Kalkine has a fully transformed New Avatar.

Company Overview: MACA Limited (ASX: MLD) is an integrated services contractor specialized in providing services related to mining, crushing, civil construction, infrastructure and mineral processing equipment. Its mining services and civil construction business provides open pit contracting services to the mining industry, including loading and hauling, drilling and blasting, crushing and screening and civil infrastructure services to public and private industry. The company performs Civil bulk earthworks for the private / resource sector including mining, TSF, road, borefield and camp infrastructure. With modern, well-maintained equipment and extensive knowledge of the latest technologies, the company effectively and efficiently covers all aspects of its services.

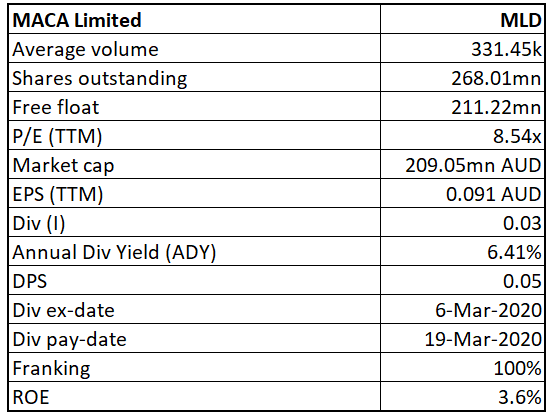

MLD Details

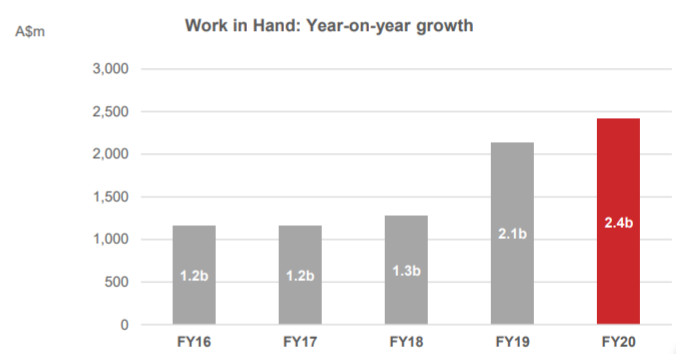

Strong Work-in Hand Position: MACA Limited (ASX: MLD) is an integrated services contractor specialized in the provision of contract mining services, civil contracting services and mineral processing services throughout Australia. MLD also provides contract mining services in Brazil, South America. The company remains focused on productivity and other initiatives to improve and protect margins to bolster earnings sustainability. It is also focused on delivering for its existing clients while winning new work and diversifying into new markets, services and commodities. Over the last four years, the company’s work in hand position has significantly improved, rising from $1.2 billion in FY16 to $2.4 billion in FY20. Over the same period, the company’s revenue has increased at a CAGR of 15.74%, rising from $429.1 million in FY16 to $665.3 million in FY19.

Work in Hand in Last Five Years (Source: Company Reports)

Moving forward, the company expects to deliver continued growth in both its revenue and earnings. During the last financial year, the company continued the expansion of its Civil Construction & Infrastructure division and expects this to be continued in FY20 as well, underpinned by recent contract awards in WA and Victoria. MLD maintains a positive outlook for FY20, supported by a strong work in hand position, favourable market conditions and a strong pipeline of opportunities with existing and new clients.

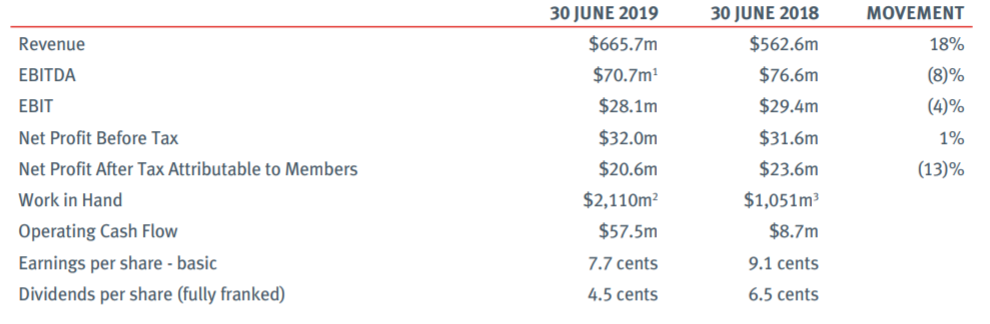

FY19 Performance Highlights: In the financial year 2019 or FY19, the company’s results were in-line with guidance, with revenue of $666 million, EBITDA of $70.7 million and NPAT attributable to members of $20.6 million. The Mining and Crushing division reported a revenue of $473 million, representing 71% of the total revenue. For the full year, the company paid total dividends of 4.5 cents per share fully franked.

Over the year, the company’s Australian mining operations witnessed significant growth, with the renewal of a long-term contract with Regis Resources at the Duketon South operations, the commencement of the Bluff Coal project for Carabella Resources in Queensland, and the award of three crushing contracts by BHP Iron Ore. During the year, the company made a significant investment of $121 million in mining business to deliver additional profitability and efficiency on both new and existing projects.

FY19 was a strong year for MACA Interquip (MACA 60% owned), as it commenced the Kirkalocka gold project for Adaman Resources during the year and completed the construction of crushing plants for MACA Mining at BHP and a secondary mill upgrade for AngloGold Ashanti at the Tropicana project.

The company ended FY19 in a strong financial position with a net debt position of $82.8 million representing a gearing ratio of 20% and with cash on hand of $59.3 million.

FY19 Results Summary (Source: Company Reports)

H1FY20 Performance Summary: In the first half of FY20, the company reported net profit after tax of $12.0 million, up 48% on pcp, and revenue of $364 million, up 12% on pcp. The company’s EBITDA for H1FY20 stood at $54.4 million, up 97% on pcp, in line with FY20 EBITDA guidance of $104 to $110 million. For the half-year period, the company declared a dividend of 2.5 cents per share, up 25% on pcp.

One of the major highlights of the period was the five-year mining contract award in November 2019 from FQM Australia Nickel Pty Ltd at the Ravensthorpe Nickel Project. This contract is expected to generate around $480 million in revenue over the initial five-year term and will diversify MLD’s client base and commodity exposure. At its Crushing divisions, the company continued its operations at a number of BHP’s sites, including Mining Area C and Eastern Ridge. During the period, MACA Interquip completed mill installation for Adaman Resources at Kirkalocka Gold Project for revenue of around $30 million.

Half-Year Result Snapshot (Source: Company Reports)

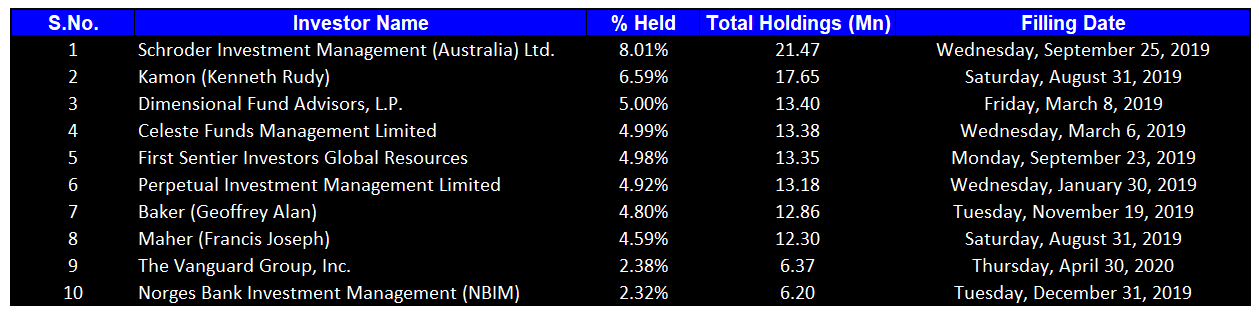

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 48.57% of the total shareholding. Schroder Investment Management (Australia) Ltd. and Kamon (Kenneth Rudy) hold maximum interest in the company at 8.01% and 6.59%, respectively.

Top 10 Shareholders (Source: Refinitiv, Thomson Reuters)

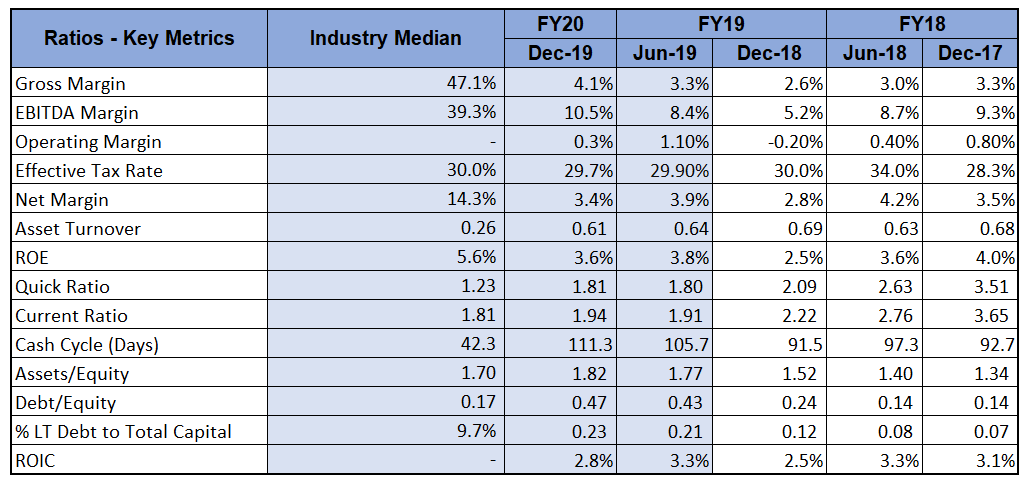

A Quick Look at Key Margin: In FY19, the company’s profitability margins have improved significantly. The gross margin has increased from 2.6% in H1FY19 to 4.1% in H1FY20. Further, the net margin has increased from 2.8% in H1FY19 to 3.4% in H1FY20. The company has a current ratio of 1.91x, higher than the industry median of 1.81x, demonstrating that the company is well-equipped to pay its short-term obligations.

Key Valuation Metrics (Source: Refinitiv, Thomson Reuters)

Recent Contracts:

(a) Award of Corunna Downs Road Works: On 17 March 2020, the company announced that it has been awarded the “Public Road Upgrade and Access Road Works’ at the Corunna Downs Iron Ore Project for Atlas Iron Pty Ltd, demonstrating the civil capability within the company’s end to end mining service offering. This contract is expected to generate a revenue of $38 million over the 8-month term of the project.

(b) Execution of Mining Contract with Emerald Resources: On 13 March 2020, the company announced that it has executed a Mining Contract with a wholly-owned subsidiary of ASX-listed Emerald Resources Ltd (ASX: EMR), for provision of contract mining services at the Okvau Gold Project in Cambodia. This contract is expected to generate around US$230 million in revenue for MACA and will allow MACA to draw on overseas experience gained in Brazil and adds further to MACA’s work in the gold sector.

What to expect: The company is experiencing strong tendering activities and demand in the market for MACA’s services. The company is well placed to take advantage of numerous opportunities with both existing and new clients. Further, the significant capital investment made in FY19 is expected to deliver additional profitability and efficiency on both new and existing projects. The Civil and Infrastructure divisions are expected to deliver significant revenue growth in the second half of FY20, with improved operational delivery to contribute to profitability. The operating cashflow in the second half is expected to be stronger as client loan positions unwind. The company expects to see improvement in debtor management and balance sheet rationalization throughout FY20 and into FY21.

The company maintains a positive outlook for FY20, supported by a strong work in hand position, favourable market conditions and a strong pipeline of opportunities with existing and new clients. The outlook is also supported by a general improvement in the mining and construction industries. In FY20, the company expects its revenue to be around $770 million and anticipates EBITDA to be in the range of $104 - $110 million.

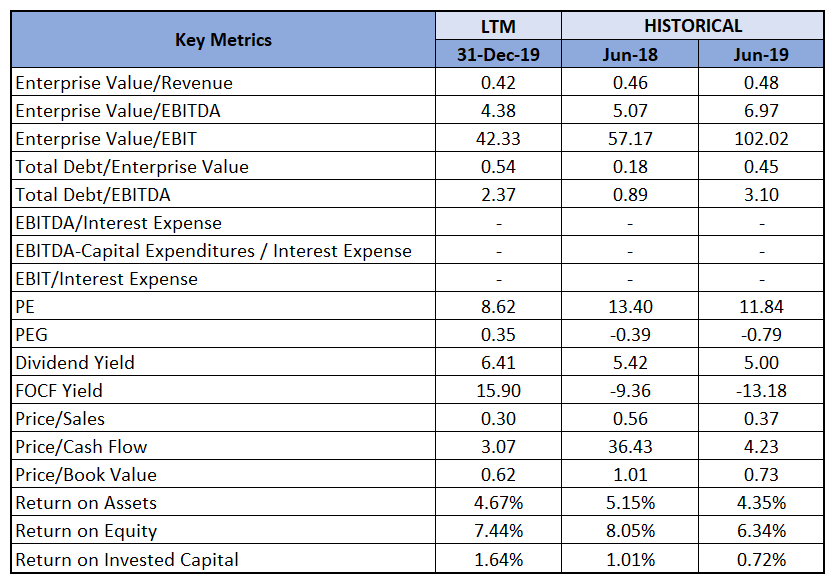

Key Valuation Metrics (Source: Refinitiv, Thomson Reuters)

Valuation Methodology: P/E Multiple Based Relative Valuation (Illustrative)

P/E Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: In the past six months, the stock of MLD declined by 22.7% on ASX, and is currently trading lower than the average of its 52-week trading range of $0.487 - $1.20. With a strong Work-in hand position ($2.4 billion in February 2020) and near-term tendered opportunities, the company expects to continue to grow in the coming years. We have valued the stock using a Price to Earnings multiple based illustrative relative valuation method and have arrived at a target price with lower double-digit upside (in % terms). For the purpose, we have taken peers like Perenti Global Ltd (ASX: PRN), Macmahon Holdings Ltd (ASX: MAH) and NRW Holdings Ltd (ASX: NWH). Considering the company’s strong work in hand position, favourable market conditions, strong pipeline of opportunities with existing and new clients, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $0.790, up by 1.282% on 20 May 2020.

MLD Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...