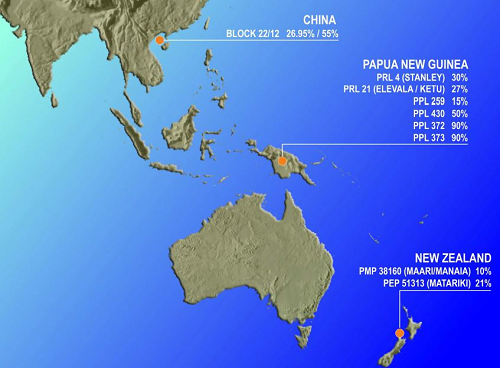

Company Overview- Horizon Oil Limited is engaged in petroleum exploration, development and production. The Company operates in five segments: New Zealand development, New Zealand exploration, China exploration and development, PNG exploration and development and other segments. New Zealand development is engaged in producing crude oil from the Maari/Manaia fields, located offshore New Zealand. New Zealand exploration is engaged in the exploration and evaluation of hydrocarbons in two offshore permit areas, PEP 51313; and PMP 38160 Maari/Manaia. China exploration and development is engaged in developing and producing of crude oil from the Block 22/12-WZ6-12 and WZ12-8W oil field development and in the exploration and evaluation of hydrocarbons within Block 22/12. PNG exploration and development is engaged in the Stanley condensate/gas development, and the exploration and evaluation of hydrocarbons in six onshore permit areas, PRL 4, PRL 21, PPL 259, PPL 372, PPL 373 and PPL 430.

Analysis– December 13 quarter production of 0.39 mmbbl was 35% above the September 13 quarter. With Maari off line for the majority of the quarter the increase has been driven by the Beibu producing at an average rate of 14,816 bopd, close to the expected plateau production of 15,000 bopd. Sales revenue of US$35.9m was up 17% quarter on quarter. 2014 will see a busy period of exploration, appraisal and development. The March quarter will benefit from a full quarter of production from both China and Maari with the installation of electronic submersible pumps (ESP’s) on 5 of the wells to support production in China and development works at Maari to grow production to 20,000 bopd throughout the year. Award of a Petroleum Development License (PDL) at Stanley (PNG) will see the start of infield work and PNG activity will also include an exploration well in PRL 259 in the second half.

HZN delivered a strong result in the December Quarter, with increased production from china, re-start of production in Maari at higher rates and the testing of a significant discovery at Tingu-1 (PNG). Whilst award of a Petroleum Development License for Stanley missed the year-end target progress was made and the ward is expected shortly. Given the significant progress made in the 2H 2013 we believe that award of a PDL for Stanley will lead to a re-rate for HZN given the minimal value factored in for its PNG portfolio at present. Production was up 35% for the quarter to 386kbbls (286kbbls, September Quarter) with 15 wells online for the quarter in China delivering a gross 14,816bopd (up 37%) and with the restart of Maari production late in the quarter. Next quarter will be stronger with a full contribution from both assets. Revenue was up again at $35.9m ($32m, Sep Q) given higher sales volume of 343kbbls (299kbbls, September Quarter). After close to $40m in expenditure HZN finished the period with cash lower at $37m and its reserve based lending facility steady at $134m.

Daily Chart HZN (Source - Company Reports)

Daily Chart HZN (Source - Company Reports)

In our view Horizon’s oil production should more than double in the FY14 due to a full year of oil production from Beibu Gulf project. Offsetting this number of challenges and steps lie ahead for an LNG project in PNG to achieve final investment decision. These include completing front end engineering and design (FEED), JV project agreement, proving up further gas, signing gas sales agreements, obtaining financing and obtaining regulatory approvals. Based on this FID is likely to be at least three years away in our view.

Further clarity on gas commercialisation in PNG can lead to an upside scenario for the stock.. Horizon has material gas resources in PNG and progress on the commercialisation of gas is ongoing. We see multiple options for commercialising this gas including domestic sales and potential for an LNG option with JV partners Talisman and Mitsubishi. We expect oil prices to remain at elevated levels moving towards our long term Brent assumption of US$92/bbl over the next four years. We expect the link between oil prices and natural gas prices to remain in international markets. Global demand growth for oil is expected to be low at 1%, while natural gas it is expected to be between 2-3%.

Geographical Focus & Asset Location (Source – Company Reports)

Geographical Focus & Asset Location (Source – Company Reports)

There is a full quarter of production from China and planning for Phase 2 is underway. Development works were complete during the last quarter with all 15 wells permanently tied into the facilities and averaged 14,600bopd over the period. Five of the 15 wells are currently flowing back naturally and will be put on ESP in due course. On the back of the very successful execution of Phase 1 project, planning for the Phase 2 development of the project was immediately underway. The phase 2 will see the development of the WZ12-8E field utilising a leased mobile production platform. Processing of a recently acquired 3D seismic survey continued during the quarter and interpretation of a fast track set is nearing completion with the data quality reportedly good.

Production resumed at MAARI on 12

th December and stabilized on the 17

th at a gross rate of 11,600bopd. While this rate could decline in the short term, it would increase significantly towards 20,000bopd throughout the next 12 months as additional wells are drilled and tied in as part of the Greater MAARI development works. The Greater MAARI Area development program got underway during the quarter. The bulk of the program will commence this quarter with the arrival of Ensco 107 in March.

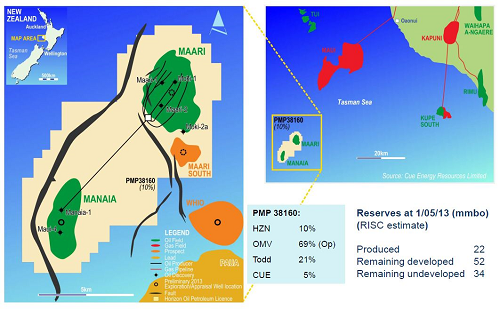

MAARI + MANAIA Fields – New Zealand (Source – Company Reports)

MAARI + MANAIA Fields – New Zealand (Source – Company Reports)

We are still waiting on the Stanley PDL, the outstanding issues are execution of a Gas Agreement and convening a development forum with land owners, are the same issues that were outstanding 12 months ago. Horizon has issued the PDL application to the PNG state solicitor for formal legal clearance prior to submission to the PNG cabinet for approval which we understand could happen any time from now as the cabinet meets on a weekly basis. Production was up 35% quarter on quarter to 0.39 mmbbl thanks to Beibu with MAARI offline for the majority of the quarter. Sales revenue of US$35.9m was up 17% quarter on quarter. Beibu produced 14,816 bopd for the December quarter very close to the expected plateau rate of 15000bopd. All 15 wells are now online and five of the fifteen are flowing naturally. We will be putting a BUY on the stock at the current price of $0.335.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Please wait processing your request...

Please wait processing your request...