Kalkine has a fully transformed New Avatar.

Company Overview: Mineral Resources Limited is a provider of mining infrastructure services in Australia. The Company is engaged in the integrated supply of goods and services to the resource sector. The Company operates in three segments, which include Mineral Services and Processing, Mining, and Central. The Company provides pit to port solutions across the mining infrastructure supply chain, including mining, crushing, processing, materials handling and support logistics. Its integrated infrastructure services include remote, mine-site accommodation services; remote power services; dewatering; equipment hire; mobile processing services; pipeline and water solutions; port logistics; ship loading; commodity sales and marketing; mine scheduling and grade control, and beneficiation services. It operates as a mining services contractor, infrastructure owner, infrastructure manager and mine operator based on prudent selection of critical infrastructure projects.

.png)

MIN Details

In-Line Q3FY19 Performance, Expecting Decent Iron Ore Production by Q1FY20: Mineral Resources Limited (ASX: MIN) is a mid-cap mining services and processing company with the market capitalisation of ~$2.89 Bn as of May 08, 2019. Its mining related services include crushing, processing, road & rail bulk haulage, camp services, and marketing & shipping. Its major focus is on commodities such as Lithium and Iron Ore. Recently, the company disclosed Q3FY19 results wherein the group delivered March Quarter total iron ore production of 2,671,000 wet metric tonnes (WMT) against the production of 2,327,000 WMT in the previous quarter (Q2FY19). Moreover, the company shipped total iron ore of 3,307,000 WMT in Q3FY19, showing an increase of 41.0% against the prior quarter shipments. It was mainly driven by the successful ramp up of Koolyanobbing. During the quarter, the company submitted the binding Asset Sale and Share Subscription Agreement between Mineral Resources and Albemarle Corporation regarding the sale of a 50% interest in the Wodgina Lithium Project, to the relevant regulatory authorities in Australia and China. The Completion of the transaction is still anticipated to occur in CY19. Moreover, the Koolyanobbing site achieved its target annualised run rate of 6Mtpa of iron ore production, and plans have been developed to increase production to 8Mtpa by Q1 FY20. Spodumene concentrate production from the Mt Marion project remained in line with Q2 FY19, shipping 111,287 wet metric tonnes (WMT) with 66% of output being high-grade 6% Li2O product.

.png)

Production & Commodity Shipments Data (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form around 30.76% of the total shareholding. Ellison (Christopher James) and Perpetual Investment Management Limited hold maximum interest in the company at 11.59% and 4.96%, respectively.

.png)

Top 10 Shareholders (Source: Thomson Reuters)

YTD March’19 Operational Highlights: The Lithium is extracted from two mines, Wodgina and Mt Marion. Wodgina is located in the Pilbara with 259 mt of resources. It is being developed to produce 750 ktpa spodumene concentrate. Mt Marion is located in the Goldfields with 71 mt of resources. It is being developed to produce 450 ktpa spodumene concentrate.

.png)

Project Sites at Pilgangoora & Wodgina (Source: Company Reports)

The iron ore is extracted from mines Koolyanobbing which is located in the Yilgarn – 400 km east of Perth, and Iron Valley which is located 300 km SE Port Hedland. Both these mines produce medium grade Iron ore with combined production of 14mtpa.

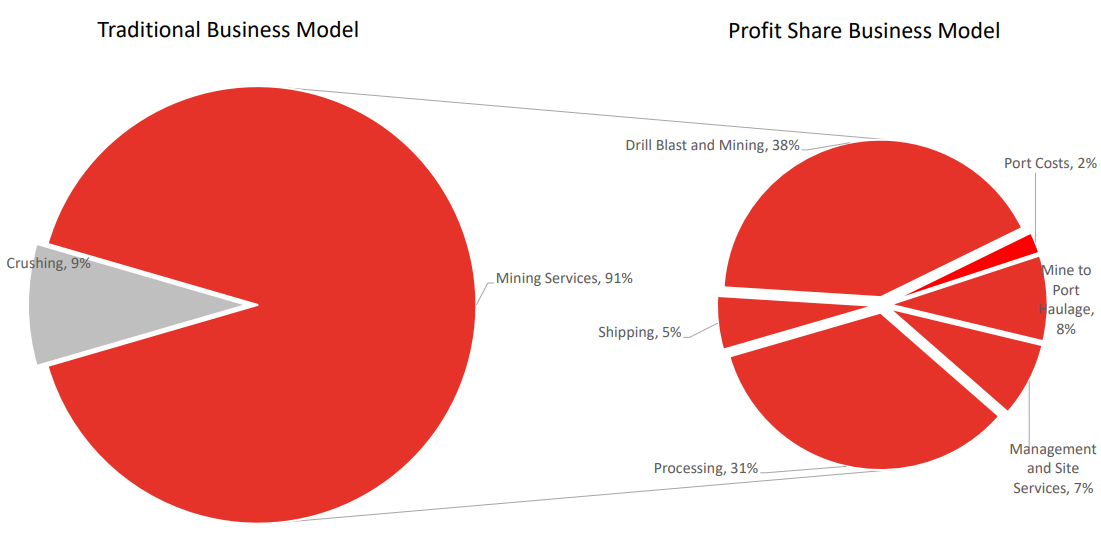

The company is working currently on 4 profit sharing projects where it has taken equity position in the ore body. Moreover, the Joint Venture owners have been granted a life-of-mine contract to build, own, operate (BOO) service. Under extensive supply chain infrastructure, strategic port has been allocated along with road train and rail networks. Currently, MIN is developing unique mining equipment solutions with high barriers to entry to retain its competitive advantage in the mining services business.

Its profit-sharing model with potential partners includes project stake acquisition to provide BOO development and services. Projects are then developed at lowest cost and expedited time frame. Various optimisation measures are utilized in order to increase efficiency and maximise profitability. The project divestment opportunity is identified for maximum capital gains. In the entire process, MIN endeavours to provide range of innovative products to deliver best possible value. Few innovative products & services are CarbonArt, NextGen Crushing, Synthetic Graphite Production and Pilbara infrastructure project. Partners get benefitted financially as projects are delivered quickly and on budget.

Profit Sharing Model (Source: Company Reports)

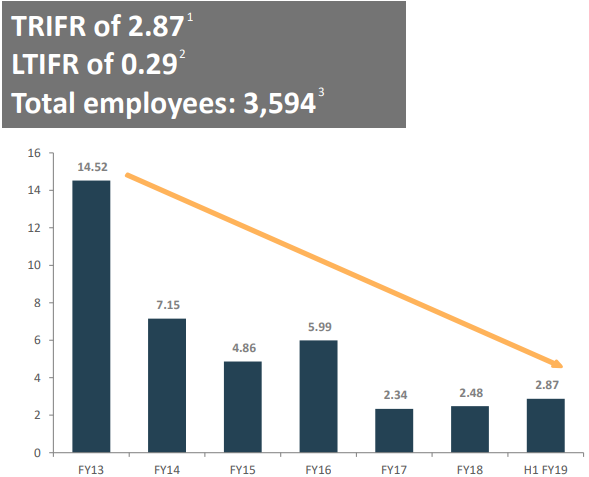

MRL competitive advantage: It delivers innovative high quality and cost-efficient mineral processing and mining infrastructure pit-to-port solutions to its clients. Its core business of ‘build own operate’ solutions reduce the need for the clients to use their own capital. Its innovative, high quality designs lead to significant operating efficiencies with specific focus on crushing, screening and processing activities. This provides clients the opportunity to achieve lower costs of production. It has stood well on all the safety parameters for the second consecutive year. It reported TRIFR at 2.87 and LTIFR at 0.29. Its safety initiatives include the induction of enhanced safety measures along with the implementation of mobile real time reporting for lead safety indicators.

Occupational Health & Safety (Source: Company Reports)

Successful completion of US Unsecured Notes Offering: MIN recently completed an offering of US$700 Mn in Senior Unsecured Notes (8-year term) with maturity in 2027. The proceeds will be used to refinance existing credit facilities and general corporate purposes including capital expenditures. It is expected that the net cash position will be reflected on the balance sheet following the completion of Albemarle transaction during CY19.

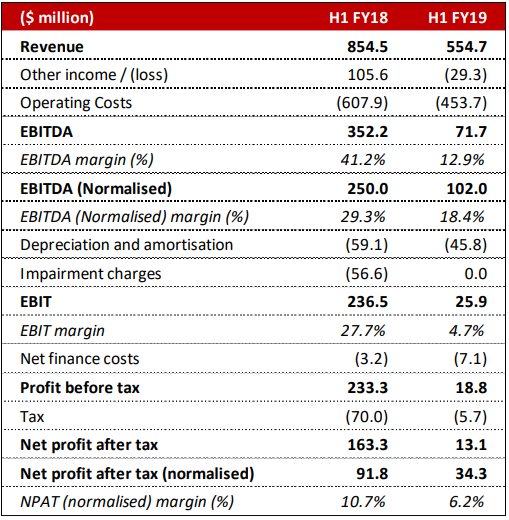

H1FY19 Financial Performance: MIN reported a decrease in revenue and EBITDA by 35% and 80% to $554.7 Mn and $71.7 Mn, respectively in 1HFY19 as compared to the previous corresponding period. This was primarily on the back of following reasons, i.e., (1) ceased Direct Shipping Ore (DSO) activities at the Wodgina Lithium Project in September 2018 in favour of higher-value beneficiation of spodumene concentrate, (2) experienced delays in approvals for the start-up of the Koolyanobbing Iron Ore Project, resulting in first ore shipped in December 2018 rather than at the end of September 2018, (3) received lower pricing for its iron ore from the Iron Valley Project, due to higher discounts for fines and impurities, and (4) increased logistics & shipping costs, predominantly due to higher prevailing fuel costs. Normalised NPAT stood at $34.4 Mn in 1HFY19. Net cash from operations decreased by 90% pcp to $21.6 Mn, reflective of the development phase of the business. Working capital outflow was reported at $80.4 Mn, primarily due to commencement of Koolyanobbing operations, resulting in build-up of inventory levels and receivables net of payables and increased inventories associated with Mount Marion and Wodgina mining operations.

Growth and investment capex in 1HFY19 was reported at $468.2 Mn. It includes the capital expenditure of $330 Mn for Wodgina spodumene concentrate plant and related infrastructure construction; $60 Mn for Mt Marion beneficiation plant upgrade and related infrastructure; and $27 Mn in the acquisition of Kumina tenements. Despite the soft performance in 1HFY19, the company reiterated its EBITDA guidance in the range of A$360-390 million for FY19.

H1FY19 P&L Statement (Source: Company Reports)

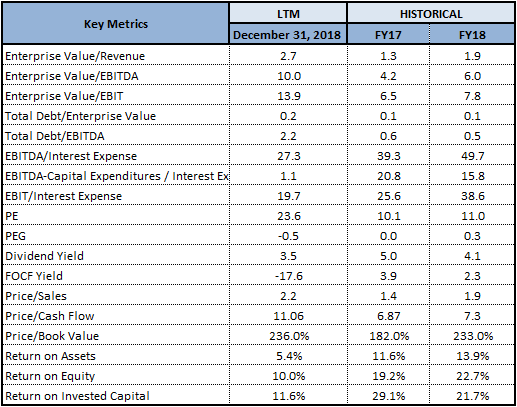

Key Ratios: Its gross margin and EBITDA margin for H1FY19 stands at 95.9% and 18.3% better than the industry median of 28.7% and 13.3% respectively, which implies decent financial performance by the company than its peer group. Its quick ratio for H1FY19 stands at 0.94x better than the industry median of 0.83x, which implies that the company is in a better position to address its short-term obligations than its peer group.

.PNG)

Key Ratios (Source: Thomson Reuters)

What To Expect: In mining services, the company expects that growth for the next 12 months would be greater than 20% in external crushing business, majorly due to revenue from Koolyanobbing mining services. Moreover, the company retained crusher at Wodgina under build, own, and operate (BOO) services, and life-of-mine (LOM) contract. In Lithium segment, the commencement of spodumene concentrate sales is expected at Wodgina site, whereas continued sales of spodumene concentrate to Ganfeng is expected to be according to offtake arrangement at Mt Marion site. In Iron Ore segment, the production of iron ore is expected in the range of 6 mtpa to 8.0 mtpa by August 2019 at Koolyanobbing site, whereas production of iron ore at Iron Valley is expected to be steady at 8 mtpa with low grade iron ore & with high impurities. MIN wishes to become self-sufficient in gas supply in the next 12 months. It has a strong focus on reducing reliance on diesel fuel through innovation and application of other sources of energy.

FY19 Earnings Guidance: It is expected that FY19 Earnings Before Interest, Tax, Depreciation and Amortisation (EBITDA) at a consolidated group level is expected to be in the range $360 million to $390 million. The guidance has been estimated over assumptions of pricing for lithium (spodumene concentrate) and iron ore. Major assumptions include:

- Spodumene concentrate price: US$682.38 per tonne (6%)

- CFR 62% Fe: US$83.89 per tonne

- AUD/USD: 0.723 cents.

Key Valuation Metrics (Source: Thomson Reuters)

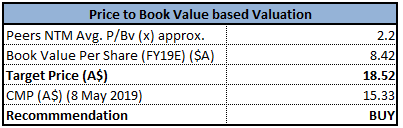

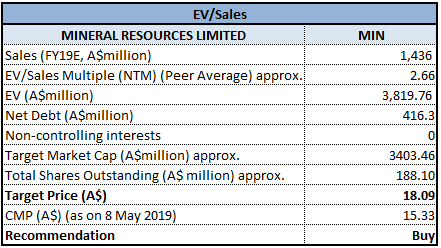

Valuation Methodology:

Method 1- Price to Book Value multiple Approach (NTM):

P/BV Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

Method 2-EV/Sales Multiple Approach (NTM):

EV/Sales Multiple Approach (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: Mineral Resources generated a positive YTD return of 2.81%, while in the span of 6 months, MIN generated a gain of 0.20%. During the third quarter of FY19, the company showed improvement in the production and shipment of its minerals, which is a good sign for the business in the forthcoming year. It has revised its EBITDA guidance from earlier range of $280 Mn to $320 Mn to new guidance range of $360 Mn to $390 Mn. Considering the bright prospects of the business over the long term, we have valued the stock using two Relative valuation methods, Price/Book Value ratio and EV/Sales multiple and arrived at a single-digit upside growth in the next 12-18 months. Hence, considering the aforesaid facts and current trading levels, we recommend a “Buy” rating on the stock at the current market price of A$15.33 (down 0.325% on May 8, 2019).

.png)

MIN Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...