Kalkine has a fully transformed New Avatar.

Company Overview: Macmahon Holdings Limited (Macmahon) is principally engaged in the provision of contract mining services. The Company has three operating segments: Surface Mining, Underground Mining and International Mining, which are aggregated into the Mining segment. The Mining segment operates in two principal geographical areas, including Australia and Overseas. The Mining segment provides a range of mining services for surface and underground operations, from mine development to materials delivery, which include a range of engineering services, including design, construction and on site services to deliver on client needs from the design phase to completion. The Company offers various services, including surface mining; underground mining, and plant, maintenance and engineering. Macmahon's Mining Services business provides a range of services, including drilling, shotcreting, raise drilling, shaft sinking and engineering design to various projects.

.png)

MAH Details

MAH Declares First Dividend in Seven Years: Macmahon Holdings Limited (ASX: MAH) is involved in providing mining and consulting services to mining companies throughout Australia, Southeast Asia, and South Africa. The group generates revenue from the provision of mining services, civil construction and rehabilitation services to mining companies in Australia and Indonesia. Revenue for services is recognized on the basis of work completed over time and billed to customers as the services were delivered to customers. The amounts billed to customers are typically due within 30-60 days from invoice date. The transaction price for each contract is based on agreed contractual rates to which the Group is entitled and may include a variable pricing element which is accounted for in accordance with the policy on variable consideration. Other income includes management fees from the joint venture partners. Looking at the historical performance, bottom-line of the company posted a decent CAGR growth of 62.2% over the period of FY2016-2019. Going forward, the company expects revenue to record a Y-o-Y growth in the range of 8.8% to 17.9% in FY20. With this, we expect CAGR-Growth in revenue over the period FY16-FY20E to be in the range of 36.3% to 39.1%.

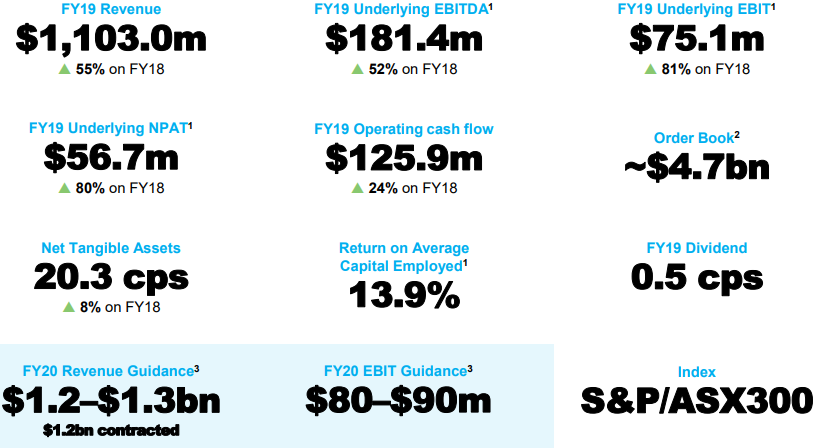

Consistent project execution has been a key focus for Macmahon and is driving a real transformation in Macmahon’s financial performance, with FY19 revenue more than tripled what it achieved in FY17 and earnings moved from negative to strongly positive in that period. This reliable performance and the good revenue visibility, along with order book worth of $4.7 Bn has underpinned the Board’s decision to reinstate dividends to Macmahon’s shareholders. The Board of Directors declared a final dividend of 0.5 cents per share, which is the company’s first dividend in seven years with the Management aiming to pay dividends on a sustainable basis going forward.

.png)

Financial Highlights (Source: Company Reports)

Decent FY19 Top-Line and Bottom-Line Performance: Revenue for the period increased by 55% to $1,103.0 Mn, as compared to $710.3 Mn in FY18, mainly due to increase in company’s activity across its contract mining projects in Australia and Indonesia. Underlying EBITDA increased by 52% to $181.4 Mn, while Underlying EBIT increased by 81% to $75.1 Mn. Underlying EPS for the period increased by 74% to 2.69 cps. Statutory Net Profit After Tax for the period was reported at $46.1 Mn, as compared to $33.2 Mn in the previous year. For FY19, the Board has approved the payment of a final dividend of 0.5 cents per share, partially franked to 30%, for which the record date will be 14 October 2019 and the payment will be made on 29 October 2019. Going forward, the company intends to pay dividends on a sustainable basis and the Board may also consider share buybacks as a means of returning cash and delivering value to shareholders.

.png)

FY19 Income Statement (Source: Company Reports)

Robust Balance Sheet with Cash on Hand of $113.2 Mn: Its operating cashflow (excluding interest, tax and settlement for the class action) for the period was reported at $125.9 Mn, as compared to $101.9 Mn in FY18, representing a conversion rate from underlying EBITDA of 69.4%.The cash flow conversion was impacted by an increase in working capital due to the delayed receipts from trade receivables of $24 Mn.

The company maintained a robust balance sheet in the year, with gearing of 10.5%, cash on hand of $113.2 Mn and net debt of $52.7 Mn as on June 30, 2019. After factoring in the delayed receipts from clients, net debt and gearing were reduced to $28.7 Mn and 6%, respectively.

.png)

FY19 Cash Flow Metrics (Source: Company Reports)

Other FY19 Important Achievements:During the period, the company joined the benchmark S&P/ASX300 index; settled a legacy class action relating to events in 2012; achieved record monthly volumes for its largest contracts including Batu Hijau, Byerwen and Tropicana; secured the new Boston Shaker underground contract at the Tropicana gold mine; and bolstered its underground division and announced the acquisition of GBF group.

Its safety performance improved over the year, with a Lost Time Injury Frequency Rate (LTIFR) of 0.36 from 0.46 in FY18, and a Total Recordable Injury Frequency Rate (TRIFR) of 3.98 against 6.28 in FY18.

.png)

FY19 Injury Frequency Rates Data (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 51.15% of the total shareholding. Perpetual Corporate Trust Ltd. and CPU Share Plans Pty. Ltd. hold maximum interest in the company at 44.27% and 3.05%, respectively.

.png)

Top 10 Shareholders (Source: Thomson Reuters)

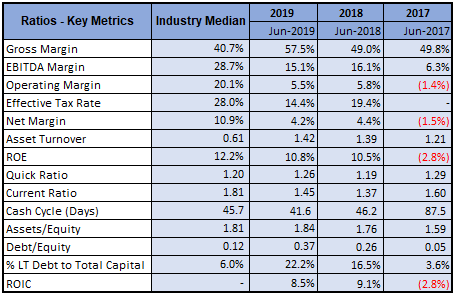

A Quick Look at Key Metrics: Its gross margin for FY19 stood at 57.5%, better than the industry median of 40.7%. Its quick ratio for FY19 stood at 1.26x, better than the industry median of 1.20x, indicating high liquidity for the company than its peer group. Its ROE has improved from 10.5% in FY18 to 10.8% in FY19.

Key Metrics (Source: Thomson Reuters)

Key Updates: On September 30, 2019, the company announced the appointment of two highly credentialed independent non-executive directors Mr Bruce Munro and Mr Hamish Tyrwhitt, effective from October 1, 2019. Both individuals have spent decades in the contracting industry in senior executive and director roles. They are expected to bring the benefit of their industry knowledge, experience and networks to the Macmahon Board. Their executive experience, managing large organisations with operations in Australia and Asia, together with Hamish’s public company experience in Australia, the UAE, and the UK, will be very useful to Macmahon in its endeavor to grow into an industry leading company.

On October 1, 2019, MAH’s Chief Executive Officer, Mr. Michael Finnegan, will join the Board as Managing Director. Mr. Finnegan has been serving MAH since 2014, and before joining MAH, he held senior operational management positions with other major mining contracting companies, both in Australia and across Asia.

On June 12, 2019, the company commenced facilitated negotiations with Newcrest Mining regarding pricing for changes to the mine plan and contract programme at the Telfer gold project. While these discussions did not initially reach a resolution, progress in recently renewed discussions between the parties has led Macmahon to form the view that an acceptable agreement for increased revenue is likely to be reached in the near future.

Key Risks: The company is susceptible to various risks such as changing industry and commodity cycles, failure to win new contracts, early contract termination and contract variations, project delivery risk, risks associated to margins, operations, safety, equipment and consumable availability, currency fluctuation, partner and control risk, country risk, financing risk, acquisition risk, etc.

What to expect: As per the Annual report, the company is well-positioned for growth in FY20 with secured work in hand of $1.2 Bn. It is expected that FY20 revenue and EBIT would be around $1.2-$1.3 Bn and $80-$90 Mn, respectively. Over the past twelve months, the company has positioned its business for growth, both organically and through the strategic acquisition of specialist underground contractor GBF Group. The growth can be supported by consistent execution on its secured work in hand and tender pipeline of more than $7 Bn in potential new revenue. This pipeline includes over $4.5 bn of projects where the company is the preferred or exclusive tenderer. Many of such opportunities are with existing clients placing the company in a competitive position. In FY20, company’s focus is expected to integrate the GBF business, continue to execute its order book safely and secure new work, whilst leveraging its collaborative end to end offering to benefit its clients, people and shareholders. These initiatives are supported by continued investments in innovation and technology, and improving the capacity of human resources through training, aimed to strengthen its service delivery and operating efficiency. These growth strategies are expected to enable the company to be a leading mining contractor that can service clients through the life cycle of their mining operations.

FY19 Financial Metrics & FY20 Guidance (Source: Company Reports)

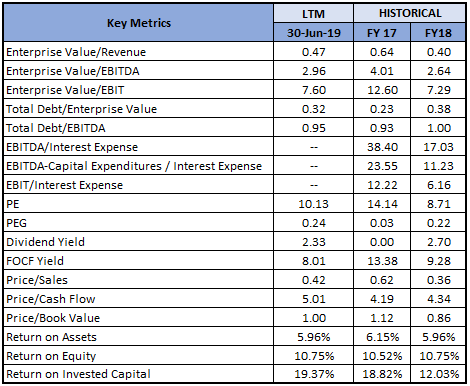

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology 1: Price to Earnings (PE) based Valuation

(11).png)

Price to Earnings (PE) based Valuation (Source: Thomson Reuters)

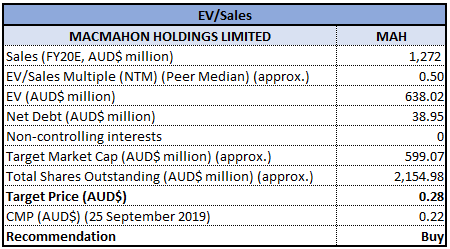

Valuation Methodology 2: Enterprise Value to Sales based Valuation

Enterprise Value to Sales based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The stock of the company generated a negative return of 8.89% in the span of six months, however, it posted a positive return of 20.59% over one-month period. Company’s top-line grew by 55% on previous year, its statutory NPAT grew by 38.86% on previous year. It held a decent cash balance of $113.2 Mn at the end of FY19. The acquisition of GBF, company’s $4.7 Bn order book and significant tender pipeline augur well for the company to deliver further earnings and cash flow growth in FY20. Looking at the business prospects over the long-term, we have valued the stock using two relative valuation methods, i.e., Price to Earnings multiple and Enterprise Value to Sales multiple and arrived at a target price of double-digit growth (in % term). Hence, we give a “Buy” recommendation on the stock at the current market price of A$0.220 per share, up 2.326% on 25 September 2019.

MAH Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...