Newcrest Mining Limited (Newcrest) is a gold mining Company, operating in the Asia Pacific region and West Africa. The Company’s asset portfolio includes operating mines that use a variety of efficient mining methods for large ore bodies, together with selective underground mining methods to optimize high-grade epithermal deposits. Its mines are located in Australia, Papua New Guinea (PNG), Indonesia, and in Cote d’Ivoire, West Africa. The Company’s operations include Cadia Valley Operations (near Orange, New South Wales), Telfer (Pilbara Region, Western Australia), Gosowong (Halmahera Island, Indonesia), Lihir (New Ireland Province, PNG), Hidden Valley (Morobe Province, PNG), Bonikro (Cote d’Ivoire, West Africa), Wafi-Golpu, PNG and Namosi, Fiji.

Enhanced Production boosted earnings: Newcrest Mining Limited (ASX: NCM) reported a revenue increase of 8% yoy to $ 4,344 during the fiscal year of 2015, and accordingly the Statutory profit rose to $546 million against the Statutory loss of $2,221 million in the prior corresponding period (this was mainly due to asset impairments of $2,353 million in FY14). Subsequently the underlying profit surged 19% yoy to $515 million during the period driven by better contribution of higher margin production at Cadia East coupled with positive net impact of falling Australian Dollar as compared to the US Dollar during fiscal year of 2015. As per the production highlights, Gold production slightly increased by 1% yoy to 2.423 million ounces on the back of increase in Cadia East underground mine, higher ore feed grades at Gosowong and West Africa, coupled with better milling rates at Lihir which partly offset the impact of lower ore feed grades at Lihir during FY15. Meanwhile, NCM improved its copper production by 12% yoy to 96.8 thousand tonnes driven by better processing of higher copper grade ore from Cadia East.

.png)

Fiscal year of 2015performance (Source: Company Reports)

Strong cash generation: Newcrest Mining generated a free cash flow of $1,086 million in fiscal year of 2015, an increase of $953 million as compared to fiscal year of 2014, driven by enhanced cash flow generation among all operations except Hidden Valley. As a result, NCM also repaid USD 760 million of debt and rose the cash by USD 65 million. Moreover, the group’s debt is USD-denominated and accordingly falling Australian dollar decreased NCM’s debt by $174 million post translation to AUD at 30 June 2015. Subsequently, USD net debt fell by USD 819 million or 22% yoy to USD 2.89 billion or AUD 3.76 billion as at 30 June 2015. The group’s edge program also generated a cash benefits of over AUD 390 million to date and cultural change. The group’s net debt to EBITDA is 2.2 times, which is 15% yoy decrease as compared to the corresponding period in last year. Newcrest’s gearing ratio fell to 29.3% as at 30 June 2015, as compared to 33.8% in the corresponding period of last year.

.PNG)

Free cash flow generation (Source: Company Reports)

Improving assets potential: NCM decided to retain Telfer and West Dome Stage 2 and Main Dome Stage 6/7 were approved. The group estimates to incur a capex of about $46 million and intends to extend open pit to December 2017. M-Reefs and Sub Level Cave are projected to operate till FY19 and FY20 respectively. Meanwhile, the Vertical Stock Corridor option investigation is ongoing which might witness underground mining continue beyond FY22. As per the Lihir project highlights, NCM intends to finish the Pre-Feasibility Study by this year end, which includes mine plan optimization, review seepage barrier options to ensure cash flow maximization , capital efficiency and risk mitigation. With regards to the Cadia Panel Cave 2 highlights, the project resumed its production from last month and NCM issued a gold production guidance of 2.4 to 2.6 Moz, while the copper production is in the range of 80 - 90 kt. But, due to the seismic event in Feb 2015, the localized damage needed rework and some design tuning while Cave establishment and propagation process needed stress redistribution and release. On the other hand, the group’s world class copper-gold deposit Golpu has Mineral Resources of 9mt of copper and 20moz of gold (100%). The group scheduled Feasibility Study in the ending of this year for Golpu, while permit for advanced exploration and feasibility support was granted. Meanwhile, NCM is also pursuing exploration and new projects to generate value. Accordingly, the group is building an international portfolio. Mungana JV (Queensland, Australia) is located on a metal rich district with Gold-Copper porphyry related mineralization. Southern Coromandel JV (New Zealand) is at highly prospective corridor wherein NCM can also leverage the Gosowong experience to search for high grade epithermal vein style mineralization. Wamum (Papua New Guinea) is adjacent to Wafi-Golpu in Morobe Province with potential for discovery of high grade porphyry mineralization at depth. Wailevu West (Fiji) had historic Mt.Kasi gold mine with porphyry related gold-copper mineralization. Regional Côte d’Ivoire has orogenic gold mineralization at promising structural locations

.png)

Cadia Panel Cave 2(Source: Company Reports)

Focus on Safety remains Priority: NCM faced two fatalities during the fiscal year of 2015, with an employee of the Hidden Valley Joint Venture was fatally injured after being struck by a reversing loader in the milling area. Again on May 15, second fatality happened wherein a contractor working in the underground mine was fatally injured while operating an elevated work platform. Therefore, Newcrest is focusing more on safety of its workforce and intends to eliminate fatalities and life-altering injuries from its operations in the future.

.PNG)

Safety performance (Source: Company Reports)

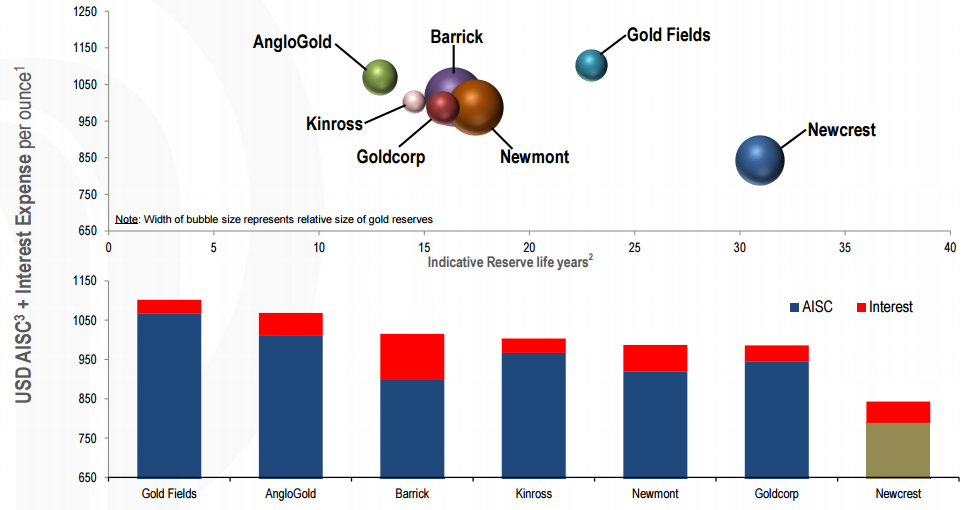

Lower costs: The group’s all-in Sustaining cost reduced by 4% yoy to AUD 941 per ounce due to decrease in production stripping and sustaining capital expenditure, higher byproduct revenue related to higher copper sales volumes, which partially offset the 9% deterioration in the average Australian Dollar against the corresponding period (which increased USD-denominated costs). All-In Sustaining Cost of USD 789 per ounce sold decreased by 12%yoy as compared to the fiscal year of 2014. Meanwhile, Newcrest’s All-in Sustaining Cost expenditure was $2,270 million during the period, while the total capital expenditure reached $564 million. Exploration expenditure stood at $46 million during FY15, which were lower than the group’s guidance range .

Ongoing cost leadership (Source: Company Reports)

Outlook: Newcrest estimates its gold production in the range of 2.4 to 2.6 million ounces while the copper production could to be in the range of 80 to 90 thousand tonnes for the fiscal year of 2016. NCM’s All-In Sustaining Cost expenditure is anticipated to be in the range of $2,650 to $2,950 million, while the group estimates to incur a total capital expenditure in the range of $700 to $825 million, The total exploration expenditure is projected to be in the range of $60 to $70 million while the Depreciation and amortisation is likely to be in the range of $880 to $950 million during the period. NCM intends to achieve a lower Net Debt to EBITDA of less than 2.0 times while estimates its gearing ratio to be less than 25%.

NCM Daily Chart (Source - Thomson Reuters)

Stock Performance: The shares of Newcrest Mining have delivered a year to date returns of 11.6% as compared to the S&P/ASX 200 decline of 5.7% during the same period, driven by the rising gold prices, falling Australian dollar and better productions. In fact the shares have been performing well even during the recent tough market conditions, and accordingly delivered over 2.6% in last four weeks, even though the broader S&P/ASX 200 continued to face pressure and fell over 2.1%. Newcrest Mining have been making several efforts to drive growth in the coming months, by improving production, ongoing cost optimization and through Edge program (which focus on safety, operational discipline, cash generation, profitable growth). The group also has a solid reserves base as compared to its peers with over 75 Moz of gold while its gold reserves life is over thirty one year’s. We continue to remain bullish on the stock, and accordingly recommend investors to “BUY” Newcrest Mining at the current price of $11.93.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...