Kalkine has a fully transformed New Avatar.

Company Overview: Metcash Limited is an Australia-based wholesaler and distributor, engaged in supplying and supporting independent retailers and other businesses across the food, grocery, liquor and hardware industries. The Company's segments include food, liquor and hardware. Food activities comprise the distribution of a range of products and services to independent supermarket and convenience retail outlets. Liquor activities comprise the distribution of liquor products to independent retail outlets and hotels. Hardware activities comprise the distribution of hardware products to independent retail outlets and the operations of Company owned retail stores. Its Independent Brands Australia (IBA) business operates national independent retail brands including Cellarbrations, The Bottle-O, IGA Liquor, Duncans, Thirsty Camel, Big Bargain and Porters. The Company has its operations in Australia and New Zealand.

.png)

MTS Details

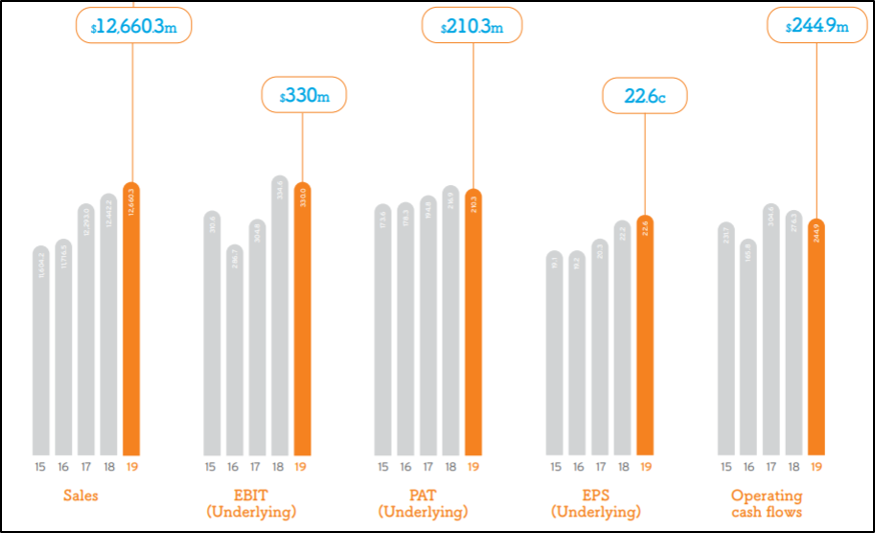

Stable Earnings and Strong Balance Sheet: Metcash Limited (ASX: MTS) is Australia’s leading wholesaler and distributor to independent retailers in the food, grocery, liquor, hardware and automotive industries. As on 24 February 2020, the market capitalisation of the company stood at ~$2.56 billion. In the Annual General Meeting, the management stated that the company delivered a decent set of financial results. During FY19, reported group sales witnessed an increase of 1.8% to $12.7 billion, and EBIT of the company stood at $330 million, with earnings growth in the Hardware and Liquor pillars offset by a decline in the Food pillar and higher corporate expenses. In the same time span, statutory profit after tax stood at $192.8 million, up from a loss of $148.2 million. During the year, the company bought back shares worth $150 million, which resulted in the earnings per share to increase by 1.8% to 22.6 cents. The company’s business pillars continued to generate solid cash flows along with the focus on working capital, which resulted in operating cash flows of $244.9 million. Despite the challenging market conditions, the company reported decent earnings and cash flows by all pillars and was well-positioned with a strong balance sheet. Owing to the decent financial performance, the Board determined to pay a final dividend of 7 cents per share, bringing total dividends for the year to 13.5 cents per share, representing an increase of 3.8% on the prior year. This represents a full year dividend payout ratio of 60% of underlying earnings per share.

Turning towards the company’s strategy, the group has clearly defined its five-year strategy- MFuture, which is delivering a pathway to sustainable growth. This strategy is a balanced-out approach for revenue growth and costs out. During the year, the company continued to invest in stores under the Diamond Store Accelerator (DSA) store upgrade program, bringing the total stores through the program to approximately 400 with average sales growth of roughly 10% from the newly added 79 stores. While the market was highly competitive, the company reported a continued increase in the sales trajectory through the first quarter of FY20.

In the upcoming years, the company will have a strong focus on cutting out costs under its MFuture program. It will also focus on increasing its revenue which includes major investments to improve the competitiveness of its Food, Liquor and Hardware retailer networks. Metcash Limited is supported by the confidence of retailers and their inclination to continue to invest in the company’s stores. .png)

FY19 Financial Highlights (Source: Company Reports)

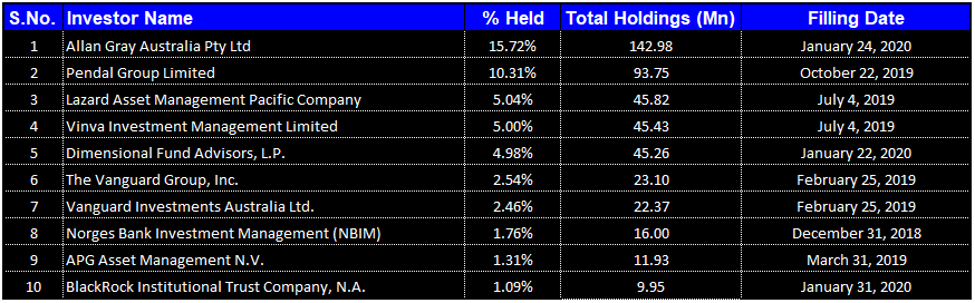

Details of Top 10 Shareholders: The following table provides an overview of the top 10 shareholders of Metcash Limited. Allan Gray Australia Pty Ltd. is the largest shareholder in the company, with a percentage holding of 15.72%.

Top 10 Shareholders (Source: Thomson Reuters)

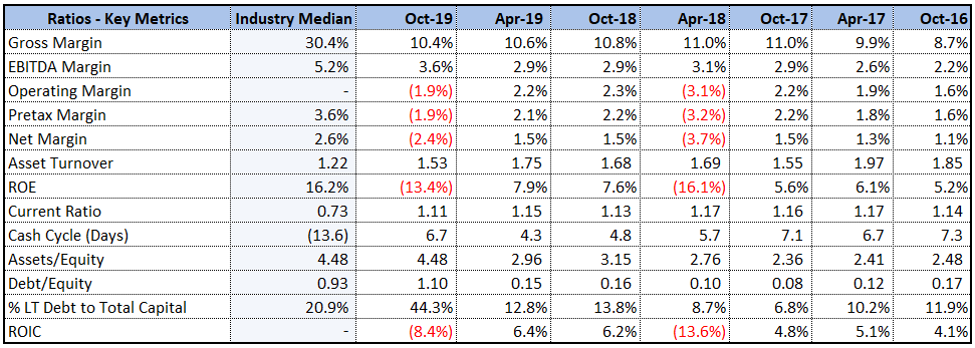

Sufficient Liquidity Levels and More Profitable Position: During 1H20, gross margin of the company was in line with 2H19 and stood at 10.4%. In the same time span, EBITDA margin of the company witnessed an improvement over the previous half and stood at 3.6%, up from 2.9% in 2H19. During 1H20, current ratio of the company stood at 1.11x, higher than the industry median of 0.73x. This indicates that the company is liquid enough to pay off its current liabilities using its current assets.

Key Margins (Source: Thomson Reuters)

Liquor delivered its Sixth Consecutive Year of Earnings Growth: The company has recently updated the market with the financial performance of 1H20, wherein it reported an increase of 1.6% in group revenue to $6.3 billion. In the same time span, group underlying EBIT of the company was $149.7 million and underlying profit after tax stood at $95.7 million. The company also reported a strong balance sheet with no debt maturities until FY21 and initial asset value of $936.8 million. During 1H20, the hardware pillar performed well in comparison to the previous period with growth and cost initiatives compensating for the negative impact of the slowdown in construction activity. The liquor business also reported a decent financial performance, delivering another period of earnings growth. In the same time span, operating cash flow of the company stood at $88.8 million, representing a cash realisation ratio of 52.4%. The Board has declared a fully franked interim dividend of 6.0 cents per share which was paid on 23 January 2020. The dividend represents a payout ratio of ~60% of underlying earnings per share.

Convenience business – 7-Eleven: The company has recently announced that 7-Eleven will not be renewing the current supply agreement as MTS was not able to reach its supply requirements for the east coast. MTS determined that these requirements would lead to supply being uneconomic for its Convenience business. Total convenience annual sales to 7-Eleven are approximately $800 million, which mainly comprise of tobacco sales with lower margins. The company has also announced that Annette Welsh has been appointed as the new CEO of the Hardware business with effect from 1 May 2020, owing to the retirement of Mark Laidlaw.

Analysis of Five-Year Performance: Over the span of five years from FY15 to FY19, the company witnessed a CAGR (compound annual growth rate) of 2.2% in sales revenue, up from $11.6 billion in FY15 to $12.6 billion in FY19. In the same time span, underlying profit after tax went up to $210.3 million from $173.6 million in FY15, representing a CAGR of 4.91%. This decent financial performance resulted in a decent increase in earnings per share to 22.6 cents from 19.1 cents in FY15. The dividend payout ratio also went up to 60% in FY19 from 34% in FY15.

Five-Year Performance (Source: Company Reports)

Metcash’s Business Model: MTS is Australia’s leading wholesaler and distributor, supplying approximately 5,000 independent retailers across the food, liquor and hardware domains. The company operates a low-cost distribution model, enabling retailers to maintain a stand against competitors. The group employs over 6,000 people and indirectly supports employment in the independent retail network. During 1H20, sales revenue of food and liquor witnessed a slight increase of 1.2% and 1.7% on the previous year and stood at $4,381.1 million and $1,784.2 million, respectively. This increase was, however, offset by the decline in sales revenue of hardware by 4.2% to $1,044.2 million. Metcash’s operations are designed to allow significant volumes to be distributed through its warehouse infrastructure at a relatively fixed cost and has several programs to derive sales and margins, including pricing and promotions, customer alignment etc.

Future Opportunities and Growth Expectations: The company has placed its focus on reducing the costs and expects to balance the effect of cost inflation over the remainder of FY20. Metcash Limited is anticipating market growth in liquor in the remaining year, which will be influenced by the ‘premiumisation’ trend of higher quality but lower consumption. The group is focused on its growth initiatives under the MFuture program with prospects in private and exclusive label. The company has announced that it has entered into a five-year supply agreement with Drakes Supermarkets in Queensland and is expecting to invest in growth initiatives through the MFuture program. The company also anticipates operating expenditure for FY20 to be in line with the expenditure in FY19. On the cost front, the company has identified initial savings of approximately $50 million over FY20 and FY21, backed by the MFuture strategy.

MTS expects that slowdown in construction activity will impact trade sales over the remainder of the year. However, the company has a strong focus on reducing the costs to help offset the effect of the slowdown in construction activity. The market fundamentals for hardware are likely to remain positive over the medium to longer term with expectations of increasing construction activity, boosted by population growth and an undersupply of housing..png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: Price to Cash Flow Based Relative Valuation.png)

Price to Cash Flow Based Relative Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of MTS gave a return of 10.59% on YTD basis and a return of 6.42% in the past one month. The company is one of the largest suppliers of liquor and is supporting over 1,600 independently owned food stores in Australia, including the well-known IGA and Foodland brands. The company is prioritising the successful execution of MFuture plans, which is well supported by the quality and dedication of the Board and MTS’s retailers. Considering the returns, decent financial performance over the past five years, growth opportunities, and future expectations, we have valued the stock using the price to cash flow based relative valuation approach, and arrived at a target price of lower double-digit growth (in percentage terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $2.780, down by 1.418% on 24 February 2020..png)

MTS Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...