that exhibits the success of Hansen worldwide. The approach of the company to the global market continues to be driven by a strong focus on servicing its clients’ needs, targeting strategic opportunities for new business and acquiring businesses that complement and strengthens the core business of the company. We presume that the synergistic acquisition will support the overall growth to the business in the upcoming period. The company enjoys +500 client base spread across Energy, Pay TV, Telecommunication and Water industry throughout the world. These include EnergyAustralia, Direct Energy, MNC Group, Telia, UrbanUtilities, etc.

.png)

Hansen Client Base (Source: Company Reports)

Acquiring Sigma Systems: Sigma Systems is into providing catalog-driven software products primarily to the companies in the telecommunication, media and high-tech sector globally. The Toronto based company with a huge customer base, has software products which streamline complex products & services with fastening the process of creating, selling & delivering new digital and traditional products & services.

Hansen is acquiring Sigma for an Enterprise Value of CAD$157.0 million or AUD166.2 million. It represents an EV/EBITDA multiple of 8.3x. The funding, however, will be done through a new bank debt facility of AUD 225.0 million. The acquisition deal is likely to close on 31st May 2019.

SIGMA’s Customers (Source: Company Reports)

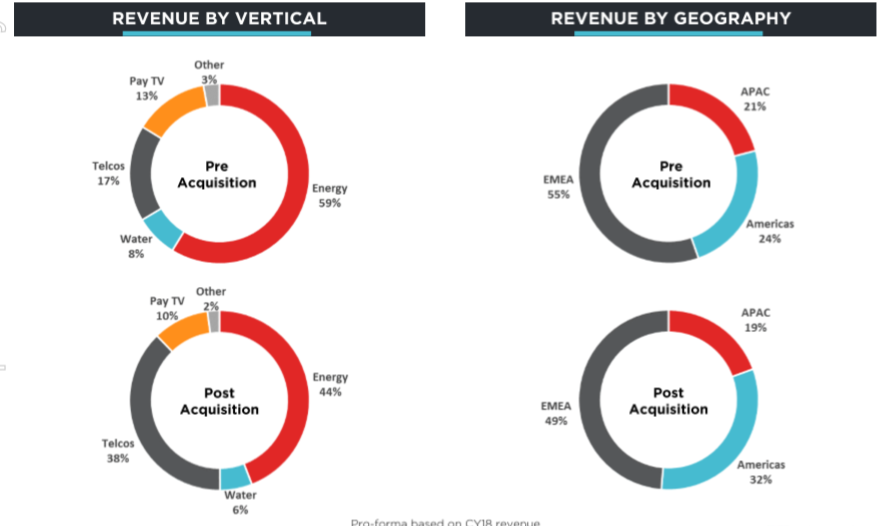

Strategic Rationale: The company’s business is a high-quality asset with its global footprints. HSN is a leader in providing catalog-driven software products. The products are in line with the core business of billing & customer management and are well designed to capture any growth opportunities from the roll-out of 5G telecommunication service. It gives Hansen significant opportunities to expand its scope and scale in the telecommunication sector. On a pro-forma basis, Hansen would have had revenue from the telecommunication sector of 38.0% of the total revenue in CY18, if Sigma was owned during that period as compared to the actual revenue of 17.0%. Moreover, the cross-selling opportunities for the company exist into the large utility customer base of Hansen, with the integration of the catalog product into the energy product offerings of Hansen as well as Pay TV.

The CY18 revenue of Sigma was CAD73.1 million or AUD75.5 million, and the normalized EBITDA in CY18 was CAD18.8 million or AUD19.4 million, equating to a normalized EBITDA margin of 25.7%. The earnings per share are expected to be accretive in FY20, excluding non-IFRS measure like amortization of acquired intangible assets.

Hansen Pre & Post Acquisition (Source: Company Reports)

Key Financial Highlights: The operating revenue for Hansen in 1H19 was $112.4 million, down by 5.1% on 1H18 and consistent with 2H18. The company exhibited broadly consistent recurring revenues over the past year, however the reduction in the overall operating revenue in comparison to 1H18 was due to lower non-recurring revenues, underpinned by lower project work which followed the large part of work completed in the first half of FY18 associated with implementing Power of Choice for the customers in Australia and lower one-off licence fees.

The EBITDA for Hansen in the first half of FY19 stood at $28.5 million, $5.3 million lower than 1H18 and $3.0 million higher than 2H18. The EBITDA margin in 1H19 was 25.3% lower when compared to 28.6% in 1H18, however, it improved on the 22.7% in the second half 2H18. The 1H18 EBITDA margin was primarily underpinned by the elevated amount of non-recurring revenue. An improved margin was achieved in 1H19 with revenue remaining consistent from 2H18 to 1H19 due to lower employee expenses as well as lower “other” expenses driven by reduced contractor, occupancy and travel costs.

After the implementation of the new accounting standard AASB 15 (which has the effect of reducing reported recurring revenue) and reclassification of some of Enoro’s revenues, the recurring revenue for Hansen stood at 63% of total revenue in 1H19.

On the cash flow front, the company reported free cash flow for 1H19 of $10.1 million, with a net $8.0 million increase in working capital. The increase in working capital was driven by a $2.6 million negative impact on working capital from the adoption of AASB 15 that is expected to smoothen over time, and a seasonal increase in Enoro’s working capital.

In January 2019, the group exhibited a $3.2 million improvement in the working capital position. The company repaid debts of $4.7 million during the half which left a gross outstanding debt of $22.7 million at the period end, and a net debt position of $0.6 million, resulting in a strong balance sheet position to fund for future growth.

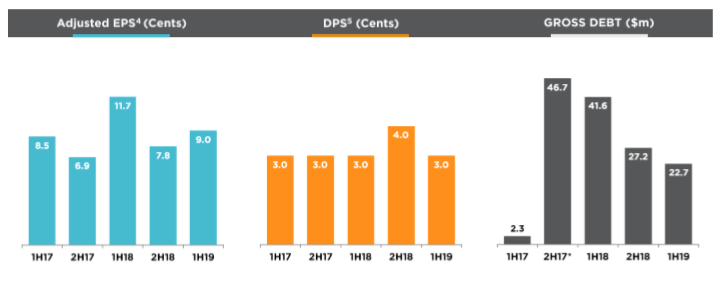

Key Ratios & Margins: Among the key profitability ratios, ROE and pre-tax ROA stood at 5.5% and 5.1%, an increase of 60 bps and 100 bps respectively on the previous half, which is substantially higher than the industry median. Among the balance sheet ratios, the fixed asset turnover and current ratio stood at 11.12x and 1.47x, exhibiting a significant increase compared to the previous half, however, the current ratio came in marginally below the industry median of 1.66x.

1HFY19 Key Metrics (Source: Company Reports)

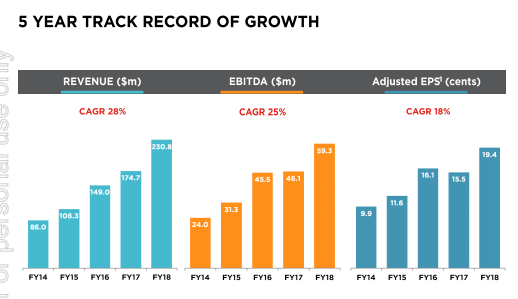

The key metrics of the company consistently maintained its growth over the past five years. It experienced a CAGR growth of 28.0% in revenue with the absolute revenue numbers standing at $230.8 million in FY18 as compared to $86.0 million in FY14. The EBITDA experienced a CAGR growth of 25.0% with $59.3 million in FY18 as compared to $24.0 million in FY14. The adjusted earnings per share (EPS) significantly increased to 19.4 cents per share in FY18 with a CAGR growth of 18.0% over the past five years.

5 Year Track Record (Source: Company Reports)

Top ten shareholders form around 42.03%of the total shareholding as highlighted in the below table. Hansen (Andrew Alexander) holds maximum interest in the company with a stake of 17.61% followed by Mawer Investment Management Ltd. and Fidelity Management & Research Company with 8.59% and 4.41% stakes respectively.

Top Ten Shareholders (Source: Thompson Reuters)

FY19 Outlook: The company expects the FY19 guidance to remain almost same as provided previously during August 2018. However, with 1H19 revenue being higher than anticipated, the company expects 2H19 revenue to be in line with 1H19, whereas the previous guidance was for a stronger 2H19 revenue as compared to 1H19.

As per the full year guidance, Hansen expects operating revenue to be slightly lower than FY18, predominantly due to a lower level of non-recurring licence fees and services revenue following the elevated levels achieved in 1H18. It was due to termination of an underperforming call centre contract in June 2018 within the US Solutions business, on the back of which the company will have a loss of ~$1.9 million of revenue in FY19 compared to FY18.

The company expects the expense for FY19 to remain in line with FY18. A higher expense base is expected in the second half of FY19 as compared to 1H19 on the back of continuous investment in the global platform to support future growth.

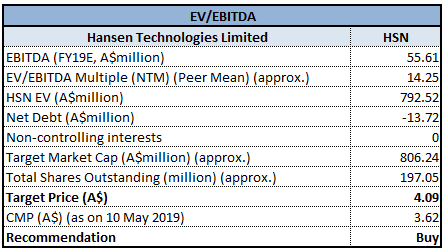

Valuation Methodology: EV/EBITDA Multiple Approach (NTM):

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: Meanwhile, HSN’s stock has risen 19.32% in the past one month as on 9 May 2019 and is trading at a P/E multiple of 29.84x. The company has immediate support at ~$2.89 and resistance at ~$3.80 level. With the current scenario of the strategic acquisition of Sigma Systems and its benefits to be reaped going forward through the substantial synergies, the company is well poised for revenue growth in the niche areas. Moreover, the core financials of the company look decent on the back of strong fundamentals, with consistent growth over the past few years. Further, supported by strong parameters as aforesaid facts, we recommend a “Buy” rating on the stock at the current market price of $3.620 per share (down 0.549% on 10 May 2019).

HSN Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...