Kalkine has a fully transformed New Avatar.

Company Overview: OceanaGold Corporation is a gold mining company. The Company is engaged in the exploration, development and operation of gold and other mineral mining activities. The Company's segments are New Zealand, the Philippines, the United States and All other segments. The Company's assets encompass its flagship operation, the Didipio Gold-Copper Mine located on the island of Luzon in the Philippines. On the north island of New Zealand, the Company operates the high-grade Waihi Gold Mine. On the south island of New Zealand, the Company operates the gold mine in the country at the Macraes Goldfield, which is made up of a series of open pit mines and the Frasers underground mine. In the United States, the Company is constructing the Haile Gold Mine, an asset located in South Carolina along the Carolina Slate Belt.

.png)

OGC Details

Consistently Creating Value and Real Growth: OceanaGold Corporation (ASX: OGC) is a mid-cap gold mining company with the market capitalization of ~$2.64 billion as of May 15, 2019. It is a high-margin, multinational gold producer with four operating assets and a pipeline of exploration opportunities. It aims to operate high quality assets and deliver superior returns for its shareholders. It focuses on maintaining high safety standards along with maintaining a consistent track record of profitability from its business. It wishes to continue to leverage nearly 30 years of operating experience to identify new value-creating opportunities in the Americas, Australasia and Asia-Pacific regions. The company recently published its 2019 investor presentation wherein it updated about the production activity and financial highlights. According to the presentation, the company delivered a positive ROIC over the 8 consecutive years with good EBITDA margins as compared to its peers.

.PNG)

Consistently Creating Value and Growth (Source: Company Reports)

It operates in Haile, Didipio, Waihi, Macraes, and Reefton. It posted a production growth rate of Gold at 10% from the year 2012 to 2018. Its EBITDA growth stood at 20% from the year 2012 to 2018. Its Earnings growth stood at 192% from the year 2012 to 2018, despite the decline in gold price by 24% from the year 2012 to 2018.

In Q1FY19, the production was impacted due to heavy rainfall at Haile which led to increase in ASIC as compared to the previous quarter. With the improvement in the challenging conditions, the overall productivity of OGC is expected to increase which is likely to reduce All-In-Sustaining Costs (ASIC) and, thus, improve overall margins.

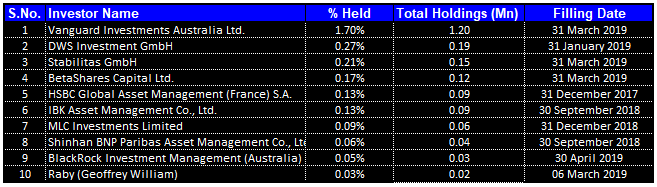

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form around 2.85% of the total shareholding. Vanguard Investments Australia Ltd and DWS Investment Gmbh hold maximum interest in the company at 1.70% and 0.27%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

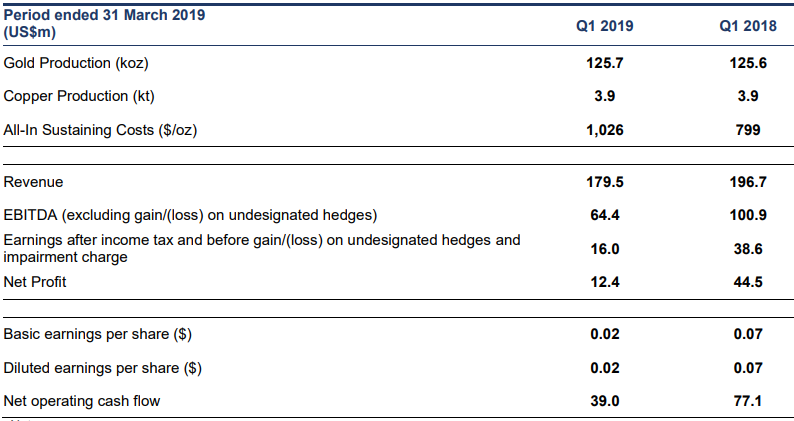

Understanding OGC’s Q1 FY 2019 Performance: OGC, for Q1FY19, reported consolidated gold production of 125,681 ounces which was broadly in-line with Q4 FY18 and Q1FY18. It was mainly impacted by increased production from Didipio, Macraes and Waihi while partially offset by softer production from Haile. Haile continued to be impacted by poor ground conditions and reduced productivity as the mine remained saturated following the heavy rainfall experienced in the fourth quarter and start of the year. Access to higher grades was restricted and pre-stripping the saprolitic clay material proved challenging. The improvement plans implemented by the company this year became effective in March with considerable improvement in productivity and production. The Company also produced 3,910 tonnes of copper and 89,280 ounces of silver in the first quarter of 2019, along with 125,681 ounces of gold.

Its Haile expansion is on track with the installation of regrinding circuit, and commissioning of Isa & Tower mills. Its exploration success continued in New Zealand with an initial resource announced at WKP and an increased resource for the Martha Underground Project.

Recent accolades and awards for Didipo (four Global CSR awards) and Macraes (Environment Excellence Award) indicate for the company’s commitment towards environment and society. The increase in All-in-sustainable cost (q-o-q) reflects lower grades and productivity challenges at Haile. As per the management, EPS and CFPS (Cash Flow from Operations before working capital movements) are broadly in-line with their estimates. It reported consolidated All-In Sustaining Costs (“AISC”) of $1,026 per ounce on sales of 121,144 ounces of gold and 3,324 tonnes copper. It reported revenue of $179.5 million with EBITDA of $64.4 million and a Net Profit of $12.4 million. The cash balance was reported at $86.5 million with total immediately available liquidity of $136.5 million. Total debt including equipment leases was $185.7 million, an increase of approximately $10 million primarily related to the reclassification of capital leases pursuant to IFRS 16. These increases mainly related to the Company’s New Zealand operations.

Production & Financial Metrics (Source: Company Reports)

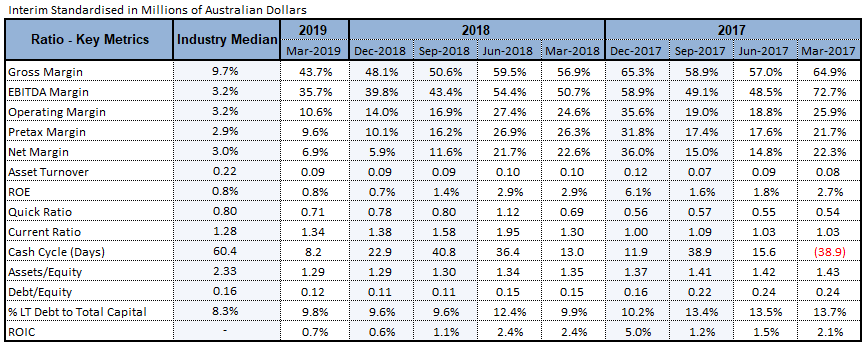

Key Ratios: Its gross margin, EBITDA margin, and net margin for Q1FY19 stand at 43.7%, 35.7%, and 6.9%, better than the industry median of 9.7%, 3.2%, and 3.0% respectively, which implies decent financial performance by the company than its peer group. Its current ratio for Q1FY19 stands at 1.34x better than the industry median of 1.28x, which implies that the company is in a better position to address its short-term obligations than its peer group.

Key Ratios (Source: Thomson Reuters)

Details on Waihi Acquisition: The Waihi project was acquired in November 2015, and the acquisition and development cost for the acquisition in the year 2015 stood at US$101 Mn. Its Net asset value was estimated at US$130 Mn. Its cumulative free cash flow since acquisition till December 31, 2018, stands at US$180 Mn.

Waihi’s Martha underground project has been approved to proceed. As at 31 March 2019, M&I Resource Growth and inferred resource growth were reported at 330K oz and 667K oz, respectively. It was higher than the deposit estimates in August 2018, where M&I Resource and Inferred Resource were reported at 140K oz and 339K oz.

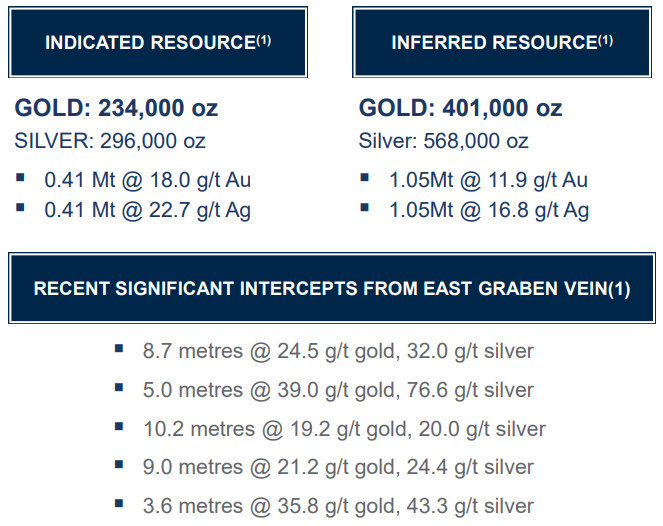

Initial Resource at Wharekirauponga (WKP) is a newly discovered high-grade mineralisation in New Zealand. The indicated resource reported 234,000 oz Gold and 296,000 oz Silver while the inferred resource reported 401,000 oz Gold and 568,000 oz Silver.

Resource at Wharekirauponga (WKP) (Source: Company Reports)

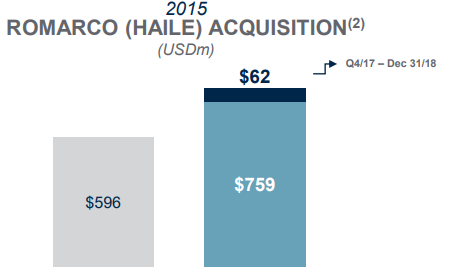

Romarco (Haile) Net Asset Value (NAV) estimated at US$596 Mn: The Romarco (Haile) project was acquired in October 2015, and the acquisition and development cost for the acquisition in the year 2015 stood at US$596 Mn. Its Net asset value was estimated at US$759 Mn. Its cumulative free cash flow since acquisition till December 31, 2018, stands at US$62 Mn.

Romarco (Haile) Acquisition (Source: Company Reports)

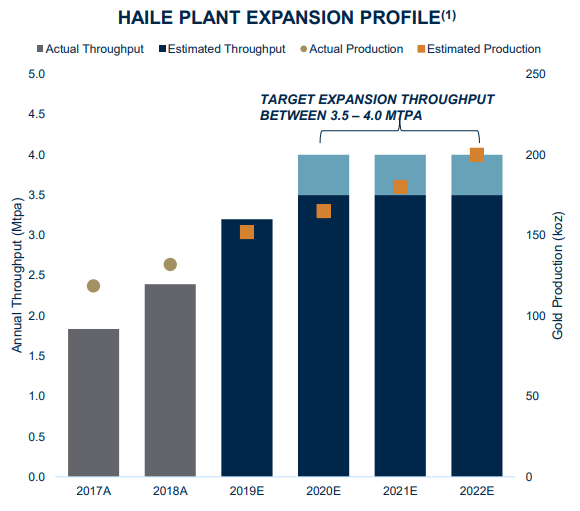

Target Expansion Throughput For Haile Plant: In the year 2018, annual throughput and gold production stood at between 2.0 Mtpa-2.5 Mtpa, and 100K oz-150K oz, respectively. The target expansion throughput for the year 2020 to 2022 is estimated to be in between 3.5 Mtpa-4.0 Mtpa, whereas the gold production is expected to remain in the range of 150K oz - 200K oz.

Haile Plant Expansion Guidance (Source: Company Reports)

Underground Potential For Macraes: The recent significant intercepts comprise holes i.e. 15.0 metres @ 4.3 g/t gold; 9.0 metres @ 4.6 g/t gold; 9.0 metres @ 3.9 g/t gold; and 6.6 metres @ 4.0 g/t gold. The production at Macraes is expected to be slightly lower on grades while assessing additional mine life extension options.

Macraes Golden Point Drilling (Source: Company Reports)

Mining Rate To Increase At Didipio Underground: The ramp-up of underground is progressing well with 19 Mt plus of ore stockpiled for processing, and mining rate is expected to increase in the year 2019 and beyond. In 2018, mining rate stood at 500 – 600 kt (actual: 627 kt), and in 2019 it is expected to reach 1.2 – 1.3 Mt. It is expected to further increase around 1.6 Mt in the year 2020 and beyond. Moreover, construction of panel two is underway; and potential of additional resources is there at further depths.

What To Expect: The Company expects to generate strong operating cash flows from its portfolio of assets in 2019 and reinvest most of these cash flows to advance its value accretive organic growth opportunities and targeted exploration programs.

The Haile operation demonstrated a significant improvement to production in the month of March as a result of improved weather conditions combined with the implementation of improvement actions to boost mining productivity and reduce resource constraints. The impact of these improvement actions should continue to be seen in the coming quarters.

Didipio production is expected to increase as average grades increase with the continued ramp-up of underground operations. Following receipt of resource consents (permits) for the Martha Underground Project at Waihi, the Company is advancing mine development and management plans and ongoing resource drilling in anticipation of a rapid development approach. At Macraes, the production is expected to be slightly lower on grades while assessing additional mine life extension options remain a focus.

The Company expects production in the second half of 2019 to be stronger than in the first half while costs are expected to be lower.

Production & Cost Guidance (Source: Company Reports)

Gold Outlook: The pressure across the global equities due to uncertainty across interest rate change by various central banks is turning the gold lustre bright and attracting investors to hedge the potential interest rate risk, which in turn is expected to support the gold prices. As per the media reports, China further expanded its gold reserves due to geopolitical tensions, especially the trade tensions between the US and China which could remain high in the coming times. Other countries such as Russia, and Turkey following the sanction concerns are looking for reducing dependencies on the US dollar by increasing bullion in their reserves. These developments have brought optimism among market participants and are expected to boost yellow metal prices in the coming times.

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology:

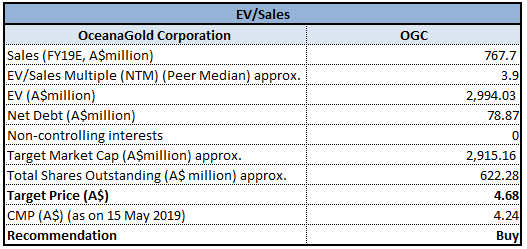

Method 1- EV/Sales Multiple Approach (NTM):

EV/Sales Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

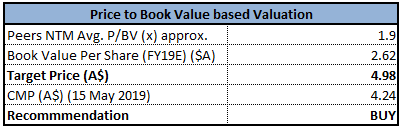

Method 2- Price to Book Value multiple Approach (NTM):

P/BV Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: OceanaGold’s shares generated a positive return of 9.25% in the span of 6 months, while in the span of one-year OGC generated a good return of 20.06%. During the Q1FY19, the Gold production was little better than the previous corresponding period, whereas the copper production in the same period was in-line to the previous corresponding period.

Estimates for M&I resource and inferred resource at various projects sites are promising. Conditions at Haile is expected to improve, and temporary restrictions due to heavy rainfall will be lifted. Improvement plans are underway and are expected to improve productivity this year. Moreover, All-In Sustaining Costs (ASIC) increased in the Q1FY19 due to higher mining costs at Haile, higher group sustaining capital spend combined with lower group gold sales. With the production ramp-up, ASIC is expected to normalize which will lead to an improvement in margins.

Considering the bright prospects of the business over the long term, we have valued the stock using two Relative valuation methods, Price/Book Value ratio and EV/Sales multiple and arrived at a single-digit upside growth in the next 12-18 months.

Hence, considering the aforesaid facts and current trading levels, we recommend a “Buy” rating on the stock at the current market price of A$4.230 per share (down 0.471% on May 15, 2019).

.png)

OGC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...