Kalkine has a fully transformed New Avatar.

Company Overview: ReadyTech Holdings Limited (ASX: RDY) provides SaaS technology, that offers people management software in fields of student management, apprenticeship management and employment services, to a large base of educators, employers, and work transition facilitators. In whole, the company supports customers to adhere to the respective regulatory environments, while better handling and connecting with students and employees, thereby aiding businesses to be ready for the future of education and work. The company reports under two segments namely Education segment and Employment segment. It offers a wide range of products for Education, such as JR Plus, VETtrak, A2E and My Profiling. Whereas, its products for Employment consist of HR3, Aussiepay and ePayroll.

.png)

RDY Details.png)

RDY Rides on High Customer Retention & Higher Investments: ReadyTech Holdings Limited (ASX: RDY) is engaged in providing SaaS-based technology for employers, educators, as well as facilitators of career transitions. The company has a track record of 20 years of organic growth. Notably, the company also has a strong foothold in employment services, which aids job searchers to have appropriate work and adds value across job markets via the integration of social science intelligence. In FY19, the company reported a robust result, which surpassed the FY2019 financial outlook defined in the prospectus. During the period, the company’s pro forma revenue soared 13.5% year over year, and rose 1% ahead of the prospectus estimate. The company’s pro forma EBITDA and NPATA also topped its guided forecasts, depicting the company’s initiatives to remain on track to deliver on future growth prospects. Notably, the company undertook necessary measures and focused mainly to win new customers and add value to existing customers. In order to carry out the above goals, the company is constantly involved in integrating new and innovative technology.

In FY19, RDY company unveiled the Education Products Standard Committee (REPS), which is engaged in promoting the uppermost levels of compliance across its education business, in order to set a goal for this sector into the future. As the need for IT security is increasing with each passing day, ReadyTech is tapping on the opportunity by investing more in the IT security space.

One more factor that contributes towards improving the company’s growth prospects is the cross-sell opportunities that occur from its complementary technology offerings. Presently, the company offers certain leading top skills profiling and behavioural science assessment tools, which are useful for more than 10% of its education customer base.

Coming to 1HFY20, RDY continued its growth path and successfully delivered on its business objectives of securing high-value customers in both education and employment segments, along with added value for the existing customers. During the period, the company continued to invest in R&D, with more than $10 million every year targeted towards product and customer value enhancements. In 1HFY20, the company made investments to assist digital credentials, boosts student services, along with new workflow automation, apps, self-service, and onboarding upgrades in the Employment segment. The company reported higher customer satisfaction rates, with a client revenue retention rate of 95%. In 1HFY20, the company continued to improve its earnings generation abilities and reported a double-digit growth in underlying EBITDA. During the period, cash flow from operating activities amounted to $7.1 million, indicating a conversion of 86% as a percentage of EBITDA. From 1HFY18 to 1HFY20, both cash flow and conversion rate have increased significantly. Consequently, the company has bolstered its financial position to pursue its M&A and partnership strategies.

.png)

Cash Flow (Source: Company Reports)

Going forward, the company will focus on improving customer loyalty by enriching its functions and seeking to build a network of “sticky” customers. The company further expects to promote its offerings in the market, by long lasting customers, consequently leading to growth in business and revenue. The company anticipates several opportunities with the changing nature of the education and employment sectors and is dedicated to being up to date through a forward-thinking approach, to leverage growing opportunities as and when they occur.

1HFY20 Key Financial Results for the Period Ended 31st December 2019: During the period, the company reported pro forma revenue of $19.2 million, soaring 19.9% year over year, owing to robust organic revenue growth from new client wins and cross-selling to existing customer base. Notably, the strong revenue base depicted 16.5% growth in subscription and license revenue, which contributed ~87% of total revenue. Underlying EBITDA for the period increased 35.9% year over year and stood at $8.3 million. Underlying net profit after acquisition amortisation went up a whopping 73.8% and stood at $4.3 million. Average revenue per client increased by 8% to $9.6k. During the period, total expenses came in at $10.9 million, depicting acquisitions impact, continued investment in key sales and technology-related roles along with higher hosting costs driven by client and revenue growth.

.png)

1HFY20 Financial Summary (Source: Company Reports)

Segmental Highlights: Revenue from the education segment increased 11% and came in at $10.7 million. EBITDA for the segment stood at $4.8 million, up 30% from the prior corresponding period. The Employment segment reported revenue of $8.5 million, soaring 35% year over year, whereas EBITDA, including acquisitions, stood at $4.1 million, up 29% on the prior corresponding period.

.png)

Education Segment (Source: Company Reports)

.png)

Employment Segment (Source: Company Reports)

Balance Sheet $ Cash Flow Details: The company exited the period with cash and cash equivalents amounting to $7.1 million and net debt amounting to $20.4 million. The company’s net-debt to pro forma EBITDA ratio stood at 1.4x. Cash provided from operating activities in 1HFY20 stood at $7.1 million, up from $5.5 million in 1HFY19, whereas net cash used in investing activities stood at $9 million.

.png)

Cash Position (Source: Company Reports)

Key Developments: During the period, the company secured a contract with Bendigo TAFE and Kangan Institute in Victoria, for its flagship student management system, JR Plus. Per the contract, the company will offer an early five-year software subscription to the institute worth $7 million. In 1HFY20, the company completed two complementary strategic acquisitions of two workforce management and payroll software and services businesses, namely Zambion and Wagelink. The latest acquisitions provided new customer opportunities in the New Zealand and South Australian markets.

Further, the company has also notified about a new offering, HR3, that is likely to drive future sales across the employment segment.

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form around 42.91% of the total shareholding. Pemba Capital Partners Pty Ltd held the maximum number of shares with a percentage holding of 21.59%, followed by Microequities Asset Management Pty Ltd. holding 5.99%.

.png)

Ten Shareholders (Source: Thomson Reuters)

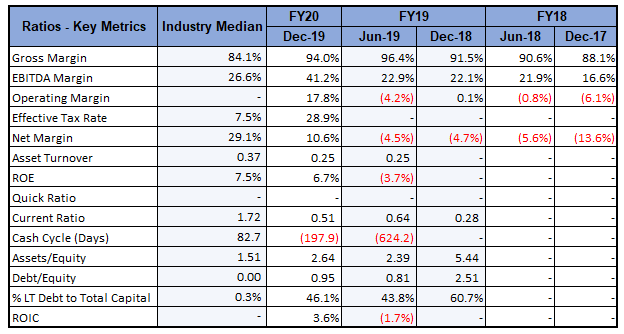

Key Metrics: For the half year ended 31st December 2019, RDY reported gross margin and EBITDA margin of 94% and 41.2%, which is higher than the industry median of 84.1% and 26.6%, respectively, implying decent fundamentals of the company. Net margin of the company stood at 10.6%. Debt to Equity multiple stood at 0.95x, as compared to a multiple of 2.51x in the prior corresponding half.

Key Metrics (Source: Thomson Reuters)

What to Expect: RDY seems to be well-positioned to provide its customers with the best possible solutions and has set a solid footing for future progress in the form of new client wins, acquisitions, product enhancements and talent retention. The Australian tertiary education and training industry signifies noteworthy growth forecasts, portrayed by information and technology expenditure of $1.85 billion in 2020. In FY20, the company anticipates revenue to increase at a rate of ~20%, with an organic revenue growth rate in the early double-digits. Underlying EBITDA margin in FY20 is expected to be ~40%.

To conclude, the COVID-19 led crisis is changing the way people live their life and how they communicate with friends and family. SaaS-based technology companies are playing an enormous role, in assisting organizations to run crucial applications and services. Given the current scenario, during this virus-driven crisis, RDY looks poised to continue its expansion.

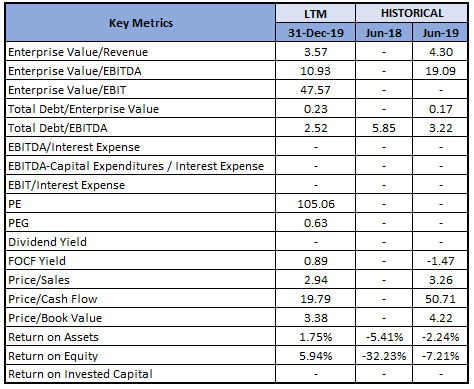

Key Valuation Metrics (Source: Thomson Reuters)

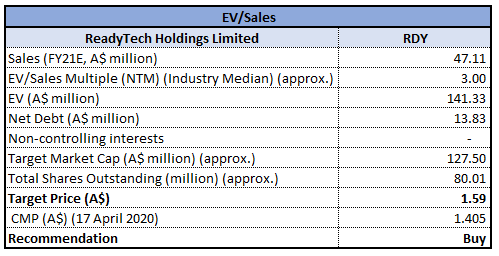

Valuation Methodology: EV/Sales Multiple Based Relative Valuation

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company generated a positive return of 6.4% over a period of one month. Currently, the stock is trading below the average of its 52-week trading range of $0.960 - $2.290. During the first half, the company continued to invest in its growth objectives to drive sales and boost customer retention. The company’s overall business reported a strong half and expects new client wins, acquisitions, a loyal customer base, along with several product enhancements, to shape its performance in FY20 and beyond. We have valued the stock using EV/Sales multiple based illustrative relative valuation method and arrived at a target price with an upside of lower double-digit (in percentage terms). Considering the current trading levels, followed by a strong first half, anticipated benefits from the integration of new businesses and new client wins, we give a “Buy” recommendation on the stock at the current market price of $1.405, up 5.639% on 17 April 2020.

.jpg)

RDY Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...