Kalkine has a fully transformed New Avatar.

Company Overview: Infomedia Ltd (ASX: IFM) is a technology-based company, which is engaged in the development and supply of Software as a Service (SaaS) offerings. The company's operating segments are in the Asia Pacific region, EMEA and the Americas. The Company offers numerous solutions, such as Parts and Service, Data Management and Future Motors, to name few. Infomedia's Parts and Service solutions consist of Microcat, Superservice Menus, Superservice Triage, Superservice Insight, Superservice Connect, Superservice Register, and Microcat Market, etc.

.png)

IFM Details

.png)

Geographical Expansion & Higher Investment Aids IFM: Infomedia Limited (ASX: IFM) is engaged in the development and supply of Software-as-a-Service & provision of data analytics solutions to the parts and service sector of the automotive industry. In 2019, the company witnessed an outstanding year by delivering its objectives to drive growth and innovation at its workplace. The year was marked by the company’s enhanced performance, increased innovation, and service to leverage global opportunities and higher investments to take advantage of key trends disrupting the global automotive industry.

In 2019, the company delivered robust growth with improved margins. It remained committed to invest in people, products, processes, and new technology, which aided the company to achieve its growth strategies. During the year, the company completed the roll-out of Nissan global electronic parts contract and extended its tie-ups with automotive manufacturers globally. It also introduced new products to existing partners, to new partners and to new markets. The company had completed the acquisition of Nidasu, which aided IFM to support more than 30 top global automotive manufacturers in Australia. The company remains on track to leverage the Australian and APAC experience and strengthen its foothold in the wider portion of the market and drive growth in this area. The company’s revenues and earnings increased 16% and 25% year over year, respectively in FY19. Net profit after tax for the year also increased 25% over the year, while EBITDA margin continued to expand from 40% to 45%, reflecting an improvement in delivery and efficiencies resulting from scale across the business. The company has a strong financial position with cash balance increasing 17% from the prior financial year to $15.5 million, reflecting the robust cash generative nature of the business. It is worth mentioning that the company has a debt-free balance sheet.

The company has a track record of consistent growth in revenue, profitability and returns to shareholders. It reported a CAGR of 8.8% and 5.1% in revenue and NPAT, respectively, over FY15-FY19. It paid a final dividend of 2.15 cents per share in FY19, increasing 26% on pcp.

.png)

Past Performance (Source: Company Report)

The company entered FY20 with a positive stance and expects higher traction from its mature product, Microcat, used by many customers and generating a significant portion of revenue, along with the immature product, Superservice, used in a fragmented market. The group continues to make investments in the products and regions that have the potential for sustainable growth in the near future. The group’s core areas include SaaS business model. This growth potential foreseen in the group’s business is enabling it to invest in infrastructure and resources to build a larger and more resilient organization. The company expects to deliver continued double-digit growth in both revenue and earnings in FY20. We opine that IFM is likely to continue its current growth trajectory and leverage on growth opportunities from the emerging automotive industry, through its strong execution.

Robust Interim Results: In 1HFY20 for the Period Ended 31st December 2019, Infomedia’s net profit after tax (NPAT) surged 24% year on year to $9.04 million. The group’s revenue rose 19% year over year to $47.89 million. During the period, the company continued to invest in both the platform and additional functionality in its core parts and service products. In 1HF20, more than 95% of revenues were recurring in nature. EBITDA for the period increased 35% year over year and came in at $22.89 million, while cash EBITDA went up by 45% from the prior corresponding period. Earnings per share for the period came in at 2.86 per share, up 21% year over year. On the back of continuous investment in business development, IFM has built a strong top-line growth.

.png)

1HFY20 Key Highlights (Source: Company Reports)

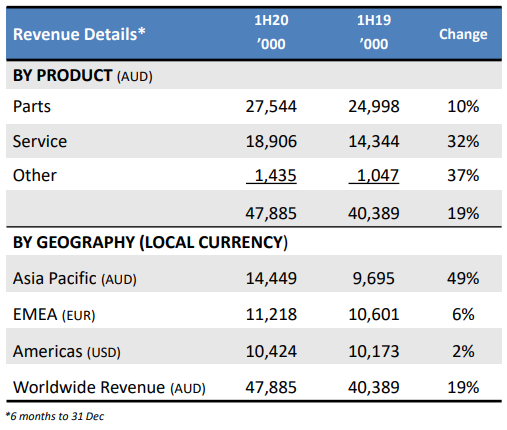

Revenues From products & Geographical Highlights: As per the regional performance, Americas segment delivered revenue growth of 2% on reported currency terms while Asia pacific segment’s revenue enhanced 49%. EMEA segment’s revenue went up 6% on reported currency terms while enhanced 19% yoy on local currency basis. Product-wise, the company generated $27.5 million from parts products, which increased 10% year over year. Service revenues went up 32% year over year and came in at $18.9 million.

Product & Geography Highlight (Source: Company Reports)

Market opportunities: The group is well-positioned to leverage two major growth industries - Software as a Service, or SaaS, and the rising parts and service sectors of the global automotive industry. Being a top SaaS provider, the company has eminence opportunity to tap on ongoing opportunities to support the growth of the customers and the brands. On the other hand, management is expecting to maintain the underlying growth momentum for the year on year revenue and profitability growth. The group is focusing on developing a high performing and customer-centric culture. The company is one of the few worldwide software providers in parts, service, and data insights to the global auto industry. Notably, more than 80% of revenues are generated from outside Australia. Given that the automotive original equipment parts and services market worldwide, the company’s future looks promising. Reliance of Automotive manufacturers on high margin original parts sales and brand loyalty are rising via good customer service. On the flip side, keeping brand loyalty from one purchase to another is a major task for the automotive manufacturer as they rely on a consistent service experience across many franchised dealerships.

Balance Sheet & Cash Flow Highlights: The group has also built a decent balance sheet position with total assets reaching $101.8 million as at 31 December 2019. IFM has a cash and cash equivalents of $17.2 million, which grew 10.7% as compared to June 2019, reflecting the cash generative nature of Infomedia’s business. The company declared an interim dividend of 2.15 cents per share, up 23% pcp (70% franked).Net cash from operating activities came in at $14.7 million for the period ended 31 December 2019.

Cash Position (Source: Company Report)

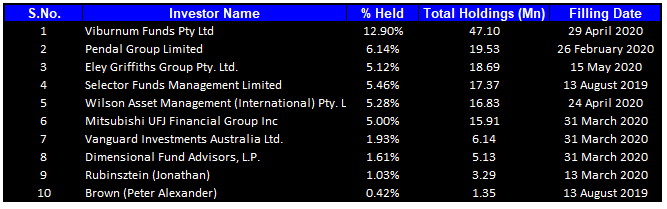

Recent Updates: In a recent update, the company announced that Eley Griffiths Group Pty Limited, became a substantial holder of the company, with a voting power of 5.12%. In another update, the company stated that Viburnum Funds Pty Ltd, a substantial holder of the company, has decreased its voting power from 14.69% to 12.9%.

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form around 44.89% of the total shareholding. Viburnum Funds Pty Ltd held the maximum number of shares with a percentage holding of 12.9%, followed by Pendal Group Limited holding 6.14% of the shares.

Top Ten Shareholders (Source: Refinitiv, Thomson Reuters)

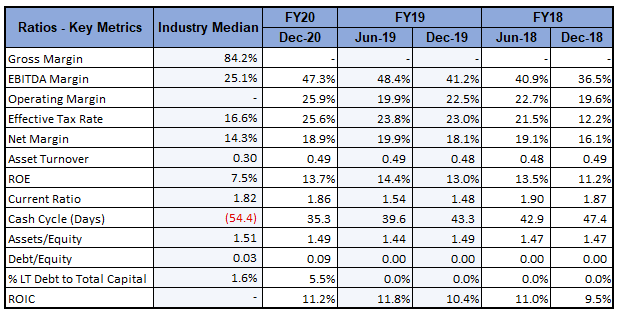

Key Metrics: For the half-year ended 31 December 2019, the company reported EBITDA margin of 47.3%, which is higher than the industry median of 25.1%. Net margin for the same period stood at 18.9%, higher than the industry median of 14.3%. The company improved on its short-term liquidity with a current ratio of 1.86x in 1HFY20, as compared to a current ratio of 1.48x in the prior corresponding half.

Key Metrics (Source: Refinitiv, Thomson Reuters)

Outlook: The company remains on track to gain synergies from acquisition and will continue to invest in people and technology in order to raise sales and provide more value to the current customers. The company expects to deliver low double-digit growth in revenue and earnings in FY20. Further, expansion in the Americas and the implementation and roll-out of data prospects are likely to contribute potential upside in its FY20 financial performance. The company further opines that it will grow by leveraging its core assets, and exploring acquisitions, that, in turn, will aid the company’s ability to stay ahead of the competition and compete globally.

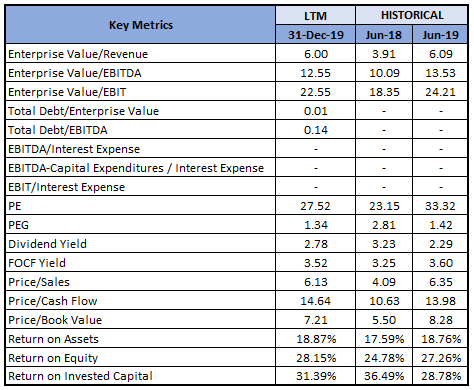

Key Valuation Metrics (Source: Refinitiv, Thomson Reuters)

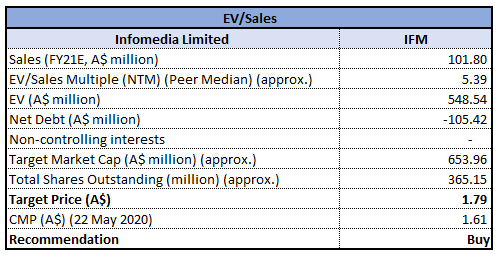

Valuation Methodologies: EV/Sales Multiple Based Relative Valuation (Illustrative)

EV/Sales Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company corrected by 25.72% in the past three months and is currently trading below the average of its 52-week low and high level of $1.2 and 2.48, respectively. The company has a market capitalisation of ~$564.15 million, with a P/E multiple of 27.15x and an annual dividend yield of 2.78%. Management believes that the contracted global sales momentum would drive the firm’s potential revenue growth. The group is targeting growth in all markets and products. We have valued the stock using EV/Sales multiple based illustrative relative valuation method. For the said purpose, we have considered peers like Audinate Group Ltd (ASX: AD8), Citadel Group Ltd (ASX: CGL), Hansen Technologies Ltd (ASX: HSN) to name a few. As a result, we have arrived at a target price with an upside of lower double-digit (in percentage terms). Considering the above-mentioned factors, we give a “Buy” recommendation on the stock at the current market price of $1.61, up 4.207% on 22 May 2020.

IFM Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...