Kalkine has a fully transformed New Avatar.

Company Overview: Origin Energy Limited (ASX: ORG) is an integrated energy company in Australia involved in the exploration and production of natural gas, wholesale and retail sale of electricity and sale of liquefied natural gas. The company mainly operates two businesses - Energy Markets and Integrated Gas. Origin is the upstream operator and has a 37.5% interest in APLNG which is a significant supplier to both domestic and international LNG markets. The company is focused on connecting its customers to the energy and technologies of the future. Origin strives to be a low-cost operator with a disciplined capital management capability..png)

ORG Details

.png)

Operating Strong Cash Generating Businesses: Origin Energy Limited (ASX: ORG) is an integrated energy company in Australia with a rich heritage in energy exploration, production, power generation and retailing. The company currently operates two strong cash-generating businesses- Energy Markets and Integrated Gas. Further, it owns 37.5% interest in APLNG, a significant supplier to both domestic and international LNG markets, which provides diversification of cash and earnings to ORG. Lately, the company has been striving to become a leaner, simplified organization with a robust risk management framework. During 2015-2019, the company witnessed significant improvement in its underlying EBITDA and underlying ROCE. Over the same period, underlying EBITDA has increased at a CAGR of 20%. .png)

Company Performance (Source: Company Reports)

Amid Covid-19 situation, the extent of the short-term impact on Energy Markets from the virus is not certain, however, the company remains in a resilient financial position, with a sound balance sheet and a competitive cost position to deal with any upcoming uncertainty. Moving forward, the company is considering a range of options which can help in reducing the expenditure and offsetting the impacts of COVID-19 and lower oil prices and it is pursuing other opportunities to deliver on its strategy of improving customer experience, reducing the cost to serve and growing new revenue streams.

FY19 Results Highlights: For the financial year 2019 or FY19, the company reported underlying profit of $1,028 million, an increase from $726 million in FY18. During the year, the company saw strong earnings from its Integrated Gas business, underpinned by cost efficiencies, higher effective oil price and stable production at Australia Pacific LNG.

In the Energy Markets, the company witnessed moderately reduced earnings in electricity, mainly due to the continued impact of heightened retail competition, price relief measures provided to customers, and lower average customer numbers and usage. From Energy Markets, the company reported underlying EBITDA of $1,574 million, down 5% on last year. And from Integrated Gas business, the company reported an underlying EBITDA of $1,892 million, up 51% on last year. For FY19, the company paid a total dividend of 25 cents per share. .png)

FY19 Performance Summary (Source: Company Reports)

H1FY20 Results Highlights: In the first half of FY20, the company saw robust operational performance which generated strong cash flow. Over the period, the company saw a strong performance from Australia Pacific LNG, delivering record production and higher revenue, however, this was offset by the impact of price re-regulation, one-off generation outages and lower electricity volumes in Energy Markets. The company reported an underlying EBITDA of $1,590 million and underlying profit of $528 million in H1FY20.

The strong free cash flow growth over the period, allowing the company to increase the interim dividend to 15 cents per share (fully franked), up 5cps from pcp. .png)

H1FY20 Performance Summary (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 19.21% of the total shareholding. The Vanguard Group, Inc. and AustralianSuper hold maximum interest in the company at 6.02% and 4.87%, respectively.

.png)

Top 10 Shareholders (Source: Refinitiv, Thomson Reuters)

A Quick Look at Key Margins: In H1FY20, the company’s gross margin stood at 18.3%, slightly higher than the pcp. For the same period, the company reported net margin of 8.9%, higher than the industry median of 8%. Further, the company has a Return on Equity (ROE) of 4.5%, higher than the industry median of 3.3%, demonstrating the company’s efficiency in handling shareholders’ money. The company has a quick ratio of 0.91x, higher than the industry median of 0.82x, demonstrating that the company is well equipped to pay its immediate short-term obligations.

.png)

Key Metrics (Source: Refinitiv, Thomson Reuters)

March Quarter Performance: During the March quarter, the company saw some initial impact from the Coronavirus pandemic on electricity demand, which contributed to lower volumes compared to March quarter of 2019. However, Australia Pacific LNG delivered stable and reliable production during the quarter. Further, there was a strong increase in gas sales to the domestic market. During the quarter, the company increased its interest in the Beetaloo Basin to 77.5%, providing greater control over the timing, direction and budgets for future project activity.

Strategic Partnership with Octopus Energy: Origin Energy Limited has recently joined hands with Octopus Energy, fast-growing United Kingdom retailer and emerging technology company, to transform Origin’s retail business by delivering radical improvement in customer experience, a material reduction in costs, and opening up future growth opportunities. ORG intends to acquire a 20% interest in Octopus which will open up new growth opportunities for the company.

Covid-19 Update: As per the update provided on 6 April 2020, the company has not witnessed any material impact on Origin’s energy supply operations and its customers are receiving interrupted and reliable electricity, natural gas and LPG supply. In response to the Covid-19, the company has allowed its workforce to work from home and only roles critical to maintaining energy supply are working from site. The company has also implemented a range of measures to protect its employees and operations and to slow the spread of the virus in the community.

Key Risks: Like several other energy businesses, ORG is also exposed to the risks of Covid-19 which could impact the operations of the business and can reduce the customers’ ability to pay their energy bills, along with energy demand in the small to medium enterprise and business sectors. Further, the company is also exposed to the risk of volatility in the International oil and LNG markets. Although there is a level of uncertainty in the Energy markets, due to the above-mentioned risks, the company’s efforts in the past three years to simplify the business, materially reduce upstream costs at Australia Pacific LNG and significantly decrease the overall debt, has placed it in a financially resilient position.

What to expect: Till now the impacts of Covid-19 have not been material and can be absorbed within the company’s existing FY2020 guidance range. However, the company is closely monitoring the potential impacts of COVID-19. Although the extent of the short-term impact on Energy Markets from Covid-19 is not yet determined, the company remains in a resilient financial position with a sound balance sheet to deal with uncertainties.

In Energy Markets business, the company expects its FY20 underlying EBITDA to be in the range of $1.4 - $1.5 billion, subject to any significant increase in bad and doubtful debt provisioning. From APLNG, the company expects the FY20 cash distributions to be in the range of $1.1 billion - $1.3 billion. In FY20, the company expects its capital expenditure to be 5%-10% lower than previous guidance of $530 million- $580 million. And in FY21, the company expects the capital expenditure to further reduce by 25% – 30% on FY20 previous guidance.

Although the current exploration program in the Beetaloo Basin has been temporarily paused due to COVID-19, the joint venture is targeting a recommencement of Stage 2 activity in H2CY20, with exploration and appraisal activities beyond this program able to be deferred, while ensuring permit obligations are met..png)

Key Financial Metrics (Source: Refinitiv, Thomson Reuters)

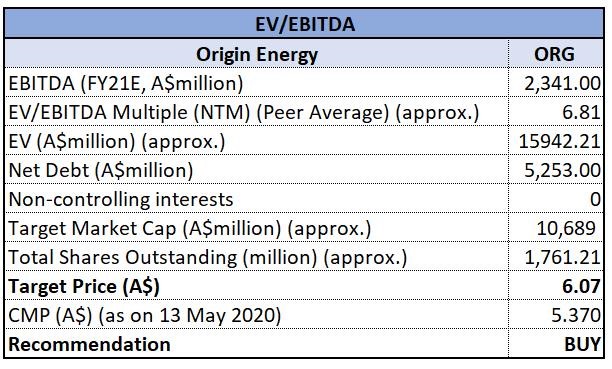

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative)

EV/EBITDA Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: In the past six months, the stock of ORG has declined by 34.9% on ASX and is currently inclined towards its 52 weeks low price, offering investors a decent opportunity for accumulation. The company currently has a robust balance sheet with the liquidity of $3.8 billion (as at 31 December 2019), consisting of $0.8 billion in cash and $3.0 billion in committed undrawn debt facilities expiring over FY2023 and FY2026. The stock has seen a sharp correction due to the fall in oil demand, accompanied by Covid-19 impact on the business activities. Impact of the lower demand in international oil market will remain a key area to closely watch in the coming months. We have valued the stock using EV/EBITDA multiple based illustrative relative valuation method and have arrived at a target price with lower double digit-upside (in % terms). For the purpose, we have taken peers like AGL Energy Ltd (ASX: AGL), APA Group (ASX: APA) and Oil Search Ltd (ASX: OSH), etc. While oil prices are expected to impact the performance going forward (to some extent), considering the company’s resilient financial position, sound balance sheet, competitive cost position, FY20 guidance, and its current trading levels, we give a “Buy” recommendation on the stock at the current market price of $5.370, down 0.371% as on 13 May 2020..jpg)

ORG Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Is Real Estate Investment Regime in New Zealand Maintaining its Resilient Sheen

Introduction

Generally speaking, REITs have been considered to be the leading players in commercial property space in New Zealand. Globally, the industry is known for its resilience and its income-generating capability to counter medium-term and short-term blows, with some support from strong government-led initiatives, financial flexibility, liquidity, and high transparency. In particular, defensive characteristics and growing industrial sector are the backbone of the country’s real estate sector.

Nowadays, global investors are banking upon the country’s real estate market primarily because of decent employment levels as well as robust and sound financial system. As per the Reserve Bank of New Zealand’s Financial Stability Report (November 2014), NZ commercial property stock has been estimated to be worth around $180 billion. Generally, the commercial property is categorised into four submarkets: 1) Accommodation buildings, 2) Industrial space, 3) Office buildings, and 4) Retail.

Key Numbers (Source: Reserve Bank of New Zealand)

With this backdrop, let us look at the relative size of NZ commercial property sub-markets:

Increased Role of Real Estate in New Zealand Economy

Residential property markets are very important for the broader economic growth and for attracting investment from global players, and ‘Housing’ occupies central part of New Zealand’s economy and makes up for around half of the assets of NZ households. Below are some key points in this regard:

History shows us that the house prices have witnessed a strong momentum over time, while volatility keeps on charting out some changes in the trend. As per the report by RBNZ, between 2002 and 2007, house prices were doubled because demand to purchase houses surpassed new supply of houses and residential land on the market. House prices rose relative to rents, incomes and (non-land) construction costs and these prices may remain elevated relative to the fundamental factors for the extended period of time.

House Prices Relative to Fundamentals (indexed) (Source: RBNZ)

Investors’ Access to High Growth Real Estate Market

Owning a house is like an investment which could provide capital appreciation in the long-term subject to 1) Demand and supply factors, 2) Performance of broader economy, 3) Industrial growth, and 4) Interest rates. One form of making investment in real estate is through REITs (or Real Estate Investment Trusts). Key points include the following:

From investment perspective, REITs provide a sustained business model as opposed to capital appreciation model. Capital appreciation will come from rise in rentals and resettling of unit price. It will be for those who want slightly more return than bond yields without taking too much risks. However, the growth of the portfolio will depend on the growth in rentals which will, in turn, depend on the performance of the real estate sector. Affordability, Liquidity, and Stability (less exposure to broad level volatility) set out the chart for REITS, while risks around becoming out of favour or oversupplied, vulnerability to economic downturns, limited growth potential, and steep changes in interest rates are need to be considered to weigh investments in the sector.

COVID-19 and its Impact on REITs

In the wake of COVID-19, the Government realized that there is a great need to ensure that tenancies are sustained, and tenants do not have to face the prospect of homelessness. It was also critical from a public health perspective that people self-isolate in their own homes during the crisis.

Accordingly, on 23 March 2020, the Government announced a freeze to residential rent increase and greater protection to tenants against having their tenancies terminated. The rent increase freeze has been made applicable for an initial period of six months.

The Ministry of Housing and Urban Development confirms that housing and related service providers constitute towards essential services and they need to continue to operate during COVID-19. Like many other sectors, REITs have also suffered from the impact of pandemic. Industry veterans are leaving no stone unturned to minimize the impact and to cushion their financial positions. Some of the leading companies in REIT space have resorted to fund raising which could further strengthen their financial footing.

Most of the companies in REIT space are working to strengthen their balance sheet which could be used to finance the future growth opportunities. Leading banks of New Zealand are also helping the companies in REIT space to dodge the pandemic-led crisis.

Property Market in NZ is Expected to Recover with Some Boost Coming from Initiatives and Settlement of the Wave Emanating from COVID-19

As per the monthly property report released by the Real Estate Institute of New Zealand (or REINZ), median house prices for NZ (excluding Auckland) rose 13.3% to $555,000, a rise from $490,000 in March last year.

In Auckland, median house prices witnessed an increase of 11.1% to the new record median price of $950,000. This is up from $855,000 in same time last year, and an increase of $65,000 as compared to February 2020. March was a buoyant month for the broader residential property throughout New Zealand.

Prior to the spread of coronavirus, the property market of New Zealand was in a robust period of growth that now includes Auckland market, which had 5 consecutive months of YoY growth, after 2 years of price stability.

The effects of coronavirus are still questionable, but impact would be dependent on a number of factors, which include the level of unemployment, business and consumer confidence levels, ability of people to access finance as well as how much time the broader economy takes to recover. However, investors need to be assured that property happens to be a long-term investment while market recovery is on the ‘watch radar.’

New Zealand’s Plan of Action

As per the announcement by the Government official under housing ministry on May 9, 2020, building activities across the country have recommenced with all 300 work sites across New Zealand expected to be up and running again shortly. Another key message as unveiled by the Government is that real estate sector has been put forth to be one of the significant sectors in creating jobs and homes. Construction activity is one of the best investment destinations where one dollar spent is estimated to deliver three dollars in the wider economy.

It is also worth a mention that Kāinga Ora is a significant player in the space, with share of 7% in the country’s residential build market, and residential building accounts for half of all construction in New Zealand. Restart of operations sends strong signal across the industry and encourages to work hard for revival of the economy. Official stats suggest that Kāinga Ora has around 3,000 state, market and affordable homes under construction and contracted, valuing at around $1.5 billion. One third of 300 Kāinga Ora sites are in the Auckland region with another third in the Wellington region. Others are in Christchurch, Hamilton, and spread throughout other locations around the country.

Expectations to meet-up demand for quality homes to counter the increased demand is likely to be strong, and robust initiatives by the Government and better lending policies might support the overall scenario.

Drivers to Boost Real Estate Market Moving Forward

Commercial property market is expected to gain pace with the ease in restrictions along with strong government initiatives to drive the economy back on track. The key occupiers driving office sector growth are from finance, insurance and real estate sectors. Many tenants with non-availability of prime hotspots, opt for traditional leasing. However, the rise in coworking, serviced office space and other variations, with the focus on the small and medium enterprises and start-up sectors, are changing the dynamics of commercial market. Growing risk appetite, strong economic growth, along with ease in credit conditions have earlier led to the surge in commercial property prices.

Now that we have a broader idea of NZ real estate sector, let us now quickly have a look at some stocks in REITs space (APL, GMT, VHP and PFI)

Business Description: Asset Plus Limited (NZX: APL) is a listed commercial property investment company investing solely in New Zealand real estate.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company has received a number of rent relief requests from tenants alongside claims for rental abatement in accordance with lease terms. Given the uncertainty regarding the length of the lockdown and ongoing conditions for the various alert levels, it is unable to currently quantify the impact of the lockdown for the 2021 financial year.

P/BV Based Relative Valuation (Source: Refinitiv (Thomson Reuters)) (Illustrative)

Valuation: The company has conditionally agreed to develop a new office building for Auckland Council at Munroe Lane, Albany, Auckland. As per the release, Auckland Council would be occupying around two thirds of the building. APL has also confirmed that Auckland Council has agreed to extend satisfaction date for the funding as well as shareholder approval condition to July 31, 2020. We have applied P/BV based relative valuation (on an illustrative basis) and the target price reflects a growth of lower double-digit (in % terms).

Business Description: Goodman Property Trust (NZX: GMT) is an externally managed, listed unit trust.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company’s investment strategy has been refined to meet the growing requirement for warehouse and distribution space across Auckland. The city’s industrial property market remains to be New Zealand’s best performing commercial real estate sector led by a strong regional economy. The company is expecting full-year distributions of 6.65 cents per unit.

P/BV Based Relative Valuation (Source: Refinitiv (Thomson Reuters)) (Illustrative)

Valuation: New equity initiatives have also provided greater financial flexibility. The balance sheet capacity this has created will be invested into new opportunities over time. We have P/BV based relative valuation (on an illustrative basis) and the target price reflects a growth of lower double-digit (in % terms).

Business Description: Vital Healthcare Property Trust (NZX: VHP) is an NZX-listed fund that invests in high-quality healthcare-related properties in New Zealand and Australia.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company’s tenants are hospital and healthcare operators who provide a wide range of medical and health services. The company started FY20 with a strong position. The company’s balance sheet has been strengthened by NZ$107 million of additional debt facilities as well as term extensions for near-term debt expiries. These enhancements to VHP’s financial flexibility and liquidity reflect that VHP now has more than NZ$243 million in undrawn debt facilities available from the long-term financiers and no debt expiring before March 2021 while only NZ$128.5 million expiring before September 2021.

P/E Based Relative Valuation (Source: Refinitiv (Thomson Reuters)) (Illustrative)

Valuation: The company stated that hospital operators in Australia (~60% of VHP’s revenue) have either agreed, or are in the process of finalising agreements, with each state government to give facilities as well as services during this pandemic. The operators are expected to recover significant portion of their costs from Australian governments. We have applied P/E based relative valuation (on an illustrative basis) and the target price reflects a growth of lower double-digit (in % terms).

Business Description: Property for Industry Limited (NZX: PFI) is an NZX listed property vehicle specialising in industrial property and its nationwide portfolio of 93 properties valued at over $1.4 billion dollars.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company remains well placed to continue to take advantage of the current low interest rate environment. On 17th March 2020, the New Zealand Government announced the reintroduction of a depreciation deduction for commercial and industrial buildings. The company estimates that this deduction will result in an increase in Funds and Adjusted Funds from Operations (FFO and AFFO) earnings of approximately $1.85 million in FY20. The company has been working closely with its tenants to understand the impact of the COVID-19 virus on their operations.

EV/Sales Based Relative Valuation (Source: Refinitiv (Thomson Reuters)) (Illustrative)

Valuation: The company has recently made an announcement that it has secured a new $50 million liquidity facility from Commonwealth Bank of Australia, New Zealand Branch (or CBA). It stated that new facility is for 18 months and is in addition to bonds as well as syndicated bank facility the company already has in place. We have applied EV/Sales relative valuation method (on an illustrative basis) and have arrived at the target price which reflects a growth of higher single-digit (in % terms).

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...