Kalkine has a fully transformed New Avatar.

Company Overview: Link Administration Holdings Limited is a technology-enabled provider of outsourced administration services for superannuation fund administration, corporate markets and related value added services, including data management analytics, digital communication and stake-holder education and advice. Its segments include Fund Administration, which provides administration services to superannuation funds; Corporate Markets, which provides an integrated corporate market offering that connects issuers with their stakeholders and offers services, including shareholder management and analytics, stakeholder engagement and company secretarial, and Information, Digital and Data Services, which provides core services of development and maintenance of information technology (IT) systems and platforms, and value-added services of data analytics, digital solutions and digital communications. It provides platform solution to its clients, covering front, middle and back office administration functions.

.png)

LNK Details

Strategic Investments, New client wins & Restructuring to Aid Growth: Link Administration Holdings Limited (ASX: LNK) provides technology-enabled administration, securities registration, and asset services. Besides, the company also provides value-added services in the areas of digital communication, data integration and insights, and stakeholder education and advice. The company has taken important measures to become a leading worldwide organisation. In doing so, it recently realigned its business structure to enhance and support service delivery for clients all over the world. Beginning from FY2020, Link Administration Holdings’ business will consist of five global segments, including Retirement & Superannuation Solutions, Corporate Markets, Fund Solutions, Banking & Credit Management and Technology & Operations.

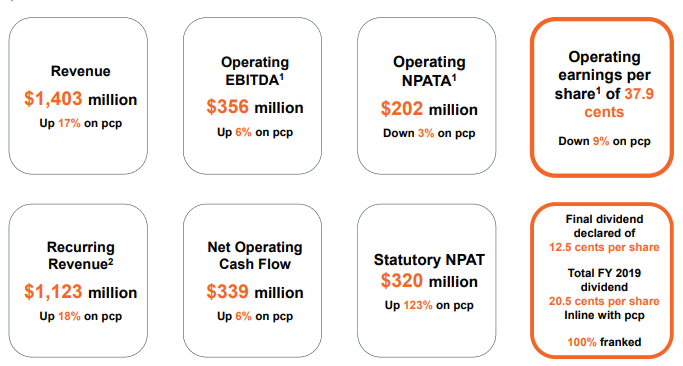

For the year ended 30 June 2019, the company reported revenue of $1,403 million, up 17% year over year. Operating EBITDA for the year stood at $356 million, up around 6% year over year. In FY19, operating NPATA came in at $202 million, down 3% on a yearly basis. Operating earnings per share for the period stood at 37.9 cents per share, down 9% year over year. The company declared a final dividend of 12.5 cents per share in FY19.

For FY20, the company anticipates operating EBITDA from continuing operations to be stronger in the second half of the year and in-line with FY19. The company also stated that the Global transformation program is on track, and the company expects to save ~$50 million of annual cost towards the end of FY2022.

The company witnessed a compound annual growth rate of ~24.3% in revenue over the period covering FY15-FY19. Over the same time period, the company’s operating EBITDA witnessed a CAGR of ~24.5%. Robust underlying member growth in Retirement & Superannuation Solutions (RSS) and expansion into newer markets like Italy, India, the Netherlands, Hong Kong, and Luxembourg, has supported the growth of the company. Moreover, continued investment in key technology platforms to deliver better end-user experience and operational competences is a key catalyst for the future.

.png)

Revenue & EBITDA (Source: Company Reports)

Key Financial Takeaways from FY19 Period Ended 30 June 2019: In FY19, the company reported revenue of $1,403 million, increasing 17% year over year. Operating EBITDA for the period went up 6% year over year and came in at $356 million. Statutory NPAT for the period increased by 123% and came in at $320 million. Operating NPATA for the year went down by 3% and came in at $202 million. Operating earnings per share in FY19 were 37.9 cents per share, down 9% year over year. Basic earnings per share for the year came in at 59.98 cents per share, up 110% on pcp. Recurring revenue increased by 18% in FY19 and came in at $1,123 million. The company declared a fully franked final dividend of 12.5 cents in FY19, bringing full-year dividends to 20.5 cents per share.

FY19 Financial Highlights (Source: Company Reports)

Retirement & Superannuation Solutions (formerly Fund Administration): Total revenue from this segment decreased marginally and came in at $550.8 million. The company witnessed client losses during the period which was partially offset by growth from underlying members and contracted price escalators. An increase in non-recurring revenue during the year was aided by a few huge regulatory projects.

Link Asset Services (LAS): Revenue rose by 3.8% on a year over year basis and came in at $607.6 million. The year over year increase was primarily due to new business, advantages from onboarding recent wins, coupled with extended operations into Europe. Operating EBITDA increased marginally i.e. 0.5% year over year and came in at $131.4 million.

Corporate Markets: The company reported revenue of $223.9 million, which increased 4.2% on a year over year basis. The increase was driven by an 81% rise in recurring revenue and $1.1 million growth in non-recurring revenue. New client wins, the positive impact of Sharex, TSR purchases in India, and the merging of the IR business in the UK are key positives.

Technology & Innovation: The segment reported revenue of $258.8 million, up 12.2% year over year, indicating solid growth in both internal and external revenue. Operating EBITDA increased 9% year over year and came in at $79.4 million. External revenue grew 21%, mainly due to higher volumes for communications services and new client wins.

Balance Sheet Position: At the end of the year, the company reported cash and cash equivalents of $560.2 million. The company’s net debt at the end of the year came in at $593.4 million. The company’s net debt increased primarily on account of higher PEXA investment completed in January 2019, divestment of CPCS in 2019 along with few other investments in Leveris, TSR Darashaw, etc.

Cash Flow Position: Operating cash inflow in FY19 came in at $339 million as compared to $320.3 million in FY18. Net cash provided by operating activities after tax and interest, came in at $196.6 million, down 6% year over year. Capital expenditure for the period came in at $80.7 million. Net operating free cash flow in FY19 stood at $258.4 million as compared to $254 million in FY18.

Despite recent client losses in FY19 and continued competitive pricing pressures in corporate markets, the company remains positive about its expanded operations in Hong Kong, India, Italy, the Netherlands, and Luxembourg. Moreover, the company is looking forward to drive growth from the increased investment in PEXA, exploring newer avenues in the UK pensions market and is well-positioned to take advantage of super fund consolidation in Australia. It is to be noted that, a healthy balance sheet will allow the company to make future accretive acquisitions.

Recent Updates:

(a) Change in Directors’ Interest: The company recently announced that John McMurtrie, one of the directors on the Board, acquired 269,009 Performance Share Rights (PSPs).

(b) On 9 December 2019, the company announced that it has bought back 3,122,175 shares for a total consideration of ~$1,74,43,594.98 via on-market, according to its daily share buy-back notice.

(c) The company issued an announcement stating that Perpetual Limited and its related bodies corporate, increased its voting power from 7.69% to 8.74%.

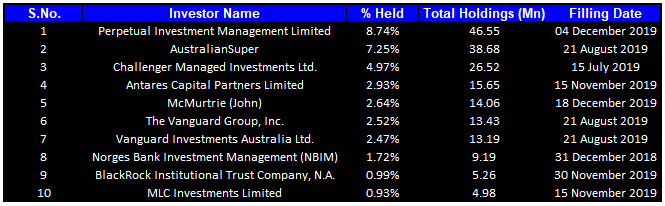

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together forms around 35.17% of the total shareholding. Perpetual Investment Management Limited is the entity holding maximum shares in the company at 8.74%. AustralianSuper is the second-largest shareholder, representing a holding of 7.25% in the company.

Top Ten Shareholders (Source: Thomson Reuters)

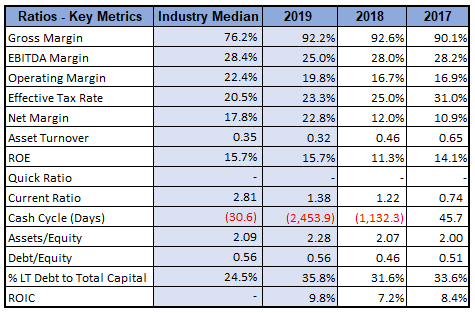

Key Metrics: In FY19, the company had a gross margin of 92.2%, which was higher than the industry margin of 76.2%.The margin, however, stood slightly below in comparison to the previous corresponding year’s gross margin of 92.6%. Net margin for the year stood at 22.8%, higher than both the industry median of 17.8% and from the previous corresponding period margin of 12.0%. Debt-to-equity ratio for the year stood at a decent level of 0.56x, reflecting the funds raised for acquisition.

Key Metrics (Source: Thomson Reuters)

Outlook: The company is positive to drive growth from the expanded investment in PEXA, discovering newer avenues in the UK pensions market and is positioned well to ride on super fund consolidation in Australia. The company is also optimistic about future growth prospects on the back of contract renewal. For FY2020, the company expects operating EBITDA from the continuing operations, which excludes Corporate & Private Client Services (CPCS) and Link Market Services (LMS) South Africa, to be sharper in the second half of the year. Overall, it expects full-year operating EBITDA to be in-line with the previous year. The company further expects progress in other businesses to offset a softer impact from Retirement & Superannuation Solutions (RSS). For FY2020, the company expects RSS revenue to be in the range of $480 million-$500 million and operating EBITDA in the range of $60 million-$70 million. The company expects transformation on a global basis to deliver $50 million of annualised savings by the end of FY2022. The company believes that continuous focus on client retention, higher investment in new products and existing product innovation will drive growth in the coming future.

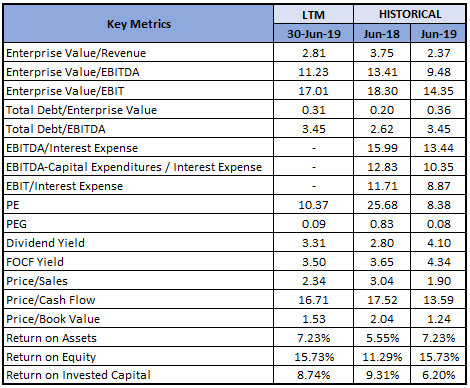

Key Valuation Metrics (Source: Thomson Reuters)

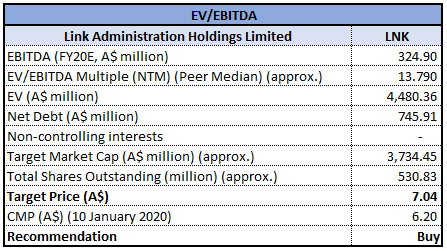

Valuation Methodology: EV/EBITDA Multiple Approach

Enterprise Value to EBITDA Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company generated returns of 11.13% and 21.61% over a period of 3 months and 6 months, respectively. In FY19, the company delivered a stellar result, driven by positive contribution from all segments and expects to thrive further growth on the back of expansion into newer markets and enhanced focus on new products. From the analysis standpoint, the company has recorded revenue CAGR of 24.3% over the last four years. The company deems that substantial client renewals in the Retirement & Superannuation Solutions business together with the realignment of its business structure will add future growth, depth, and global experience and will help the company to withstand external challenges. Considering the above factors, we have valued the stock using a relative valuation method, i.e. EV/EBITDA multiple, and arrived at a target price of lower double-digit upside (in % terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $6.200, up 0.162% on 10 January 2020.

LNK Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...