Kalkine has a fully transformed New Avatar.

Company Overview: New Hope Corporation Limited is an Australia-based diversified energy company. The Company's principal activities include coal mining, oil and gas, marketing and logistics, and investments. It operates through four segments: Coal mining in Queensland, which includes mining related exploration, development, production, processing, transportation, port operations and marketing; Coal mining in New South Wales, which includes mining production, processing, transportation and marketing; Oil and gas, which includes oil and gas related exploration, development, production and processing, and Treasury and investments, which includes cash, held to maturity investments and available for sale financial assets. The Company also has its business interests in port operation, agriculture and technologies. It has two open cut coal mines in South East Queensland that produce thermal coal: New Acland and Jeebropilly.

.png)

NHC Details

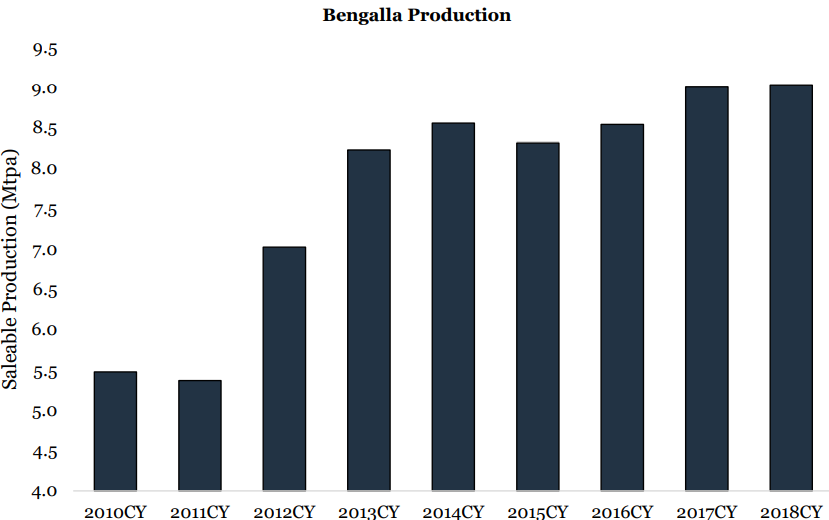

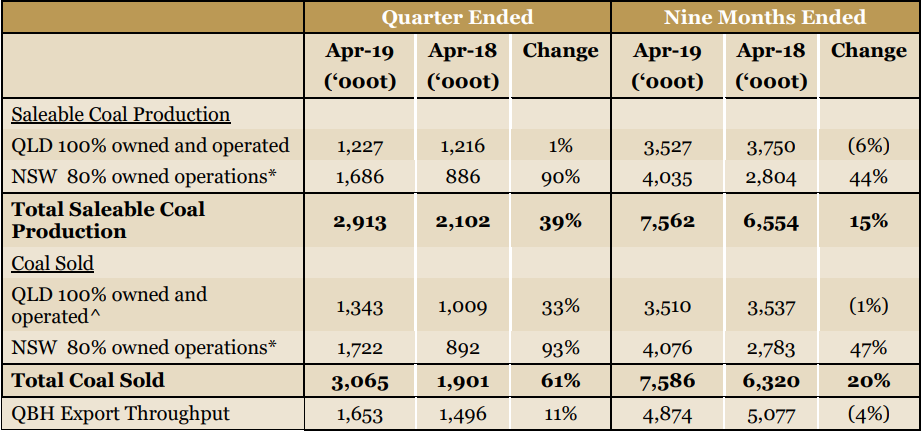

April’19 Quarter Key Highlights: New Hope Corporation Limited (ASX: NHC) has an engagement in coal exploration and project development in Queensland, coal extraction and processing in Queensland and New South Wales, marketing and logistics, agriculture; and exploration, development, production and processing of Oil & Gas. Recently, the company released its Quarterly Activity Report for the quarter ended 30 April 2019 wherein total saleable coal production and total coal sold grew by 39% and 61%, respectively, in Q3FY19 as compared to the prior corresponding period. Further, on March 12, 2019, NHC was advised by Queensland Department of Environment and Science that it had granted application to amend the Environmental Authority for New Acland Coal Mine Stage 3 Project. During Q3FY19, the company completed the acquisition of a further 10% of the Bengalla Joint Venture to a final interest of 80% in late March 2019 and there are expectations that it will continue to deliver significant benefits moving forward. Bengalla mined 2.8 million tonnes of Run-of-Mine (ROM) coal, produced 2.3 million tonnes of saleable coal and sold 2.3 million tonnes. In Q3FY19, New Hope’s share of coal produced was around 1.7 million tonnes at Bengalla, which were 90% above the prior corresponding period. The site increased its truck fleet numbers during the quarter, which will assist in its plans to increase the throughput capacity in the short term. Through debottlenecking and incremental expansion, the Bengalla operation is now producing at an annualised rate of approximately 10 million tonnes of saleable coal.

On the 1HFY19 performance front, the company reported NPAT (before non-regular items) of $160 Mn, which is 33% higher than the prior corresponding period. It sold around 4.5 Mn tonnes of coal in the period which is an increase of 2% as compared to the previous corresponding period. Based on the 1HFY19 performance, the Board of Directors declared an interim dividend of 8 cents per share, which was an increase of 33% as compared to the previous corresponding period. Decent coal outlook till the year 2040 with strong demand growth from India and South Asian countries is expected to help the company in delivering sustainable value to its customers and shareholders in the coming times. From the analysis standpoint, the company's top-line and bottom-line have grown at a CAGR of ~18.4% and 26.4%, respectively, over the period of FY14-FY18. We expect that this respectable CAGR growth in its top line and bottom line (FY14-FY18) might also attract the attention of market players.

Bengalla Coal Production Data (Source: Company Reports)

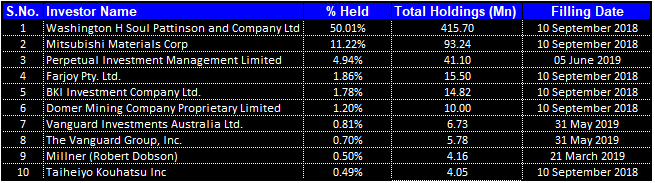

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form around 73.51% of the total shareholding. Washington H Soul Pattinson and Company Ltd. and Mitsubishi Materials Corp are holding maximum interest in the company at 50.01% and 11.22%, respectively. Recently, the company informed that Perpetual Limited and its related bodies corporate have ceased to be the substantial holder in the company, effective from June 5, 2019.

Top 10 Shareholders (Source: Thomson Reuters)

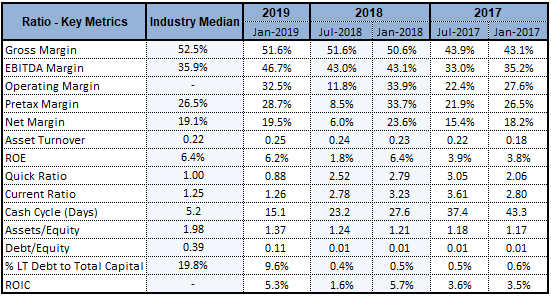

Key Ratios: Its EBITDA margin and net margin for H1FY19 stand at 46.7% and 19.5%, which are better than the industry median of 35.9% and 19.1%, respectively, implying a decent financial performance by the company than its peer group. Its debt-to-equity ratio for H1FY19 stands at 0.11x, which is lower than the industry median of 0.39x, which implies the company is less leveraged as compared to its peer group. Its gross margin has improved from 50.6% in H1FY18 to 51.6% in H1FY19.

Key Ratios (Source: Thomson Reuters)

Total Coal Sold increased by 61% pcp in April’19 Quarter: The total saleable coal production in Q3FY19 increased by 39% to 2.9 Mn tonnes as compared to 2.1 Mn tonnes in April’18 Quarter. The major increase in the Saleable Coal production was due to production at New South Wales (NHC owns 80% operation) which increased by 90% pcp to 1.69 Mn tonnes. The total Coal sold increased by 61% from 1.9 Mn tonnes in April’18 Quarter to 3.07 Mn tonnes in April’19 Quarter.

April’19 Quarter Production Data (Source: Company Reports)

No Safety related Incidents During Q3FY19 at the Bridgeport: Lost Time Injury-free period at the Bridgeport now stands at 1,697 days. Oil production totalled 93,137 barrels for the quarter, with 80,544 barrels of oil being sold in line with the prior corresponding period. The average realised oil price for the quarter was US$69/bbl (A$98/bbl). The company’s drill rig, after completing its annual workover activities at the Kenmore and Bodalla South fields, moved to the Inland field and as at end of the quarter had completed two of three workovers scheduled for that field. Production from non-operated fields has supported production levels as a result of successful development wells drilled in those tenements which were progressively brought on line during the quarter. Bridgeport closed a transaction on three exploration tenements in the north east Cooper Eromanga area near Jundah, Qld, thus acquiring the Senex interests in ATPs 736, 737 and 738. Bridgeport now holds a large area (8,434 km2) encompassing the Toolebuc shale play in the Jundah area with planning work progressing for appraisal activities.

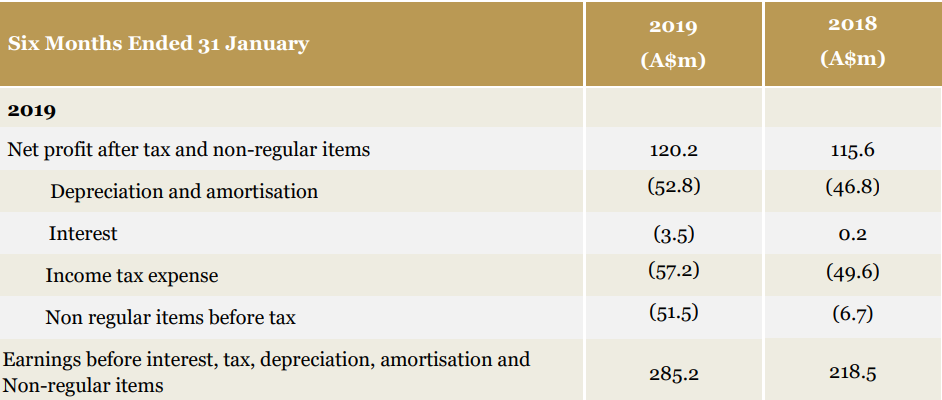

H1FY19 Key Highlights: The company’s revenue for the first half was $616.7 million, reflecting a rise of 21% on the prior corresponding period (or PCP) being the six months ending 31 January 2018. Also, New Hope Corporation’s profit before tax and non-regular items amounted to $228.9 million reflecting a rise of 33% on the PCP. NHC’s earnings before interest, tax, depreciation and amortisation, before non-regular items, was $285.1 million reflecting a rise of 31% on the PCP. However, its net profit after tax before non-regular items was $159.8 million (up 33% on the PCP). The company’s Board had declared a fully franked interim dividend of 8 cents per share, which is 33% higher than the prior corresponding period.

EBITDA (Before and After Non-Regular Items) (Source: Company Reports)

The Earnings before interest, tax, depreciation, amortisation and non-regular items increased by 30.53% from $218.5 Mn in H1 FY 2018 to $285.2 Mn in H1 FY 2019.

NPAT (Before and After Non-Regular Items) (Source: Company Reports)

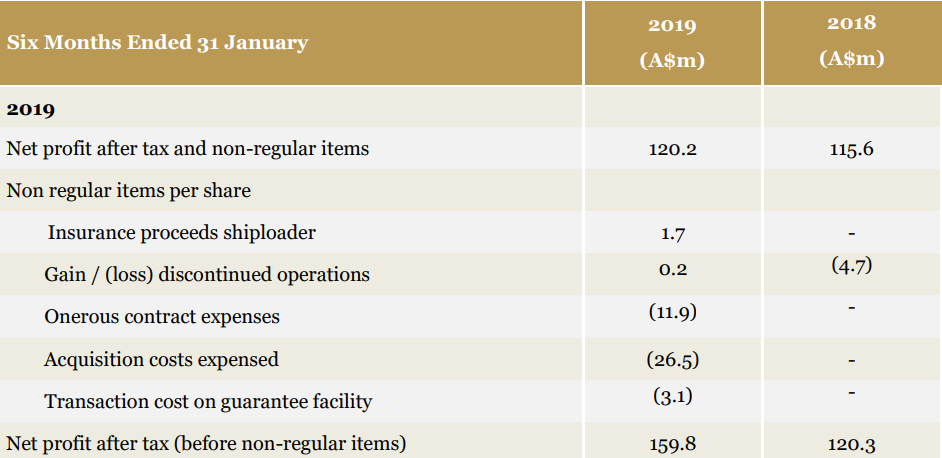

The net profit after tax (before non-regular items) increased from $120.3 Mn in H1FY18 to $159.8 Mn in H1FY19, whereas the net profit after tax and non-regular items increased from $115.6 Mn in H1FY18 to $120.2 Mn in H1FY19.

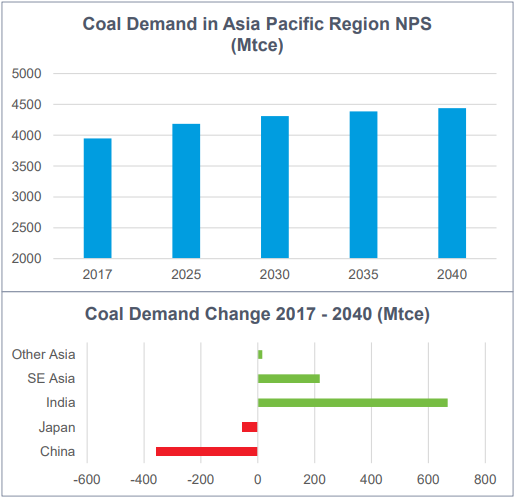

Coal Outlook: As per the International Energy Agency’s Global Energy & CO2 status report issued in March, global coal demand increased by 0.7% or 40 Mtce in the year 2018. In late 2018, the global economic growth slowed, and China introduced several policies aimed at deterring coal imports. China’s policies are targeted to support its domestic coal industry, which has been under pressure from lower domestic coal prices during 2018. Strong enforcement of these restrictions has placed pressure on exports of coals which were bound for the Chinese market to redirect into other markets such as Japan, Korea, Taiwan, and India. All these countries are demand lower ash, higher energy coals for environmental reasons. Coals at NHC’s Surat Basin have low ash and sulphur, and comparatively high energy and low emissions.

Developing Asia is reliant on new technology coal plants for the most cost competitive electrification of their countries. Development of gas and renewables in Asia is encouraging but the countries are most likely to continue to take a balanced and risk-averse approach to maintain continuous electricity supply for which the coal is still required. In total, new thermal plants will generate demand for ~600 Mtpa of coal. Excluding countries that have their own coal resource, these plants will require an additional ~130 mtpa of seaborne thermal coal.

Region Wise- Coal Demand (Source: Company Reports)

What to expect: The company is well positioned to meet the growing energy demands of its Asian customers. With the active management of the Bengalla Joint Venture, NHC is expected to increase its production levels along with improving safety performance. It is also expected that NHC would be able to secure approval for the New Acland Stage 3 project, following which it will develop Lenton Joint Venture Burton Mine.

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology:

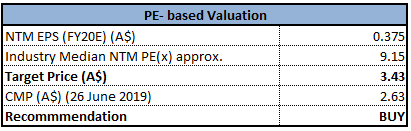

Method 1- Price/Earnings Multiple Approach (NTM):

Price/Cash Flow Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

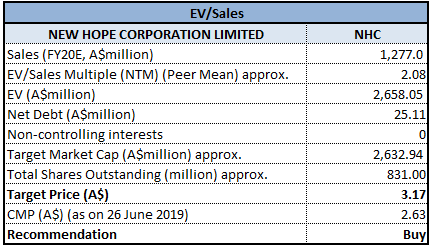

Method 2- EV/Sales Multiple Approach (NTM):

EV/Sales Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

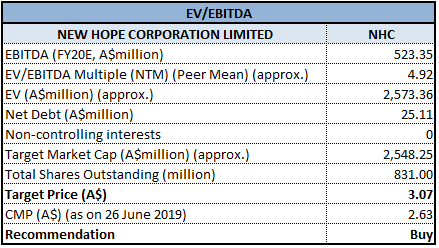

Method 3- EV/EBITDA Multiple Approach (NTM):

EV/EBITDA Multiple Approach (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

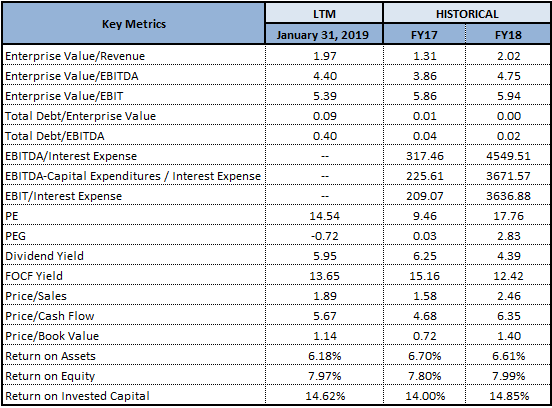

Stock Recommendation: New Hope Corporation’s shares generated a negative YTD return of 18.24% and is trading close to 52-weeks lower level of $2.525 with reasonable PE multiple of 14.54x, indicating a decent opportunity for accumulation. Fundamentally, the company has performed well on its financial books, as its EBITDA margin and net margin for H1FY19 stood above the industry median. Its gross margin improved in the first half of the financial year 2019 as compared to the previous corresponding period. Its debt-to-equity ratio shows that the company is less leveraged than its peer group and is utilizing its own funds to fuel the projects. Moreover, coal demand is expected to grow in the countries such as India and South East Asia, till the year 2040. It will help the coal producing companies to deliver sustainable value to its customers and shareholders. With the decent volume growth visibility, healthy balance sheet, respectable operating margins and return ratios, we have valued the stock using three Relative valuation methods, P/E, EV/Sales, and EV/EBITDA multiple and arrived at a double-digit upside growth (in %) in the next 12-18 months. By looking at the aforesaid parameters, we recommend a “Buy” rating on the stock at the current market price of $2.630 per share (down 2.23% on June 26, 2019).

) (1).png)

NHC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...