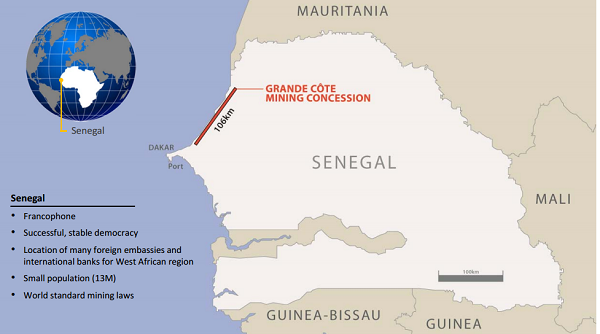

Company Overview - Mineral Deposits Limited (MDL) is an Australia-based company focused on the mineral sands sector through the joint venture interest in TiZir Limited (TiZir). MDL and ERAMET SA each own 50% of TiZir, which owns the Grande Cote Mineral Sands Project in Senegal, and the Tyssedal ilmenite upgrading facility in Norway. The Grande Cote Mineral Sands Project is located on the coast of Senegal starting approximately 50 kilometers north of Dakar and extends northwards for more than 100 kilometers. The main Heavy Mineral (HM) deposits identified to date are Diogo, Mboro, Fass Boye and Lompoul. In January 2014, Mineral Deposits Limited disposed its interest in Teranga Gold Corporation.

Analysis – Mineral Deposits has a 50% interest in the TiZir joint venture with ERAMET, a €1.7b market capitalization French multinational mining and metallurgy company. TiZir was formed in October 2011 through the combination of Mineral Deposits’ 90% interest in the Grande Cote mineral sands project in Senegal and Eramet’s Tyssedal ilmenite upgrading facility in Norway. At full production the project is expected to produce approximately 575ktpa of ilmenite, 85kt of zircon, 6kt of rutile, and 11ktpa of leucoxene, this would position Mineral Deposits as the fifth largest producer of TiO2 feedstock (4% market share) and the fourth largest producer of zircon (6% market share).

Dry Mill at the Mineral Separation Plant (MSP) (Source - Company Reports)

Dry Mill at the Mineral Separation Plant (MSP) (Source - Company Reports)

MDL has announced TiZir is raising an additional US$125m debt via an increase of its existing US$150m senior secured bond. Terms of the incremental debt are similar to the existing bond with a 9% coupon and a Sep2017 maturity priced at 102.9% of par, resulting in an 8% yield to maturity. We had estimated MDL would require an additional US$70m in debt to fund the ramp up of Grande Cote and a further $60m to fund the Tyssedal reline. The US$125m facility broadly matches our expectations; however securing it at this stage well ahead of the Tyssedal reline leaves a funding buffer of US$55m for the ramp up of Grande Cote.

Grand Cote Location (Source - company Reports)

Grand Cote Location (Source - company Reports)

Our forecasts had incorporated an additional US$70m of debt to cover the working capital requirements at Grande Cote. We considered this a conservative estimate given we model a two year ramp up versus management’s target of one year. With US$125 debt raised TiZir is well placed to cover any further delays or minor rectification work. The Tyssedal reline due Q32015 is expected to cost $70 – 100m depending on final scope. We had assumed a further $60m in debt for this work to be drawn 2H 2015. This now can also be funded out of cash flows and the debt facilities in place assuming Grande Cote does not absorb the buffer.

Dredge and Wet Concentrator Plant (Source - Company Reports)

Dredge and Wet Concentrator Plant (Source - Company Reports)

If Grande Cote does absorb the funding buffer there are further funding options for MDL and TiZir. At the group level, MDL held US$30m in cash at March 31’ this remains available to inject into TiZir if necessary. In addition there remains scope increase the US$50m working capital facility within TiZir. We would expect this facility to be expanded once Grande Cote is further into production.

Storage and conveyor facilities at Dakar Port (Source - Company Reports)

Storage and conveyor facilities at Dakar Port (Source - Company Reports)

MDL remains the only company outside of the majors specifically Rio Tinto and Tronox, to be vertically integrated with a producing mineral sands mine and ilmenite upgrading facility in Norway, which there are only five of globally. The book value of these assets is around US$1.0bn. MDL has addressed the market’s financing concerns without issuing equity should be viewed as a material positive, given it removes financing risk leaving only commissioning risk at Grande Cote.

Titanium Dioxide Prices and Zircon Prices (Source - Company Reports)

Titanium Dioxide Prices and Zircon Prices (Source - Company Reports)

Mining at Grande Cote first commenced in late march with the sand being processed through the Wet Concentrator Plant (WCP). In Mid-April the failure of mechanical seals on two major pumps caused almost a month of downtime for the WCP. Since mining recommenced the newly installed mechanical seals have operated trouble free. Since 9 May 2014, the WCP has been operating on full plant and consistently improving in reliability and production. In recent weeks feed rates well above 4,000 tonnes per hour have been recorded on several days, including some days at more than 5,000tph. Name plate capacity is 7,000tph with expected steady state utilization of 89%. Heavy mineral concentrate production rates of 1200 to 1400 tonnes have been produced on a number of days, with the midpoint representing approximately 50% of expected full production rates.

Titanium & Zircon Consumption (Source - Company Reports)

Titanium & Zircon Consumption (Source - Company Reports)

Whilst it is expected to take up to 12 months to reach full production rates on a steady state basis, the progress achieved in the first effective month of mining has been ahead of design ramp up. Feed rates through the WCP will remain restricted over the next few months as tails are pumped through land based lines off the mine path to enable the size of the dredge pond to be increased. The wet plant at the Mineral Separation Plant has had its first real production runs since the beginning of this month, operating close to design for throughput and yield. It is planned to run both non-magnetic and magnetic concentrates through the dry plant over the next month.

MDL daily chart (Source - Thomson Reuters)

MDL daily chart (Source - Thomson Reuters)

In our view the key risks with MDL are: (1) Project execution with the company yet to prove that Grande Cote can operate at targeted costs and production rates. (2) While we don’t forecast that any further capital will be required, we do not expect much free cash flow to be generated by TiZir for the next two years given the US$70 - $100m reline of Tyssedal expected in 2015. (3) Grand Cote is located in Senegal which is ranked 178

th out of 189 countries in terms of business risk by the 2013 Doing Business report.

As well as leverage to mineral sands prices which are expected to increase, our positive view is based on valuation which remains appealing, thus de-risking the project should see the stock well supported. With the Grande Cote build complete build risk and the likelihood of a material capital overrun has been removed. We like the MDL story and put a BUY recommendation on the stock at the current price of $1.63

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...