Kalkine has a fully transformed New Avatar.

Company Overview: Link Administration Holdings Limited is a technology-enabled provider of outsourced administration services for superannuation fund administration, corporate markets and related value added services, including data management analytics, digital communication and stake-holder education and advice. Its segments include Fund Administration, which provides administration services to superannuation funds; Corporate Markets, which provides an integrated corporate market offering that connects issuers with their stakeholders and offers services, including shareholder management and analytics, stakeholder engagement and company secretarial, and Information, Digital and Data Services, which provides core services of development and maintenance of information technology (IT) systems and platforms, and value-added services of data analytics, digital solutions and digital communications. It provides platform solution to its clients, covering front, middle and back office administration functions.

.png)

LNK Details

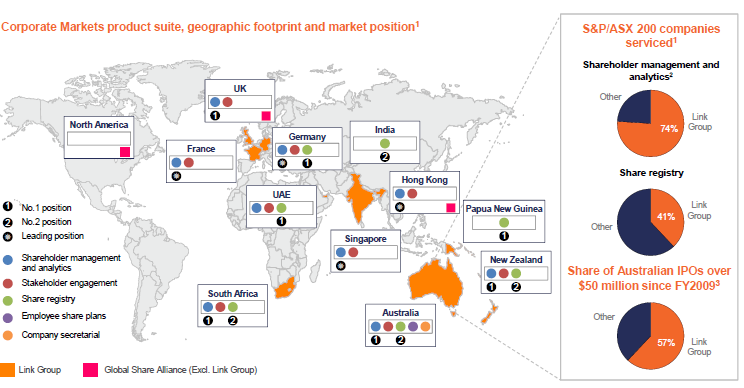

Diversified Business Model: LNK Administration Holdings Limited (ASX: LNK) is a leading technology-enabled company. It is one of the market leading administrators of financial ownership data, with strengths underpinned by investment in technology, people and processes. Currently, LNK offers its services to approximately 10 million superannuation account holders and over 35 million individual shareholders. With the operations in 18 jurisdictions worldwide and Australia being its largest market, the company caters to more than ten thousand clients globally. The group’s business segments include Fund Administration, Corporate Markets, Technology & Innovation (T&I), Link Asset Services, and Property Exchange of Australia (PEXA). In terms of revenue contribution in 1H19, Link Asset Services and Fund Administration remained the highest revenue contributor with 37.0% and 33.0% respectively, followed by the other two segments T&I, and Corporate Markets contributing 16.0% and 14.0% revenue, respectively. The Group is a leading player in all key markets in which Corporate Markets operates. Australia is the largest market, with Australia and New Zealand contributing ~70% of the division’s FY2018 revenue. The company faces near term challenges from the regulatory environment and revenue generation from the Fund Administration segment in the short term, however, the underlying business drivers of the company remain resilient to combat these issues.

Leading Player With Extensive Geographical Footprints (Source: Company Reports)

Revenue Model & Segment Snapshot: The group operates through four business segments, including Fund Administration, Corporate Markets, Technology & Innovation (T&I), and Link Asset Services (LAS). On the segmental front, the fund administration segment has core services involving, stakeholder education and advice, core administration services, value-added data management and analytics. The revenue model is contract based, (typically 3 to 5 years) where the clients are charged a weekly fee per member invoiced monthly.

The corporate market segment has a base of more than 30 million individual shareholders. It has services involving the shareholder management and analytics, stakeholder engagement, share registry, and employee share plans. The revenue model is contract based typically with 2 to 3 years. It includes margin income and incomes from corporate actions.

The Technology & Innovation (T&I) segment deals with more than 40 million financial records. The services are related to core systems development and maintenance, digital communications and solutions and data analytics. The company generates revenue from supporting other divisions and external clients charging fee-for-service and licence fees.

And, the Link Asses Services (LAS) segment has a base over seven thousand clients. It operates in areas including fund solutions, link market services, corporate & private client solutions, and banking & credit management. The revenue varies across divisions including a combination of fixed, activity based & asset related fees.

Property Exchange of Australia (PEXA) is an e-conveyancing platform acquired by the Group with consortium partners- Commonwealth Bank of Australia and Morgan Stanley Infrastructure. LNK as a part of the transaction increased its equity in PEXA to 44.2% with a fair value of this investment at $715 million. The increased stake will provide a new dimension for growth to the company on the back of an increase in volumes and the benefits of PEXA’s technology.

Segment wise revenue contribution in 1HFY19 (Source: Company Reports)

Key Growth Drivers: The company continues to execute a proven growth strategy and precisely is focussed on five key drivers. The company thrives on growing in attractive markets with innovating the products & services, expanding its clients along with products & regional boundaries, seeking integration and efficiency benefits and identifying adjacent market opportunities.

The company maintains and enhances existing client relationships through the expansion of cross-selling opportunity from larger global networks. It supports several services excellences and continues to actively assess a range of corporate and other actionable targets.

Key Growth Drivers (Source: Company Reports)

Adoption of New Standards: Under AASB 9 Financial Instruments, the company introduced a new expected credit loss model for calculating impairment on financial assets (e.g., trade receivables) and new general hedge requirements effective from 1 July 2018. No material impact on the group is expected, considering the historic low level of trade receivable impairment and no hedging arrangements.

Under AASB 15 revenue from contracts with customers, the company introduced new revenue recognition requirements with contract fulfilment costs recorded as contract assets and advance payments recorded as contract liabilities, effective from 1 July 2018. As an impact of the policy, the contract fulfilment assets (e.g. client migration costs) will be amortized over the term of the client contract. Contract liabilities will be recognised as revenue when the performance obligation is satisfied (previously recognised as received/incurred). The initial retained earnings of the company were increased by $5.1 million as a result of the first-time recognition of contract fulfilment assets and contract liabilities.

Under AASB 16, with regards to leases (effective from 1 July 2019), there will be no distinction between operating leases and finance leases. Nearly all lease assets and liabilities will be recognised by LNK on the balance sheet. This will, in general, impact the lease accounting, however, the impact on the future financial periods is under review.

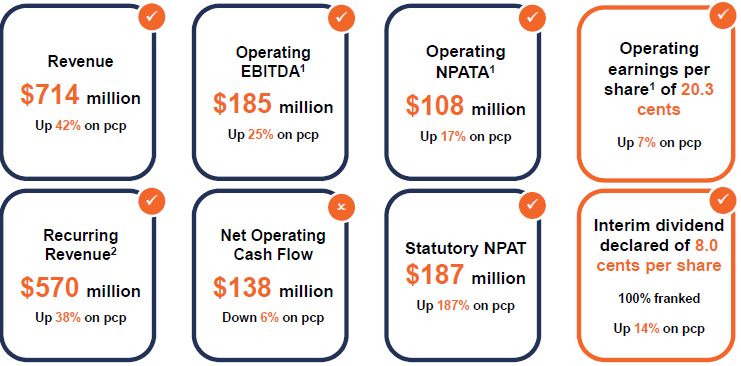

Key Financials Performance: The company experienced a mixed operating performance in 1HFY19, however, is expected to witness an improvement, going forward. The statutory net profit after tax went up by 187% in 1HFY19 as compared to the prior corresponding period. The increase was primarily, driven by the inclusion of LAS as well as a one-time benefit from the revaluation of the initial 19.8% equity held in PEXA (prior to the completion of the acquisition by Link Group and its consortium partners in January 2019). The operating EBITDA excluding LAS was 25% ahead of the prior corresponding period (pcp) to $185.4 million in 1HFY19.

Recurring Revenues represented ~80% of the total group revenue. Although, it decreased as a percentage of total revenue with the inclusion of LAS, however, the recurring revenue remains a key feature across the business for its success. Excluding LAS, the group revenue increased by 1.8% on pcp, reflecting a strong member growth in Fund Administration, offset by the impact of lower project related revenue and client losses, and a good contribution from corporate markets.

Key Financial Highlights (Source: Company Reports)

The net finance expense of the company increased substantially, reflecting a more normal level of gearing during 1HFY19. The operating expense increased during the period, reflecting the inclusion of LAS.

On the cash flow front, the net operating cash flow in 1H 2019 stood at $138.0 million, a decrease of 6.0% over the prior corresponding period, primarily, impacted by a large draw on working capital. The increase in capex reflected the full period inclusion of LAS, coupled with spending on new systems and technology refresh programs.

Turning to the balance sheet, the company maintained a comfortable level of gearing. Net debt increased during 1H 2019, following the investment in Leveris. However, the increased investment and borrowings related to PEXA, completed in January 2019, was not reflected in the balance sheet for the period. The proceeds from the divestment of Corporate & Private Clients business (CPCS)are expected to reduce the leverage of the company towards the lower end of the guidance range. After adjusting for PEXA and the sale of CPCS, the Net debt to Proforma LTM (Last twelve months) operating EBITDA stood at ~1.8x, which is in the bottom half of the guidance range of 1.5x to 2.5x.

.png)

Key Ratios (Source: Thomson Reuters)

Top 10 Shareholders: Top ten shareholders form around 44.34% of the total shareholding as highlighted in the below table. AustralianSuper, Macquarie Investment Management Ltd. holds maximum interest in the company with a stake of 7.24% and 5.24% respectively, followed by Pinnacle Investment Management Group Ltd. and Challenger Managed Investments Ltd. with 5.15% and 5.12% respectively.

.png)

Top Ten Shareholders (Source: Thomson Reuters)

Key Risks: The company faces near term challenges from the regulatory environment, but it has longer term opportunities which can have a cascading impact on its clients as well. Fund Administration revenue is likely to be challenged in the short-term as known client losses and account consolidation work through the system. However, the underlying business drivers of LNK remain strong.

Outlook Ahead: LNK is well positioned for growth supported by future earnings. On the operational front, the company has a good organic pipeline of opportunities across its business. It maintained focus on delivering high-quality service & innovative solutions for existing and new customers. The company continues to assess several opportunities to complement its current operations. The business is well positioned to perform under a range of Brexit scenarios. The company has its presence in a number of European jurisdictions, with Brexit continue to provide challenges and opportunities. The business will remain focused, supporting its clients in the changing environment and is well positioned to perform under a range of Brexit scenarios as well.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

EV/EBITDA Multiple Approach (NTM):

.png)

EV/EBITDA Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

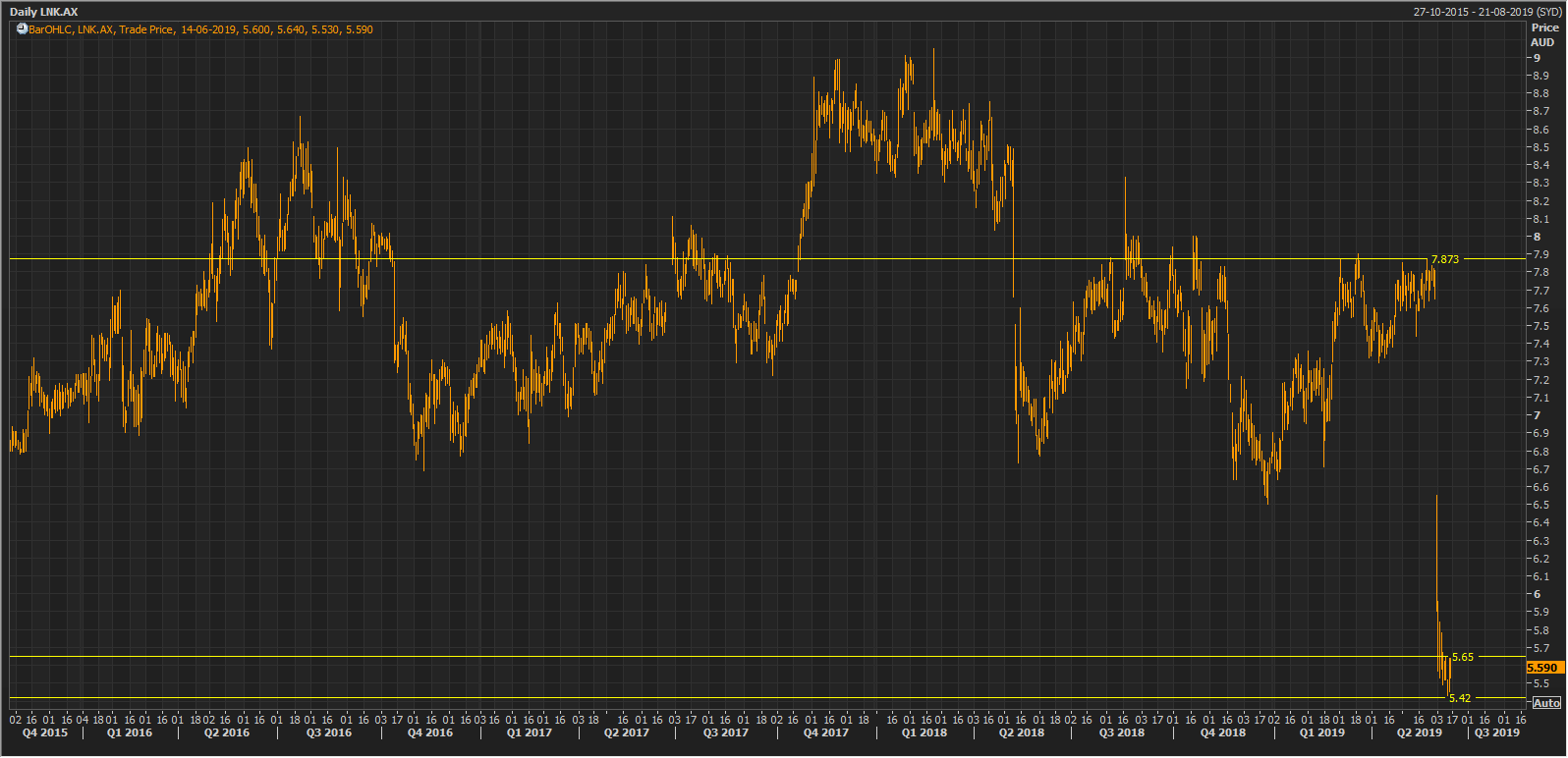

Stock Recommendation: The stock has yielded a negative YTD return of 16.42%. With a PE multiple of 11.10x, the stock is currently trading closer to its 52-week low range. LNK has several competitive advantages and robust business drivers on which it can thrive to achieve growth, going forward. Diversified business segments, strong organic pipeline, proven growth strategies along with a diversified business line and continued earnings momentum available through disciplined cost management mark the company as a resilient performer in its segment and a stock to look at. Hence, we recommend to “Buy” the stock at the current market price of $5.590 (down ~0.179% as on 14 June 2019).

LNK Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...