CompanyOverview – Iluka Resources is the leading global mineral sands miner with high grade low cost production mainly in Australia. It is the largest global producer of Zircon and second largest producer of titanium dioxide feedstock. Low costs are underpinned by the high grade Jacinth-Ambrosia mine in South Australia and Murray Basin operations in Victoria. Reserve life is about 10 years based on 2011 production levels, but well over 30 years based on resources. A royalty over BHP’s mining area C offers high quality cash flow.

Analysis– As a leading global player in both zircon and titanium minerals markets, long term growth in sales volume is dictated by overall industry growth. The high grade Jacinth-Ambrosia mine accounts for nearly half of group revenue. It brings cost advantage over zircon producing competitors due to high grades , concentration of Zircon relative to other deposits and a simple mining process. The 10 year reserve life is short but it will likely be extended by mining of lower grade resources at higher cost. The low cost Murray operations are the key source of rutile. Competitive advantage is less in downstream processing, but returns are generally strong with capital costs sunk.

Global Mineral Sands Operations (Source - Company Reports)

Global Mineral Sands Operations (Source - Company Reports)

Conditions remain weak for Iluka with first quarter 2014 mineral sands sales down 7% on the previous corresponding period to AUD 131 million. Iluka is moderately undervalued given the depth of the cyclical low and the business should again enjoy pricing power once demand starts to meaningfully recover. If there is to be a global recovery in housing and construction, Iluka is well placed with tiles and paint being demand drivers for zircon and rutile respectively. Sales volumes have declined to levels below global financial crisis levels and a meaningful cyclical recovery is highly likely with customer inventories back to normal levels.

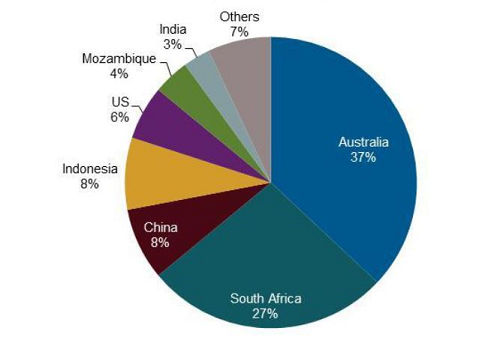

Zircon mining by region (Source - company Reports)

Zircon mining by region (Source - company Reports)

Major growth capital expenditure is behind Iluka and maintenance capital expenditure relatively modest. The company has numerous expansion projects to enhance life and to a lesser degree output. Conversion of resources to reserves is an obvious path to life extensions, but when high grade reserves are exhausted in 10 years, likely lower grade and higher cost resources will impact profitability. The emergence of Chinese demand, plus a change in marketing strategy to service smaller customers, individually insignificant but numerous and collectively important, harnessed Iluka’s latent pricing power. Iluka intends to maintain a conservative balance sheet to finance inventory build and provide the flexibility to invest through the cycle. Management values cash returns to shareholders primarily via dividends but also potentially capital returns and buy backs.

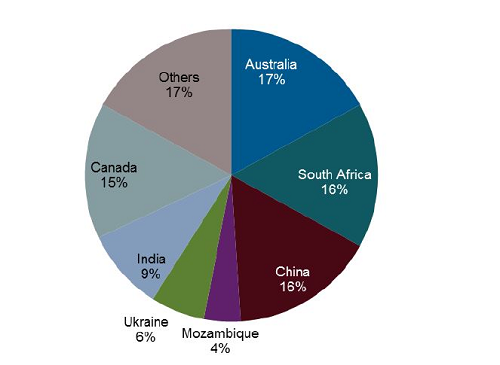

Titanium Dioxide mining by region (Source - Company Reports)

Titanium Dioxide mining by region (Source - Company Reports)

Iluka has reiterated production and sales guidance in last month’s AGM expecting to produce 550kt of Zircon/Rutile/Synthetic Rutile for CY2014. As previously guided ILU expects CY2014 Zircon/Rutile/Synthetic Rutile sales volume to exceed CY2014 production (inventory being drawn down) and CY2013 sales volume of 584kt. Year to date cash and non-cash costs and CAPEX are trending at or below previous guidance. Relative to DecQ13 average Zircon prices of US$1,080/t FOB, there has been no material change to average prices received in the year to date. According to Asian Metals, average zircon prices for premium Australian Zircon are stable having only increased by 1% in the past 6 months. Price erosion on rutile also appears to have moderated.

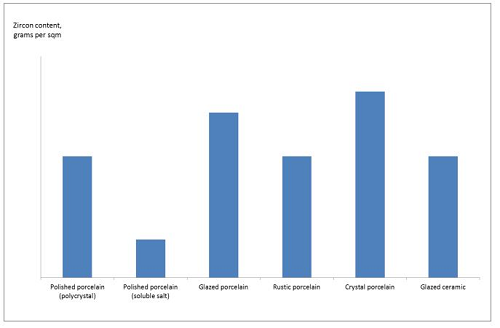

Zircon content in tiles (Source - Company Reports)

Zircon content in tiles (Source - Company Reports)

ILU has confirmed that subdued market conditions in Europe, Asia (ex-china), India and the Middle East have impacted sales for 1HCY2014. Zircon sales for CY2014 year to date are currently running below previous corresponding period. Zircon sales for 2HCY2014 are expected to be higher than the same period last year. We are not surprised about improved sentiment around the Tio2 market given recent commentary from pigment producers around inventories and plant utilization rates. Furthermore US housing starts the key leading indicator for titanium dioxide demand, in our view has continued to trend upwards during the past year. Despite the YTD pricing for rutile being below the US$980/t achieved in 4QCY13, the positive commentary around it gives us greater confidence in our US$1000/t forecast for rutile in 2HCY14. We continue to see US housing starts as a leading indicator for Tio2 demand given that the largest end user of TiO2 is pigments used in paint for housing construction. US Housing starts in April 2014 were up 26% from the previous corresponding period.

ILU daily chart (Source - Thomson Reuters)

ILU daily chart (Source - Thomson Reuters)

The primary source of competitive advantage for a miner is low cost production. Iluka’s margins are strong relative to the industry, due to high grade deposits weighted to higher value products Zircon and rutile. Reserve life is shorter than we would like at around 10 years but the resource base is significantly larger and sufficient to satisfy 30 to 40 years of operations. The company has a history of converting resources to reserves by drilling out, advancing and developing new deposits close to existing processing infrastructure. We expect this track record to continue. Lower grade resources are likely to become economic over time as the industry mines the best deposits and average grades fall. A sufficiently favorable interaction between price and industry costs would incentivize investment in the next generation of lower grade deposits of which Iluka holds significant exposure in first world locales.

Iluka is an industry leader with some of the richest and most prolific producing zircon and rutile deposits in the world. As a low cost producer with assets in the first world locales, Iluka is able to withhold supply to defend prices and margins in times of weak demand. Management has turned company fortunes around with a strong focus on returns on capital and a marketing effort which harnesses latent pricing power. The revenue mix is appropriately half from zircon and half from high grade titanium products (rutile and synthetic rutile). Geographically, Iluka’s revenue is almost evenly split between North America, Europe, China and the rest of Asia. A lack of exploration and investment in new mines is likely to constrain new supply and assists medium term returns. It will take time for competitors with undiscovered or generally inferior, undeveloped deposits to reach production. The royalty over BHP’s mining area C is a low risk, long life and high margin asset, providing a robust and potentially growing cash flow with no investment required. We believe the start of recovery in Titanium dioxide and zircon markets in CY14 will drive the share price over the next year. We believe Iluka offers potential upside to valuation, improving industry dynamics and good management. We put a BUY on the stock at the current price of $8.32.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...