Kalkine has a fully transformed New Avatar.

Company Overview: Hansen Technologies Limited is a global customer care and billing solutions provider that develops, implements and supports software, and delivers data center, application and implementation services for the energy, pay television and telecommunications industries. The Company's segments include Billing, which represents the sale of billing applications and the provision of consulting services in regard to billing systems; IT outsourcing, which represents the provision of various information technology (IT) outsourced services covering facilities management, systems and operations support, network services and business continuity support, and Other, which represents software and service provision in superannuation administration. Its geographical segments include APAC, which includes sales and services across Australia and Asia; Americas, which includes sales and services across the Americas, and EMEA, which includes sales and services across Europe, the Middle East and Africa.

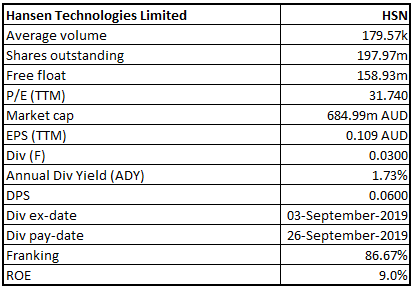

HSN Details

Financial Performance in FY19 in-line with the Guidance: Hansen Technologies Limited (ASX: HSN) is primarily engaged in the development, integration and support of billing systems software for the utilities, energy, pay-TV and telecommunication sectors. Through its offices in Europe, North and South America, South Africa and the Asia Pacific region, the company provides its services in over 90 countries around the world. In FY19, revenue remained almost flat in comparison to FY18. Underlying EBITDA and underlying NPAT dropped at a rate of ~7.0% and ~18.7%, respectively. The decline was majorly a result of low non-recurring revenues, due to lower one-off license fees and reduced project work in comparison to FY18. During the year, the company reported significant achievement with respect to business operations, ranging from new contracts to expansion and development. Some of the achievements during the period included a major contract to deliver the company’s second billing system in Finland. The company secured another contract to deliver its next-generation Meter Data Management (MDM) solution in Sweden. Other developments included the expansion of Vietnam Development Centre, client upgrades, development of a new analytics SaaS product, etc.

In 2020, the company is looking forward to the integration of Sigma, acquired late in FY19, into its platform. Simultaneously, it will continue to assess more acquisition opportunities to enhance shareholders’ value. In addition, it will leverage the network of low-cost development centres to improve both customer delivery and margins.

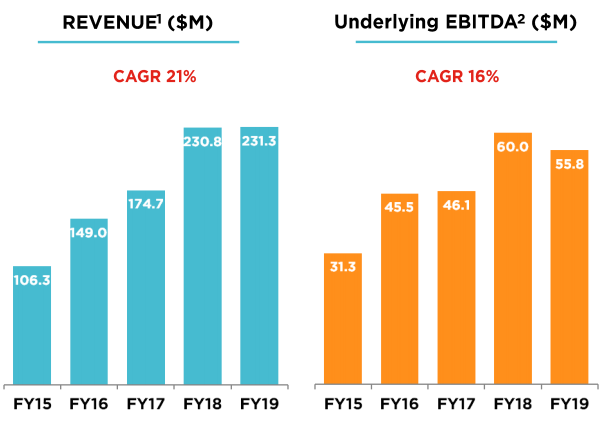

Over the 5-year period covering FY15 to FY19, the company’s revenue witnessed a CAGR growth of 21%, with FY15 and FY19 revenue amounting to $106.3 million and $231.3 million, respectively. Over the period, revenue has seen a continuous upward movement. However, in FY19, the value remained almost flat in comparison to FY18 due to lower non-recurring revenues. Bottom-line of the company grew at a CAGR of 6.1% over the same period, with FY15 and FY19 profit after tax amounting to $16.94 million and $21.46 million, respectively. Among all the five years, revenue and profit grew the highest in FY16, with an increase of 39.8% and 54.0%, respectively. Underlying EBITDA over the 5-year period witnessed a CAGR growth of 16%, with FY15 and FY19 EBITDA amounting to $31.3 million and $55.8 million, respectively.

5-Year Revenue and Underlying EBITDA (Source: Company Reports)

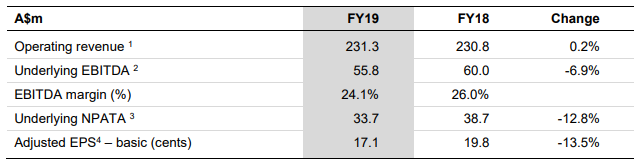

FY19 Financial Highlights: During the year ended 30 June 2019, the company reported operating revenue amounting to $231.3 million, up 0.2% on FY18 revenue of $230.8 million. Underlying EBITDA for the year amounted to $55.8 million, down 6.9% on prior corresponding period EBITDA of $60.0 million. Underlying NPATA stood at $33.7 million, down 12.8% on NPATA of $38.7 million in FY18. The company highlighted that the result was in-line with the guidance provided, despite a backdrop of challenging operating conditions for customers. Net debt of the company stood at $148.3 million, being the highest since inception. The board declared a fully franked final dividend of 3.0 cents per share, with record date and payment date of 4 September 2019 and 26 September 2019, respectively.

FY19 Results Summary (Source: Company Reports)

Operational Highlights: Although the financial performance in FY19 was impacted due to lower license fees and reduced project work, the company reported a significant development on the operational front. During the year, the company expanded the Vietnam Development Centre, increasing the employee count from 9 in FY18 to 100 in FY19. The centre supports the company’s products in the Nordic, Americas and the Asia-Pacific regions. The company also developed a new analytics software-as-a-service product for the Utilities sector in the Nordic region. Soon after the launch, the product gained momentum and now has 20 users. During the year, the company commenced 8 client upgrades to the new version of its US municipalities’ billing system. Also, HSN signed some major contracts in Sweden, Finland and Australia.

Update on Acquisitions: The company had acquired Enoro in July 2017, which has now been completely integrated into its platform and continued to perform strongly in FY19. Another significant acquisition included that of Toronto-based Sigma Systems, on 1 June 2019. The acquisition was the largest to date, involving a total consideration of $163.8 million. Sigma Systems is engaged in the provision of catalogue-driven software products for technology, telecommunication and media companies. The company has an employee strength of 500 and serves more than 70 customers. Sigma’s acquisition was funded from a new loan facility amounting to $225 million, of which $35 million remained unused at the end of the period.

Post-acquisition of Sigma, the company has balanced out its operations among the two business verticals, namely Utilities and Communications. The acquisition will significantly increase the scale and expertise in the communications sector and will help to address a bigger part of the customer needs through product innovation, customer quoting and ordering, customer care, etc. In addition, the acquisition also brings in cross-sell opportunities with Hansen’s large customer base in the Utility segment.

With the addition of Enoro and Sigma, the company has significantly expanded its footprint across dynamic market segments and has expanded its global operations to a great extent. As discussed in the above section, Enoro has continued to make a positive contribution since integration. Alongside, the company is expecting Sigma’s acquisition and integration to add further value to the business. The company is expected to enhance customer experience with the potential to drive future revenue growth.

Notice of AGM: The company recently updated that the 2019 Annual General Meeting will be held on 21 November 2019.

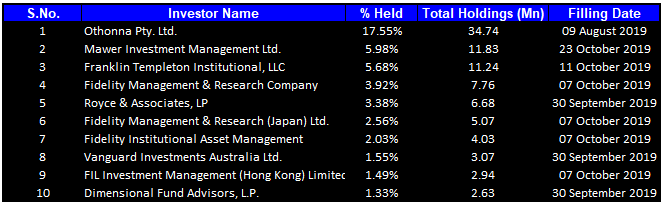

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 45.46% of the total shareholding. Othonna Pty. Ltd. is the entity, holding maximum shares in the company at 17.55%. Mawer Investment Management Ltd. is the second largest shareholder, with a holding of 5.98%.

Top Ten Shareholders (Source: Thomson Reuters)

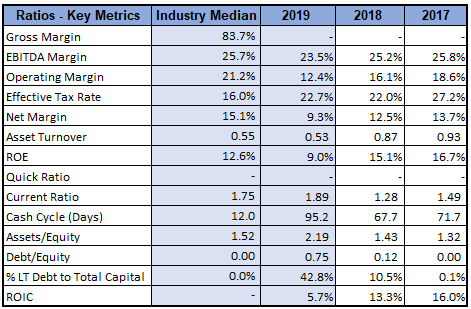

Key Metrics: During the year ended 30 June 2019, the company’s EBITDA margin and net margin stood at 23.5% and 9.3%, respectively. Current ratio for the year was reported at 1.89x, higher than the industry median of 1.75x and prior corresponding year’s current ratio of 1.28x. A higher current ratio in comparison to pcp and the industry median indicates that the company improved its short-term liquidity In FY19.

Key Metrics (Source: Thomson Reuters)

What to Expect: The company has entered the new financial year with decent momentum, with the recent acquisition of Sigma, that allows for new market entries and enhanced customer experience. The period was also characterised by signing of new major contracts that will unfold into returns in the future. It is also eyeing for new acquisition opportunities that can further add value to the business and hence, increase shareholders’ value. In FY20, the company expects operating revenue to be in the range of $305 million - $310 million. This represents growth in the range of 31.86% - 34.03% on FY19. EBITDA for the year is expected to be between $70 million - $76 million, representing growth in the range of 25.45% - 36.20%.

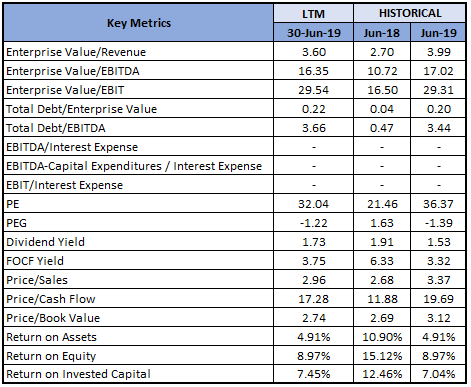

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

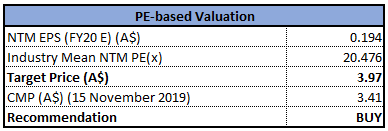

Method 1: Price to Earnings Multiple Approach:

Price/Earnings Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

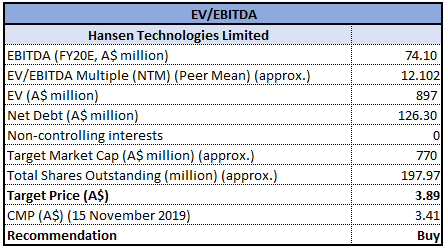

Method 2: Enterprise Value to EBITDA Multiple Approach:

EV/EBITDA Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The stock has generated negative returns of 1.98% and 10.36% over a period of one month and three months, respectively. Currently, the stock has a market capitalisation of $684.99 million and a price to earnings multiple of 31.74x. During the year ended 30 June 2019, the company managed to perform in-line with expectations, despite challenging operating conditions for customers. The highlight of the year was Sigma’s acquisition that has made a considerable contribution on the product and market front. Moreover, the acquisition and subsequent integration of Enoro have also proved to be a growth factor. While the acquisition of Enoro was weighed towards the Utility segment, Sigma’s revenues are concentrated in the Communication sector. This provided the company with a balance across its two main businesses and will ensure greater diversification across multiple industries, regions and clients.

Going forward, the company is expecting the above business to further drive revenue growth. Although net debt during the period was high, the company remains confident to dispose it over the coming years, given the cash generation capacity of the business. Free cash flow in FY19 amounted to $30.1 million, of which $20.0 million was related to the second half. Working capital improved by $4.8 million in the second half. Considering the operational achievement in FY19 in the form of new contracts and product development, expected synergistic benefits from Sigma and continued contribution from Enoro, and a decent financial guidance for FY20, we have valued the stock using two relative valuation methods, i.e., Price to Earnings and EV/EBITDA multiples, and arrived at a target price of lower double-digit growth (in % terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $3.410, down 1.445% on 15 November 2019.

HSN Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...