Company Overview - Newcrest Mining Limited is a gold mining company. The principal activities of the Company are exploration, mine development, mine operations and the sale of gold and gold/copper concentrate. The Company's operating segments are: Cadia Valley, Australia; Telfer, Australia; Lihir, Papua New Guinea; Gosowong, Indonesia; Hidden Valley JV (50% interest), Papua New Guinea; West Africa (includes Bonikro operations and exploration and evaluation activities in Cote d'Ivoire), and Exploration and Other. The Exploration and Other segment comprises projects in the exploration, evaluation and feasibility phase and includes Wafi-Golpu and Morobe Exploration in Papua New Guinea (PNG), Marsden and O'Callaghans in Australia, and Namosi in Fiji. The Company has operating assets in four countries, primarily in Australia and the South-West Pacific region.

.png)

NCM Details

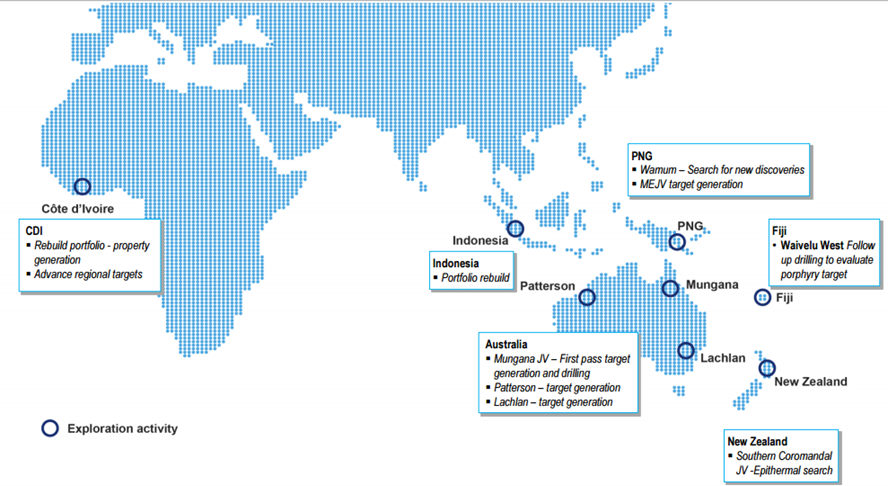

Ongoing exploration efforts: Newcrest Mining Limited (ASX: NCM) has a track record of delivering successful explorations while the group is constantly seeking for potential targets and early entry opportunities. The group has long life assets like Cadia and Lihir mines and is on track to develop Golpu resource, a strong asset wherein the stage one feasibility and stage two pre-feasibility studies are planned to be finished by December of this year. Newcrest Mining intends to spend over $60 to $ 70 million on explorations for fiscal year of 2016. The group is pursuing Greenfields opportunities like aiming gold-copper porphyry related mineralization at Mungana in Queensland as well as intends to leverage its Gosowong experience to search for high grade epithermal vein style mineralization at the Southern Coromandel project in New Zealand. Newcrest Mining entered into a non-binding agreement with Taruga Gold over the Dabakala concession situated in Côte d’Ivoire. During the September quarter, Newcrest Mining performed 10 rigs in operations with five related to exploration with one in Fiji, one in PNG, one in Australia and two in Gosowong while the remaining 5 in resource definition with two in Cadia and three in Telfer. Moreover, recently PT ANTAM (ATM) and Newcrest Mining joined to identify development opportunities for gold and related minerals explorations in many new prospective areas in Indonesia. The agreement areas include West Java, South Sumatera, Nusa Tenggara, North Sulawesi, Halmahera and Mollucas Islands.

Exploration and early stage entry (Source: Company Reports)

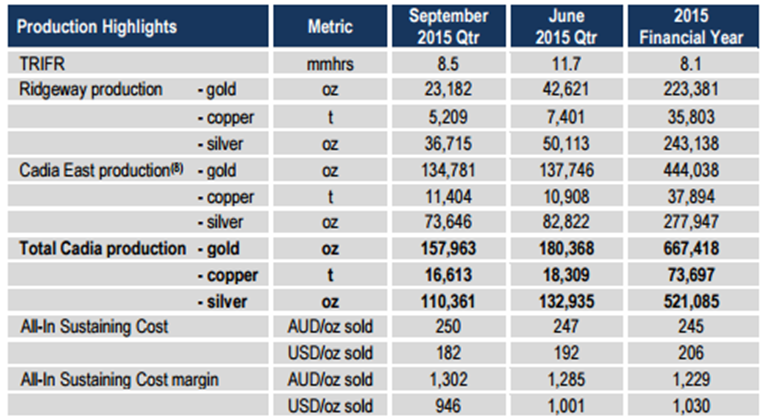

Short term pressure at Cadia, despite long term potential: Cadia operations reported a problem on the motor on concentrator 1 SAG mill during October. The inspection by engineers revealed loose windings than that was expected and the concentrator 1 SAG mill was said to remain offline for around 5 weeks while Concentrator 2 SAG mill was operating at full capacity. However, Newcrest Mining did not disclose the impact of this event on its full year of fiscal year of 2016 production and costs. But the gold production for cadia operations fell to 157,963 oz during the first quarter of 2016 as compared to 180,368 oz in June quarter affected by decrease in grades on the back of planned reduction in head grades at Ridgeway and rising lower grade volumes from Cadia East Panel Cave 2 (PC2). Earlier, Cadia operations also faced a fatality at the Ridgeway mine during September due to which the Ridgeway operations were suspended for 11 Days while Cadia East was suspended for three days to carry out safety reviews and prevent possible re-occurrence of these incidents. Meanwhile, All in Sustaining Costs (AISC) slightly increased to $250 per oz during the September quarter, as compared to $247 per oz in June quarter as decreasing production and lower by-product credits were offset by better efficiencies from Panel Cave 1 (PC1) and PC2. On the other hand, Newcrest Mining delivered solid performance in its cadia operations during 2015 financial year and even continued to enhance its production from Cadia East boosted by improved performance by the Ridgeway mine. Accordingly, Cadia Gold production rose by 13% during fiscal year of 2015 while copper production surged by 22% during the period. NCM also delivered ASIC decrease of 31% against prior corresponding period to USD 206 dollars per ounce during the period. Moreover, Newcrest Mining’s application to boost the Cadia processing plant permit to 32 million tonnes per annum from its present 27 million tonnes per annum had been approved by the NSW Government during September 2015. The group is also seeking the most cost-effective way to expand its plant accordingly.

Cadia Operations September highlights (Source: Company Reports)

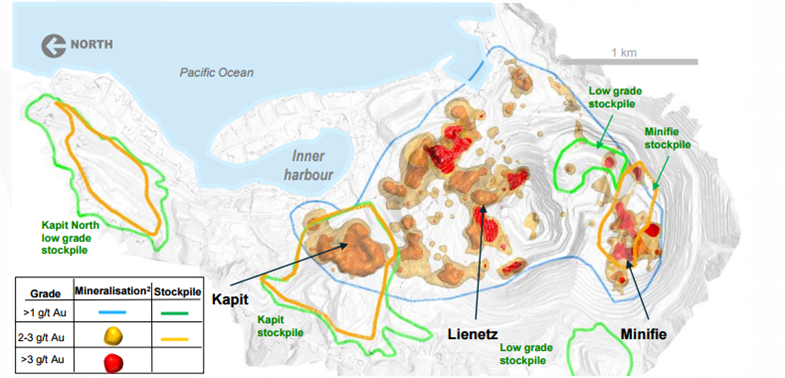

Optimizing Lihir operations: Newcrest Mining is focusing on the maintenance, process control as well as on effective shutdown planning at Lihir operations. With PNG facing drought conditions, Lihir operations is facing challenges and accordingly the company is adopting water conservation efforts to reduce the impact on production. Accordingly, the Gold production at Lihir PNG operations decreased to 190,579 oz during September quarter despite higher feed grade from both ex-pit and stockpile feed as compared to 195,457 oz in June quarter, impacted by increase in maintenance activities. Meanwhile, the operations were able to decrease its USD AISC per ounce to USD 1,008 per oz during the first quarter of 2016, against USD 1,081 per oz driven by decrease in operating costs, sustaining capital coupled with contribution from lower heavy fuel oil costs and weaker PNG Kina. The group estimates to generate 12mtpa milling throughput by the end of December 2015. Newcrest Mining adopted a new operating strategy for Lihir operations to generate a 15% rise in plant throughput during the year with minimal reduction in recovery rates.

Lihir pit optimization study (Source: Company Reports)

Favorable Golpu potential and delivery: Golpu’s progress is on track and the group reported the stage one of the Golpu project to be the feasibility stage during last year December which would be finished by this year end. NCM also received permit for advanced exploration while feasibility support was also granted. The group would be finalizing a suitable framework with the PNG Government. Meanwhile, the Wamum project which is situated over 22km from North-West of Wafi–Golpu is an advanced exploration stage project which has two known copper–gold porphyry systems - Wamum and Idzan Creek. The exploration target is Golpu-style deposits at depth below these two porphyry systems. The group started drilling during the September quarter, wherein the drill testing of the Idzan Creek porphyry center is underway and the holes are designed to test for high grade mineralization at depth.

.png)

NCM Daily Chart (Source - Thomson Reuters)

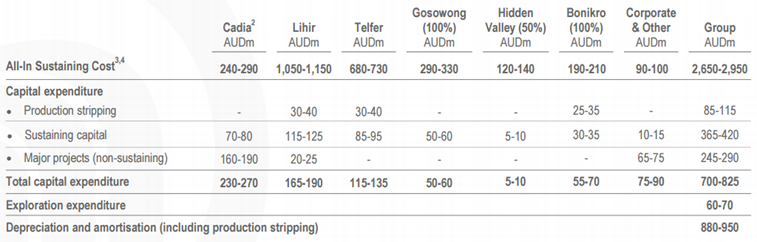

Outlook: Newcrest estimates its gold production in the range of 2.4 to 2.6 million ounces while the copper production could to be in the range of 80 to 90 thousand tonnes for the fiscal year of 2016. NCM’s ASIC expenditure is anticipated to be in the range of $2,650 to $2,950 million, while the group estimates to incur a total capital expenditure in the range of $700 to $825 million. Depreciation and amortization is likely to be in the range of $880 to $950 million during the period. NCM intends to achieve a lower Net Debt to EBITDA of less than 2.0 times while estimates its gearing ratio to be less than 25%.

Cost and Capital guidance (Source: Company Reports)

Stock Performance: Newcrest Mining’s September quarter gold production fell to 583,745 ounces as compared to 673,542 ounces in June quarter impacted by lower production in Cadia. Quarterly copper production also fell to 21,337 tonnes during the quarter from 22,170 tonnes in June quarter. NCM’s ASIC rose to $1,088/oz in September quarter from $978/oz in June quarter. As a result, the shares of Newcrest Mining fell over 22.14% in the last four weeks (as of November 17, 2015) and plunged around 21.19% in the last six months. On the other hand, Newcrest Mining stock delivered a year to date returns of 5.57%, owing to the rising gold prices, falling Australian dollar and better productions. Moreover, the group’s average realized gold prices rose to $1,552/oz during the September quarter as compared to 1,532 /oz during the June quarter. Newcrest Mining undertook several initiatives to drive growth, by enhancing production, continue cost optimization and through Edge program (which focus on safety, operational discipline, cash generation, profitable growth). The group also has a solid reserves base as compared to its peers while its gold reserves life is over thirty one year’s. Further, the outage at Cadia may only have a modest impact on the long-term confidence vested in NCM given the otherwise strong Cadia and Lihir assets. NCM is trading at decent valuations with a P/E of 16x. We continue to remain bullish on the stock, as the current volatile market sentiment might boost the gold prices further. Based on the foregoing, we recommend a “BUY” for Newcrest Mining at the current price of $11.09

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...