Kalkine has a fully transformed New Avatar.

Company Overview: Link Administration Holdings Limited is a technology-enabled provider of outsourced administration services for superannuation fund administration, corporate markets and related value added services, including data management analytics, digital communication and stake-holder education and advice. Its segments include Fund Administration, which provides administration services to superannuation funds; Corporate Markets, which provides an integrated corporate market offering that connects issuers with their stakeholders and offers services, including shareholder management and analytics, stakeholder engagement and company secretarial, and Information, Digital and Data Services, which provides core services of development and maintenance of information technology (IT) systems and platforms, and value-added services of data analytics, digital solutions and digital communications. It provides platform solution to its clients, covering front, middle and back office administration functions.

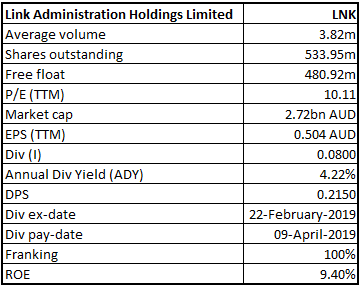

LNK Details

Continued Commitment to Client Relationships: Link Administration Holdings Limited (ASX: LNK) is a market-leading provider of technology-enabled administration solutions. The company’s core businesses of fund administration and securities registration are complemented by expertise in digital solutions and data analytics. The company has significant operations across four divisions, namely Fund Administration, Corporate Markets, Technology & Innovation, and Link Asset Services (LAS). Until FY18, the company’s international activities were largely concentrated in Corporate Markets across a number of locations including Hong Kong, India, Dubai, South Africa, and many more. The company also established a Fund Administration operation in New Zealand. Revenue from international operations in FY18 represented 40% of the total revenue as compared to 10% in FY17.

With respect to the acquisition of Link Asset Services, the company further expanded its international operations through the acquisition of Link Asset Services in November 2017 for a total consideration of $1,548 million. The acquisition of LAS provides the company with a large-scale platform for further growth in the UK and Europe.

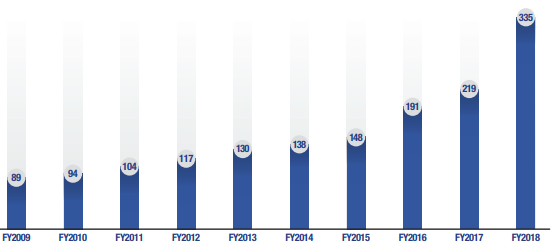

During FY18, the company generated revenue amounting to $1,198 million, up 54% on the prior year. Operating EBITDA for the year stood at $335.3 million, depicting an increase of 53% on the prior year. From the period starting FY2009 to FY2018, operating EBITDA for the company has been trending upwards from $89 million in FY2009 to $335 million in FY2018. Operating NPATA amounted to $206.7 million, up 67% on the prior corresponding period. The company’s performance during the year reflected a continued commitment to client relationships and disciplined execution of its strategy.

Looking at the performance over the period FY15 to FY18, the company witnessed 26.8% top-line CAGR growth with FY15 revenue amounting to $588.34 million and FY18 revenue amounting to $1,198.42 million. The company witnessed a bottom-line CAGR growth of 251.2% over the same period, with FY15 profit amounting to $3.31 million and FY18 profit amounting to $143.23 million.

Going forward, strategic initiatives supporting the business performance, international expansion with enhanced business on domestic front, strong balance sheet, recent acquisition, stable FY19 guidance, etc, will allow the company to explore further opportunities and excel in the business.

Operating EBITDA Trend (FY2009-18; $Mn) (Source: Company Reports)

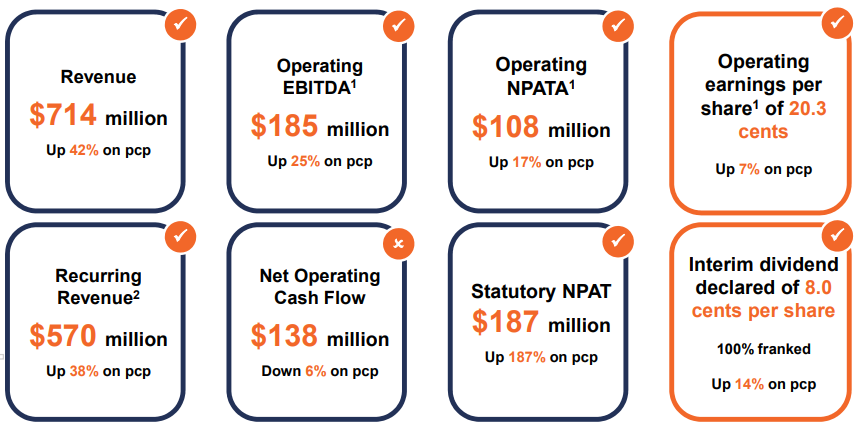

1HFY19 Highlights: During the six months ended 31 December 2018, the company generated revenue amounting to $714.4 million, up 42% on the prior corresponding period. Recurring revenue for the period amounted to $570.5 million, representing 80% of the total revenue. Statutory net profit after tax amounted to $186.8 million, up 187% on the prior corresponding period. Operating EBITDA for the period stood at $185.4 million, up 25% on pcp. Operating earnings per share during the period stood at 20.3 cents, up 7% on pcp. Based on the performance, the company declared a fully franked interim dividend of 8.0 cents per share, up 14% on the prior corresponding period.

1HFY19 Financial Performance (Source: Company Reports)

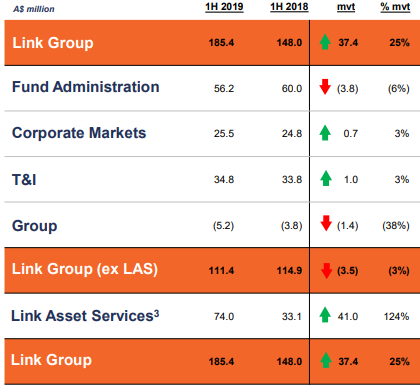

Segment Performance: Revenue from Fund Administration services amounted to $275.9 million, down 3% on pcp. Operating EBITDA for the segment went down by 6% at $56.2 million. Corporate Markets revenue was up by 13% to $116.5 million in 1HFY19, with growth attributed to domestic and international business wins. Operating EBITDA margin for the segment went down from 24% in pcp to 22% as a result of the competitive pricing environment across a number of jurisdictions. Technology & Innovation revenue amounted to $130.2 million, up 12% on pcp and Operating EBITDA amounted to $34.8 million, up 3% on pcp. Revenue from Link Asset Services (LAS) business stood at $309.3 million while operating EBITDA came in at $74.0 Mn in 1HFY19.

Segment-Wise Operating EBITDA (Source: Company Reports)

Acquisition of PEXA: During 1HFY19, the company acquired Property Exchange of Australia (PEXA), with its consortium partners, Commonwealth Bank of Australia and Morgan Stanley Infrastructure. The investment has a fair value of $715 million. Through the transaction, the company increased its equity in PEXA to 44.2%. The increased stake has provided the company with a new dimension for growth as a result of increase in volume and industry benefits from PEXA’s technology.

Growth Strategy: The company’s growth strategy is focused on five major driving factors, i.e., (a) The company enhanced its client relationships through continuous investment in technology, process improvement, and delivery of service excellence; (b) The second driving force includes innovation in the products and services provided; (c) The company also identifies client, product, and regional expansions as key drivers for growth, which is evident in the acquisition of LAS in November 2018. The company launched a share registry business in Hong Kong and has also signed an acquisition agreement with TSR Darashaw, a share registry business in Mumbai, India. The completion of the deal is expected in 2H2019; (d) Integration and efficiency benefits through synergies and other business optimisation opportunities also acted as catalysts for growth; and (e) Adjacent market opportunities in the form of increased equity holding on PEXA and sale of CPCS also supported the growth strategy.

Recent Updates:

1. Shareholder update: In a recent announcement to the exchange, it was notified that Challenger Limited ceased to be a substantial shareholder of the company, since 15 July 2019. However, National Australia Bank Limited and its associated bodies have become a substantial shareholder of the company with the voting power of 5.015%, since 22 July 2019.

2. Business Sale: In the month of June, the company completed the sale of the Corporate & Private Clients business, which was a part of the Link Asset Services division. The business has been sold to Apex Group Limited for a cash-free, debt-free consideration of €240 million. The company will utilise the net cash proceeds from the sale to reduce its debt that will provide a stronger and more flexible balance sheet.

3. Contract Extension: In another announcement in the month of June, the company updated on the extension to its contract for AustralianSuper for further 4 years, that includes the provision of superannuation administration and customer engagement activities to AustralianSuper.

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form around 44.19% of the total shareholding. AustralianSuper holds the maximum interest in the company at 7.24%, followed by Macquarie Investment Management Ltd at 5.24%.

Top 10 Shareholders (Source: Thomson Reuters)

Key Metrics: During the six months ended 31 December 2018, the company had a net margin of 26.1% as compared to the net margin of 12.9% in 1HFY18. The net margin was also higher than the industry median of 23.2%. Further, the company is generating better returns for its shareholders than its peers as it reported an ROE of 9.4% above the industry median of 7.7%.

.png)

Key Metrics (Source: Thomson Reuters)

Factors Affecting the Business Performance in 2HFY19: While the company expects its Technology and Innovation & PEXA businesses to deliver results in line with expectations, it may face certain challenges with respect to the remaining divisions. Due to the competitive pricing environment across a number of jurisdictions, the Corporate Markets division witnessed a decline in Operating EBITDA margin. ANZ and EMEA regions were characterised by lower than expected levels of capital markets related activity in the second half. Under LAS, the company saw the operating performance of its European operations, impacted due to lack of finality regarding the Brexit outcome in the UK. The Fund Administration division was impacted by the Treasury Laws Amendment (Protecting Your Super Package) Act 2019 (PYS Legislation). The principal impact of the legislation is expected to be seen in FY2020.

FY19 Guidance: For the year ended 30 June 2019, the company expects to report Operating EBITDA in the range of $350 million - $360 million as compared to $335.3 million in FY18, showing a decent rise in the range of 4.4% to 7.4% on Y-o-Y basis. Operating NPATA for the year is expected to be in the range of $195 million - $205 million against $206.7 million in the prior year.

Outlook: The company is well represented in a number of European jurisdictions with business focused on supporting clients and is well-positioned to perform under a range of Brexit scenarios. The company strengthened its operational presence in the property industry through the acquisition of PEXA. Moreover, it can now focus on its core competencies following the sale of Corporate & Private Clients business (CPCS). Overall, the company’s business fundamentals represent further growth prospects.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology:

Method 1: Price to Earnings Approach:

.png)

Price to Earnings based Valuation (Source: Thomson Reuters)

Method 2: EV/Sales Multiple Approach (NTM):

.png)

EV/Sales Based Valuation (Source: Thomson Reuters)

Stock Recommendation: The stock of the company generated negative returns of 5.38% and 33.59% over a period of 1 month and 3 months, respectively. During FY18, the company’s performance exceeded in comparison to the previous years across key financial measures with Operating EBITDA increasing by 53% and Operating NPATA increasing by 68%. FY18 was also marked by the expansion of the company’s global presence through the acquisition of Link Asset Services. Through the acquisition, the company expanded its footprints in the UK and Europe. The acquisition was strongly aligned with the company’s growth strategy and offered natural expansion into key markets. Operating EBITDA and Operating NPATA during 1HFY19 benefitted from the inclusion of LAS. The acquisition of PEXA during the first half has provided exposure to another attractive growth opportunity. The period was also characterised by a strong balance sheet that will help in exploring further growth opportunities. As a scaled provider across multiple markets and jurisdictions with a demonstrated capacity to evolve and innovate, the company remains well placed for further growth.

Considering the decent performance in FY18 and 1HFY19, the expected benefits out of synergies from LAS acquisition, growth opportunities through acquisition of PEXA and continued global expansion, we have valued the stock using two relative valuation methods, PE and EV/Sales multiple and have arrived at the target price of the stock in the range of $5.42 to $5.96 ( high single-digit to low double-digit upside (%)). Hence, we recommend a “Buy” rating on the stock at the current market price of $5.030, down 1.373% on 26 July 2019.

.png)

LNK Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...