Kalkine has a fully transformed New Avatar.

Company Overview: Hansen Technologies Limited is a global customer care and billing solutions provider that develops, implements and supports software, and delivers data center, application and implementation services for the energy, pay television and telecommunications industries. The Company's segments include Billing, which represents the sale of billing applications and the provision of consulting services in regard to billing systems; IT outsourcing, which represents the provision of various information technology (IT) outsourced services covering facilities management, systems and operations support, network services and business continuity support, and Other, which represents software and service provision in superannuation administration. Its geographical segments include APAC, which includes sales and services across Australia and Asia; Americas, which includes sales and services across the Americas, and EMEA, which includes sales and services across Europe, the Middle East and Africa.

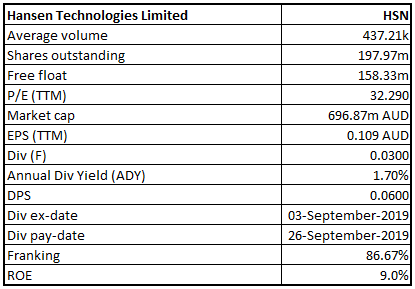

HSN Details

Acquisitions Delivering Good Results: Hansen Technologies Limited (ASX: HSN) provides software and services to the energy, water and communication industries. The company serves a network of over 550 customers in over 80 countries. Hansen’s business is formally structured around two verticals, including Utilities and Communications. In FY19, the company reported a marginal increase in revenue over pcp. The company has received remarkable returns from its acquisition of Enoro, which has now been fully integrated into the business. In June 2019, the company completed the acquisition of Sigma Systems, which is a global leader in catalogue-driven software products for telecommunications, media, and technology companies. From a financial perspective, the business continued to perform well with revenue and EBITDA coming in-line with guidance. Operating revenue, EBITDA and NPAT for the year ended 30 June 2019 came in at $231.3 million, $53.0 million and $21.5 million, respectively.

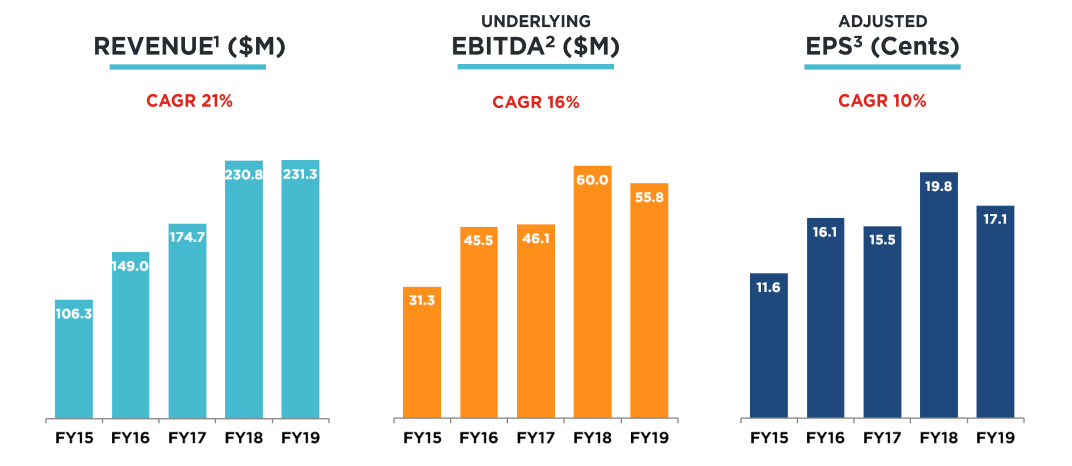

Through its unique position in the global market, the company has managed to deliver an impressive growth across key performance metrics. Over the period of FY15 – FY19, the business has reported revenue and EBITDA CAGR of 21% and 16%, respectively. Adjusted earnings per share over the above stated period delivered a CAGR of 10%. The company’s software offers a core capability to clients to create and sell new products and services, control critical revenue management and customer support processes. The company has a global presence against its competitors, that have a specific geographic presence, helping it maintain a good stand in the industry.

Through Sigma’s acquisition, the company is looking forward to expanding its product offering and quickly grabbing a share of the evolving market. Inclusion of Sigma Systems has rebalanced the company’s market portfolio, which was earlier weighted towards the Utilities sector. Overall, the acquisition has awarded the business with additional opportunities to win new clients and grow organic revenues.

5-Year Performance (Source: Company Reports)

FY19 Financial Highlights: During the year ended 30 June 2019, the company reported revenue amounting to $231.3 million, up 0.2% on prior corresponding period. Underlying EBITDA for the year came in at $55.8 million, down 6.9% on the previous year. As a result, underlying EBITDA margin declined from 26.0% in FY18 to 24.1% in FY19. Underlying NPATA for the year stood at $33.7 million, down 12.8% on the prior corresponding year. Adjusted earnings per share came in at 17.1 cents, representing a decline of 13.5% on FY18 EPS of 19.8 cents.

.png)

FY19 Results Summary (Source: Company Reports)

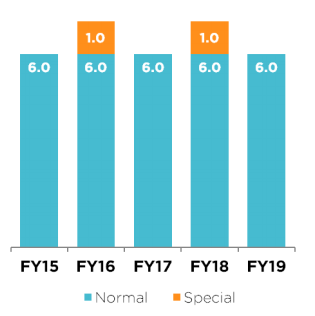

In May 2019, the company secured a new syndicated multi-currency facility worth $225 million to fund the acquisition of Sigma Systems. As at 30 June 2019, $35.5 million of the facility was unused. The company’s capital management policy is centred around maintaining a balance between retaining flexibility to fund growth through acquisitions against the payment of dividends. In FY19, the company distributed normal dividends amounting to 6.0 cents per share, in-line with the previous year’s normal dividend.

Dividend (Source: Company Reports)

Some of the key operational highlights of the period included a major contract to deliver EnoroCX billing product in Finland, a contract to deliver the Meter Data Management product in Sweden, acquisition of Sigma and expansion of the development centre in Vietnam.

Highlights of Acquisition: As discussed in the above section, the acquisition of Sigma Systems was a key highlight of the period. The deal is the biggest to date and provides a scope to significantly expand the business scale in the communications sector along with cross-sell opportunities in the energy sector. The company acquired Sigma Systems for a consideration of $163.8 million, which was funded from a new loan facility of $225 million. Adding Sigma to the platform, Hansen can now address a bigger part of its customer needs in terms of managing their end users. Moreover, the acquisition has helped the company to rebalance its business structure which was earlier weighted towards the utilities sector after integration of Enoro.

Some of the key priorities for FY20 include, complete integration of Sigma into the broader Hansen platform, developing cross-selling opportunities into the Utilities market and leveraging the Group’s network of low-cost development centres to improve customer delivery and Hansen margins.

Recent Updates:

Update on Business Structure: As per a recent announcement to the exchange, HSN’s business is now formally structured around two verticals, Utilities and Communications. Earlier, the business was weighted towards the utilities sector due to Enoro. Post-acquisition of Sigma Systems, which has a customer base primarily in the Communications sector, the company’s revenue is now equally balanced between the two verticals. The company notified that Niv Fernando will be heading the Utilities division, comprising energy and water customers. Simon Muderack will be the CEO for the communications division, comprising telecommunications and pay-tv customers.

Appointment of Director: The company recently appointed Don Rankin as a Non-Executive Director on the Board, with effect from 21 November 2019. With a strong experience in finance and governance, Don will add additional capabilities to the existing Board.

Contract with Aurora Energy: Recently, the company inked a deal with Aurora Energy, for the implementation of HubCX, HSN’s Australian-compliant energy billing product. The product has been significantly enhanced over the past few years, to boost its flexibility and configurability.

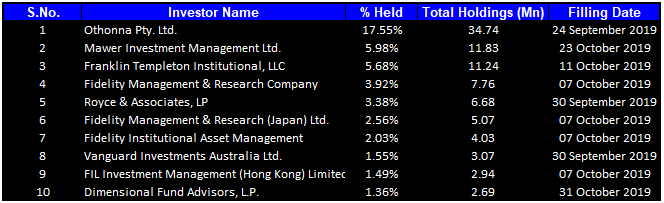

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form around 45.49% of the total shareholding. Othonna Pty. Ltd. is the entity, holding maximum shares in the company at 17.55%. Mawer Investment Management Ltd. is the second largest shareholder, with a holding of 5.98%.

Top Ten Shareholders (Source: Thomson Reuters)

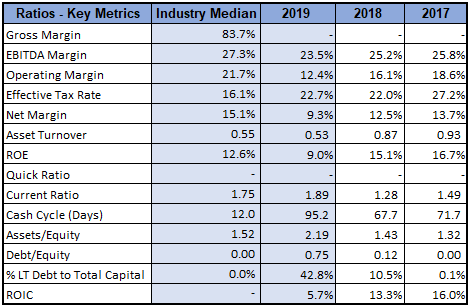

Key Metrics: In FY19, the company had an EBITDA margin and net margin of 23.5% and 9.3%, respectively. Current ratio for the year was reported at 1.89, better than the industry median of 1.75. The ratio also stood higher than the previous year’s current ratio of 1.28. This implies that the company is now in a better position to address its short-term financial liabilities. In FY19, the company demonstrated its financial strength by generating an operating cash flow amounting to $39.7 million, which was used to retire external debt and fund dividends of $12.6 million.

Key Metrics (Source: Thomson Reuters)

What to Expect: As per the management’s guidance, operating revenue for FY20 is expected to be in the range of $305 million - $310 million. EBITDA for the period is expected to be between $70 million and $76 million.FY20 results will reflect full year contribution from Sigma, which has brought in various opportunities for growth. The company has stepped into FY20 with great momentum, following new market entries for Sigma in India and Hong Kong. During the initial months, the company has seen multiple favourable events such as addition of Vocus as a new customer for Sigma in Australia, first cross-sell by Sigma into the energy customer base, contract from Aurora Energy, etc. With its expanded product portfolio through acquisitions, the company will now be able to extend better support to its customers.

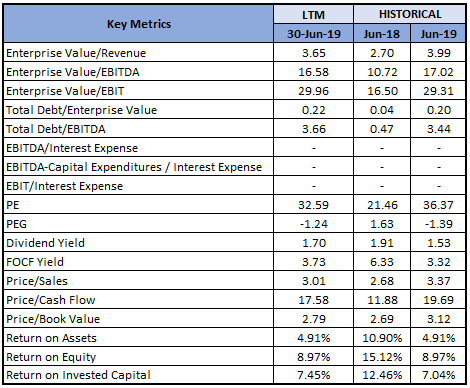

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

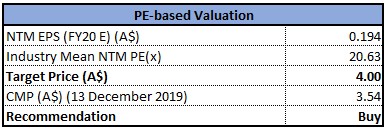

Method 1: Price to Earnings Multiple Approach:

Price/Earnings Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

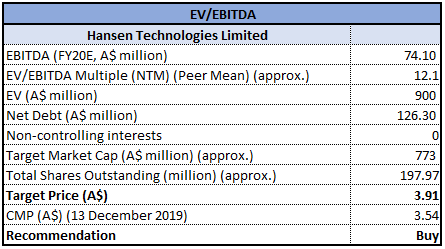

Method 2: Enterprise Value to EBITDA Multiple Approach:

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The stock of the company generated positive returns of 1.73% and 6.34% over a period of 1 month and 3 months, respectively. Currently, the stock price is nearing the average of its 52-week trading range of $2.850 - $4.290. Although the numbers in FY19 do not speak much about the company’s capabilities, the period was characterised by several operational highlights that provide confidence in the performance. Moreover, the financial results for the year were also in-line with the guidance provided by the management. During the year, the company managed to pay dividends despite raising a loan to acquire Sigma Systems. Enoro, which has been completely integrated into the Hansen platform, delivered robust results. Sigma Systems will further add growth to the business with an expanded product portfolio meeting customer needs in a better manner. Along with the payment of dividends, the company managed to discharge its external debt, which speaks volumes about its cash generation capability. Operating revenue and EBITDA guidance issued for FY20 depict decent growth over FY19, reflecting a full-year contribution from Sigma Systems. Considering the operational performance in FY19 in terms of acquisitions, new contracts, product expansion etc, strong cash generation capacity, anticipated benefits from newly signed contracts and acquisitions, decent guidance for FY20 and current trading levels, we have valued the stock using two relative valuation methods, i.e., Price/Earnings multiple approach and EV/EBITDA multiple approach, and arrived at a target price with lower double-digit upside (in % terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $3.540, up 0.568% on 13 December 2019.

.jpg)

HSN Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...