Kalkine has a fully transformed New Avatar.

Company Overview: OceanaGold Corporation (ASX: OGC) is a high-margin, multinational gold producer with a significant pipeline of organic growth and exploration opportunities in the Americas and Asia-Pacific. OGC’s operating assets include the Waihi Gold Mine and the Macraes Goldfield Mine in New Zealand; the Didipio Gold-Copper Mine in the Philippines; and the Haile Gold Mine in the US. The company is focused on driving operational efficiencies at each of its operations and creating additional value for its shareholders through prudent capital investments in organic growth opportunities and targeted exploration. The company is listed on the ASX and on the Toronto Stock Exchange (TSX) since 27 June 2007..png)

OGC Details

.png)

Consistently Delivered Positive Return on Invested Capital: OceanaGold Corporation (ASX: OGC) is a multinational gold mining and exploration company with a significant pipeline of organic growth and exploration opportunities in the Americas and Asia-Pacific regions. The company’s strategy is to drive operational efficiencies at each of its operations while creating additional value for its shareholders through prudent capital investments in organic growth opportunities and targeted exploration. In the past few years, the company has yielded strong exploration results, including the growth of Mineral Resources at the Martha Underground at Waihi, the Horseshoe Underground at Haile, and the discovery of additional resources at WKP in New Zealand. Over the past ten years, OGC has consistently delivered a positive return on invested capital. From 2015 to 2019, the company’s revenue and gross profit increased at a CAGR of 6.41% and 4.58% respectively. .PNG)

Financial Performance (Source: Company Reports)

Despite the emergence of the COVID-19 pandemic which created additional and varied risks across the company’s global operational footprint, OGC has performed resiliently over the last few months while safeguarding the health and well-being of its people and employees. Amid the current challenging period, the company has maintained its focus on managing the near-term risks while executing on its long-term operational plans. Moving forward, the company remains committed to maintain its consistent track record of profitability from its business. It continues to pursue and review internal and external growth opportunities that would further enhance shareholder’s wealth. The company’s mission is to double the value of its business by 2024.

FY19 Performance Highlights: For the year ended 31 December 2019 or FY19, the company reported consolidated production of 470,601 ounces of gold and 10,255 tonnes of copper with All-in Sustaining Costs (AISC) of US$1,061 per ounce. In the fourth quarter alone, the company reported production of 108,151 ounces of gold, up 20% from the previous quarter with strong production from Haile and Macraes.

For the full year, the company generated US$651.2 million in revenue, down by 16% from 2018, primarily due to lower sales volumes. During the Q4 FY19, the company reported revenue of US$152.1 million, up 14% on Quarter-on-quarter basis, mainly driven by increased sales volume from New Zealand and a higher average gold price received. For the full year, the company reported EBITDA of US$214.2 million.

During the year, the company achieved significant operational progress at its operation sites. At Waihi Gold Mine, the company progressed with the development of the Martha Underground and at Haile Gold Mine, which is located in the US, the company completed the construction of the pre-aeration thickener. At Macraes Goldfield Mine in New Zealand, OGC progressed on the organic growth opportunities, including the Golden Point target and the underground study which is anticipated to finish in H2 FY20..png)

FY19 Results Highlights (Source: Company Reports)

Q1FY20 Highlights: During the first quarter of FY20, the company reported revenue of US$138.2 million with EBITDA of US$42.4 million. For the quarter, the company reported a net loss of US$26.0 million and an adjusted net loss of US$10.7 million, impacted by the lower gold sales from the New Zealand assets and limited sales from Didipio, partly offset by higher sales from Haile. At Hailie, the total material mined in the first quarter increased by 124% on YoY basis, despite the higher than average rainfall during the quarter.

For the quarter, the company reported consolidated gold and silver production of 80,707 ounces and 54,134 ounces, respectively with consolidated AISC of US$1,218 per ounce. Operating cash flows for Q1FY20 stood at US$120.6 million, mainly attributable to US$78.5 million received from the pre-sale of 48koz gold during the quarter. At the end of March quarter, the company’s cash balance stood at US$177.4 million with net debt of US$121.1 million..png)

Production and Cost Results Summary (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 2.84% of the total shareholding. Vanguard Investments Australia Ltd. and Samarang Asset Management S.A. hold maximum interest in the company at 0.94% and 0.71%, respectively..png)

Top 10 Shareholders (Source: Refinitiv, Thomson Reuters)

A Quick look at Key Ratios: For March 2020 quarter, the company’s gross margin stood at 46.5%, higher than the margin of 43.7% reported in the pcp. The company has a current ratio of 1.17x, higher than the industry median of 0.93x, demonstrating that the company is well equipped to pay its short-term obligations. The company has an Assets/Equity ratio of 1.43x, lower than the industry median of 2.64x..png)

Key Metrics (Source: Refinitiv, Thomson Reuters)

Covid-19 Update: Due to the emergence of Covid-19 and strict guidance of government authorities, the company’s several operations were suspended across its different sites. However, the situation has improved since then and the company has fully resumed operations at Macraes and is developing Martha with COVID-19 safeguard measures in place. It is worth noting that despite limited operations at Macraes during the lock-down period, the company has maintained its full-year guidance and is anticipating a significantly stronger operational performance in the H2FY20. At Haile, the operations remained at full capacity with strict measures undertaken to protect the safety and health of its employees and contractors. Till now, the company not been materially impacted by COVID-19 situation, however, the risks associated with the pandemic remain elevated.

Key Risks: The company is exposed to the risks associated with COVID-19 which could significantly impact its operational performance. In order to manage this risk, the company has been strictly enforcing the protocols and safeguards at each of its operations. Further, the company’s properties are subject to the risks inherent in operating in a foreign country.

What to expect: Looking ahead to the remainder of FY20, particularly the second half, the company expects increased consolidated production from its operations with lower All-In Sustaining Costs. At Haile, two-thirds of the annual gold output is expected in the second half with the fourth quarter being the strongest and at Macraes, where production is impacted by the lockdown restrictions, the company is targeting a rebound in the second half of the year.

Till now, the company has maintained its FY20 guidance, as per which, it expects its consolidated gold production to be in between 360,000 and 380,000 ounces with All-In Sustaining Costs ranging from US$1,075 to US$1,125 per ounce sold. The company expects its total capital investment to be between US$220 million to US$255 million. From Haile, the company expects its production to be between 180 – 190koz and from Macreas, it expects the production to be in the range of 160-170koz. From Waihi, the company expects its production to be between 18-20koz..png)

2020 Gold Production Guidance (Source: Company Reports).png)

Key Valuation Metrics (Source: Refinitiv, Thomson Reuters)

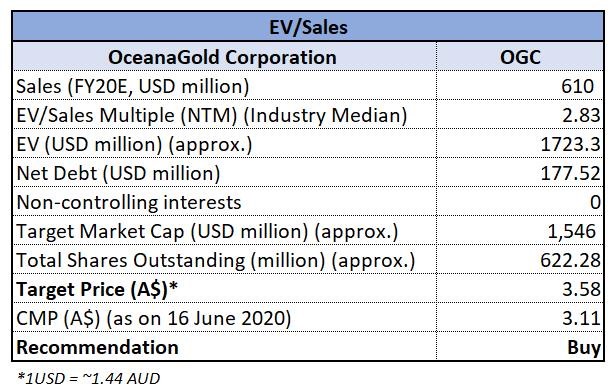

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative)

EV/Sales Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Over the last three months, the stock of OGC has increased by 61.38% on ASX and is currently trading close to its average 52-week trading range. H2FY20 is going to be an important period for the company, as OGC expects production in the second half to deliver two-thirds of the year’s total gold output with lower corresponding AISC. Moving forward, the company remains committed to maintain its consistent track record of profitability from its business. We have valued the stock using an EV to Sales multiple based illustrative relative valuation method and arrived at a target price with an upside of lower double-digit (in percentage terms). For the purpose, we have taken peers like Newcrest Mining Ltd (ASX: NCM), St Barbara Ltd (ASX: SBM) and Saracen Mineral Holdings Ltd (ASX: SAR). Considering the aforesaid facts, FY20 guidance of the company, its resilient performance amid COVID-19, its prudent capital investments in organic growth opportunities, we give a “Buy” recommendation on the stock at the current market price of A$3.110, up by 1.967% on 16 June 2020.

.jpg)

OGC Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...