Kalkine has a fully transformed New Avatar.

Company Overview: Link Administration Holdings Limited is a technology-enabled provider of outsourced administration services for superannuation fund administration, corporate markets and related value added services, including data management analytics, digital communication and stake-holder education and advice. Its segments include Fund Administration, which provides administration services to superannuation funds; Corporate Markets, which provides an integrated corporate market offering that connects issuers with their stakeholders and offers services, including shareholder management and analytics, stakeholder engagement and company secretarial, and Information, Digital and Data Services, which provides core services of development and maintenance of information technology (IT) systems and platforms, and value-added services of data analytics, digital solutions and digital communications. It provides platform solution to its clients, covering front, middle and back office administration functions.

.png)

LNK Details

New Client Renewals to Aid Future Growth: Link Administration Holdings Limited (ASX: LNK) is primarily engaged in the provision of technology-related administration, securities registration and asset services for listed and unlisted corporate entities, and superannuation funds across the globe. In addition, the company also provides ancillary services in the areas of digital communication, data integration and insights, and stakeholder education and advice. The company employs over 6,500 employees globally, serving a client base of more than 6,000.

In FY19, the company reported revenue amounting to $1,403 million, posting a growth of 17% on yoy. The highest growth was seen in the link asset services’ business with an uplift of 37% on prior corresponding period. Link Asset Services was followed by revenue growth of 33%, derived from Retirement & Superannuation Solutions. Technology & Innovation business and Corporate Markets business reported revenue growth of 16% and 14%, respectively. While all the key metrics reported decent growth over prior corresponding period, statutory NPAT grew at a whopping rate of 123%. During the year, the company renewed the Executive Leadership Team and made several key external appointments in Human Resources & Brand, Risk & Compliance and Retirement & Superannuation Solutions. In addition, the period was also marked by internal promotions in other executive roles. The above initiatives strengthened the business to seek growth opportunities and respond to the changing economic and political environments. Over the period covering FY15 to FY19, the company witnessed a top-line CAGR growth of 24.3% with FY15 and FY19 revenue amounting to $588.34 million and $1,403.47 million, respectively. The company’s bottom-line witnessed a CAGR growth of 213.6%, with FY15 and FY19 profit amounting to $3.31 million and $320.22 million, respectively.

Going forward, the company expects to benefit over the medium to long-term with the foundations laid in FY19. In FY20, operating EBITDA of the continuing business is expected to be stronger in the second half. Overall, operating EBITDA is expected to be broadly in-line with FY19. On a long-term perspective, global transformation is expected to deliver annualised savings of $50 million by the end of FY2022.

.png)

Revenue (Source: Company Reports)

Financial Highlights for the Year Ended 30 June 2019: During the year, the company reported revenue amounting to $1,403.5 million, up 17% on prior corresponding period revenue of $1,198.4 million. Operating EBITDA for the period stood at $356 million, up 6% on prior corresponding period value of $335.3 million. NPAT for the year was reported at $320.2 million, up 123% in comparison to $143.6 million in prior corresponding year. Recurring revenue for the year was reported at $1,123 million, up 18% on pcp. During the year, the company generated net operating cash flow amounting to $339 million, representing an increase of 6% in prior corresponding year. A fully franked final dividend of 12.5 cents was also declared, taking full-year dividend to 20.5 cents per share. Operating NPATA for the year was in-line with the revised guidance issued, going down at a rate of 3% on pcp. Despite significant regulatory and market uncertainty, the business stood strong during the year.

.png)

Key Financial Metrics (Source: Company Reports)

Keeping aside the impact of external factors on the operating performance, the period was marked by the successful implementation of various strategic initiatives including, contracts renewals with two large clients, Rest and AistralianSuper, increased stake in PEXA at 44.2% and divestment of Corporate & Private Client Services for a cash consideration of £240 million. The above initiatives represent an important milestone in setting the foundation for future growth.

Key Business Highlights:

Retirement & Superannuation Solutions: Revenue for the segment was reported at $550.8 million, which was marginally lower than FY18 revenue. While the company lost clients in the segment, the negative impact was partially offset by strong underlying number growth and improved fee for service within the division. Going forward, the company is confident on capitalising on future opportunities in the segment with underlying business drivers remaining strong.

Corporate Markets: Revenue for the corporate markets stood at $223.9 million, up 4.2% on pcp revenue of $214.8 million. Recurring revenue for the division increased by approximately 81% mainly due to new client wins, consolidation of the investor relations business in the UK, and acquisition of Sharex, and TSR Darashaw in India.

Technology & Innovation: The segment reported revenue growth of 12.2% at $258.8 million. Operating EBITDA increased at a rate of 9.0% in pcp. External revenue witnessed a rise of 21%, mainly due to expanded portfolio of digital products and services, higher volumes from new clients and larger volumes for communication services from insourcing of activity under a broader efficiency program.

Link Asset Services (LAS): Revenue increased by 3.8% on a pro-forma basis. Growth in revenue was driven by new business conversion, continued expansion in Europe and Ireland, and the flow of on-boarding benefits from recent client wins. The segment continued to provide strong recurring revenue growth and reported no client losses in 2H2019.

Going forward, the company is looking to improve its efficiency to cope up with short-term challenges. In the second half of FY19, the company witnessed an improvement in operating cash flow. Contract renewals, investment in PEXA and divestment initiatives during the year, together enhanced the balance sheet flexibility, laying the foundations for growth over the medium to long-term.

Recent Updates:

Change in Directors’ Interest: (a) The company recently announced that Glen Boreham, one of the directors on the Board, acquired 2,246 fully paid ordinary shares for a total consideration of $12,622.52. Another director name Peeyush Gupta, acquired 998 ordinary shares for a total consideration of $5,608.76. Anne McDonald and Fiona Trafford-Walker acquired 327 and 666 ordinary shares, for a total consideration of $1,837.74 and $3,742.92, respectively. The securities were issued under Link Group’s Dividend Reinvestment Plan. (b) Notice of AGM: As per a recent release, the company updated that the 2019 Annual General Meeting will be held on 15 November 2019.

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form around 38.79% of the total shareholding. AustralianSuper is the entity, holding maximum shares in the company at 7.24%. Pinnacle Investment Management Group Ltd is the second largest shareholder, representing a holding of 5.15% in the company.

.png)

Top Ten Shareholders (Source: Thomson Reuters)

Key Metrics: During the year ended 30 June 2019, the company had a gross margin of 92.2% which is higher than the industry median of 76.2%. The margin stood slightly below in comparison to the prior corresponding year gross margin of 92.6%. Net margin for the year was reported at 22.8%, which was higher than both the industry median and prior corresponding period margin of 17.8% and 12.0%. Moreover, the margin has seen a continuous upward movement over a period of 3 years, covering 2017 to 2019. Current ratio for the year stood at 1.38x as compared to prior corresponding year ratio of 1.22x, implying an improved position to meet the short-term obligations of the business.

.png)

Key Metrics (Source: Thomson Reuters)

What to Expect: Although, FY19 was a period of several challenges for the company, reflecting various headwinds in the form of uncertainty due to Brexit, client losses and competitive pricing pressures, the company is positive about growth over the medium term on the back of renewal of key contracts. Operating EBITDA of the continuing business i.e., excluding the impact of Corporate & Private Client Services (CPCS) and Link Market Services (LMS) South Africa, is expected to be broadly in-line with FY19. FY20 revenue for Retirement & Superannuation Solutions is expected to be in the range of $480 million - $500 million. Operating EBITDA for the business is expected to be between $60 million and $70 million. The company believes that the underlying business drivers for the business are strong and confides in medium-term growth potential through local and global opportunities. On a firm-wide perspective, the company is focusing on driving efficiency through cost and margin control to cope up with challenges in the economic environment.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies

Method 1: Price to Earnings Approach

.png)

Price to Earnings based Valuation (Source: Thomson Reuters)

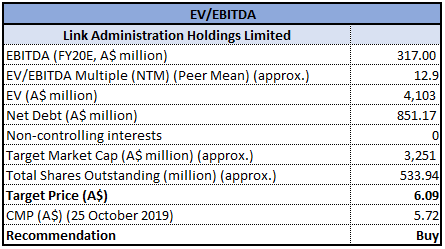

Method 2: EV/EBITDA Multiple Approach (NTM)

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The stock of the company generated returns of 1.24% and 13.07% over a period of 1 month and 3 months, respectively. In FY19, the company depicted strong resilience in the face of several external challenges and reported decent growth across key metrics. The period was marked by an improvement in operating margin and net margin, implying a decent financial position. Current ratio for the period also improved in comparison to pcp. In FY20, the company will be focused on cost and margin control to drive efficiency and sees good growth potential over the medium-term on the back of renewal of key contracts. The company believes that significant client renewals in the Retirement & Superannuation Solutions business together with an improved operating cash flow in 2H2019, will define the path for future growth. Considering the above factors, we have valued the stock using two relative valuation methods, Price to Earnings and EV/EBITDA multiples and have arrived at the target price of the stock in the range of $6.09 to $6.04 (high single-digit to low double-digit upside (%)). Hence, we recommend a “Buy” rating on the stock at the current market price of $5.720, up 0.175% on 25 October 2019.

LNK Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...