Company Overview - Origin Energy Limited (Origin) is engaged in the exploration and production of oil and gas, electricity generation, and wholesale and retail sale of electricity and gas. The Company's segments include Energy Markets, Exploration & Production, liquefied natural gas (LNG) and Corporate. Its Energy Markets business is an integrated provider of energy solutions to retail and wholesale markets in Australia and in the Pacific. It has exploration and production interests principally located in eastern and southern Australia, the Browse and Perth basins in Western Australia, the Bonaparte basin in north-western Australia, the Beetaloo basin in Northern Territory and in New Zealand. Its liquefied natural gas segment includes Origin's equity accounted share of Australia Pacific LNG, and also contains its activities and transactions arising from its operatorship of the Australia Pacific LNG upstream activities. Its Corporate segment includes investments in Chile and Indonesia's energy sectors.

.png)

ORG Details

Boosting solar portfolio through PPA with FRV: Origin Energy Ltd (ASX: ORG) is expanding its renewable energy portfolio by entering into purchase agreement with Fotowatio Renewable Ventures (FRV). According to the agreement Origin will purchase 100% output and large scale renewable energy certificate (LREC’s) from FRV’s Clare Solar Farm in north Queensland. The power purchase agreement (PPA) would be for 13 years from the starting of operations till December 2030. FRV would start construction on the 300-hectare site later in 2016, with operations forecasted to begin by 2017. Origin has also secured an option to develop a further 35 MW of capacity.

The deal follows the signing of a 15-year PPA with FRV for the solar power generated by the 56 MW Moree Solar Farm in northern NSW in March and even confirms the group’s commitment to adding more renewable energy into its portfolio. The Clare PPA would enhance Origin’s owned and contracted renewable portfolio to more than 700 MW. This move enables the company to focus on gas-fired generation with owned and contracted renewable energy to meet customer’s demand for cleaner electricity. This deal is a milestone in the transition to the renewables because solar prices have fallen to levels, which the Australian Renewable Energy Agency (ARENA) had targeted for 2020.

.png)

Origin’s energy position (Source: Company Reports)

Positioning to target the booming renewables market: Origin reported that over 14 TWh of new renewables would be required to meet 33 TWh target by 2020 (over 5,000 MW of wind). As a result, the group got development approval for a 106 MW solar farm in Darling Downs in QLD. On the other hand, Origin is short energy while its current generation portfolio has low stranding risk from potential renewables build. Moreover, the volatility from rising renewable penetration would enhance the value of the group’s peaking assets.

.png)

Energy Markets performance (Source: Company Reports)

Ongoing positive drilling results from South Australian Gas Project: Origin has 13.19% stake in South Australian Gas project, while Beach (the operator) has 20.21% of stake in the project. Beach has a five?well development campaign near 50 Km north of the Moomba gas processing facility.

The first well of the campaign, Tirrawarra?93 drilling is faster than estimated. Furthermore, at the Queensland gas project (where Origin has 16.7% stake), the three?well appraisal campaign started in the Durham Downs Complex near 30 kilometres north of the Ballera gas processing plant. This campaign is driven from the earlier identified potential to appraise and develop new reserves within the Toolachee Formation.

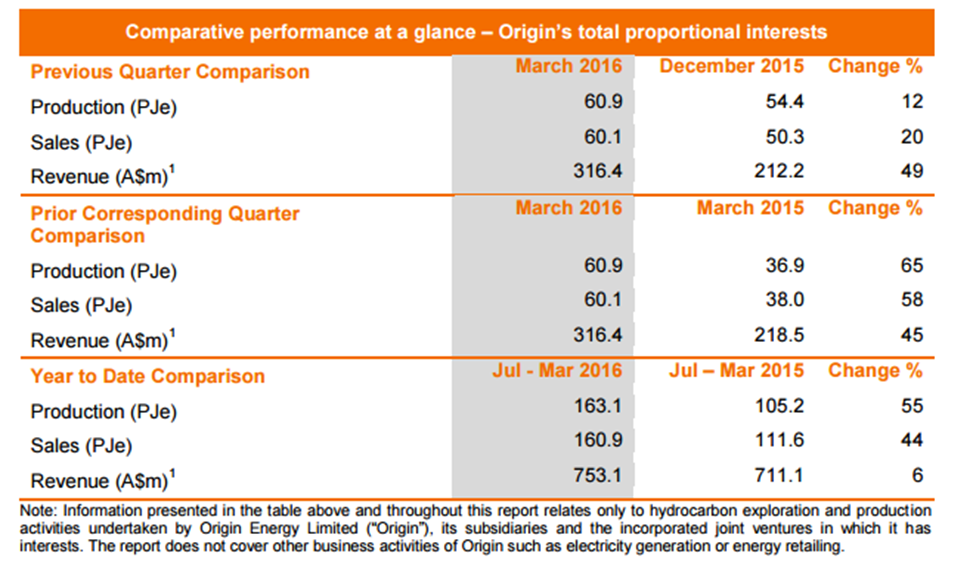

Strong March quarter production: During March 2016 quarter, Origin recorded a gas production of 60.9 PJe, representing a 12% increase against the prior quarter and a 65% increase on the prior corresponding period in FY2015. The performance was primarily driven by rising LNG production by Australia Pacific LNG. As a result, the revenue for the March quarter was at $316.4 million, a 49 % increase against the previous quarter and a 45 % increase as compared to previous corresponding period. The rise is supported primarily due to the commencement of LNG sales by Australia Pacific LNG. Meanwhile, most of the 11 cargoes shipped from Australia Pacific LNG’s Curtis Island facility during the quarter were bought by Sinopec in accordance with the Sale and Purchase Agreement. The project also sent four more cargoes during April further boosting Origin’s performance. APLNG production (100%) delivered a production of 119.4 PJe during the March Quarter, which is a rise by 25% as compared to the December 2015 Quarter (95.5 PJe), driven by the ramp up of LNG production which consumed 49.0 PJe (including liquefaction gas).

Even production from the operated fields rose while ramp gas sales into the domestic market were decreased to meet LNG train demand. Accordingly, the average production from operated assets rose to 917 TJ/d during the March 2016 Quarter as compared to 689 TJ/d during the December 2015 Quarter (APLNG share), on the back of higher rates of production from Combabula/Reedy Creek (69 TJ/d increase), Orana (64 TJ/day increase), Talinga (35 TJ/day increase), Spring Gully (32 TJ/day increase) and Condabri (26 TJ/d increase).

Production highlights (Source: Company Reports)

Enhanced production guidance: Origin reported that its Australia Pacific LNG’s production has exceeded design nameplate capacity of 4.5 million tonnes per annum. First cargo from the second production train is expected during the first half of FY17. Management is also confident of strong operational performance of second train driven by the performance of Train 1.

The Train 1’s production would be accounted from March 2016, and consequently support EBITDA expansion for FY16 from $30 million - $80 million to $100 million to $150 million. Furthermore, the company also expects first gas from the Halladale and Speculant well to start by FY2017. The proposed planned production might start contributing mainly from FY17, further boosting Origin’s sales.

.png)

Halladale / Speculant development on track (Source: Company Reports)

Decrease in debt and boosting capital position: The Company continues to focus on reducing its debt and has targeted net debt below $9 billion in FY17. As a result, the company sold its non-core assets, contact for $3 billion and even boosted its capital position via an entitlement offer of $2.5 billion. The company has targeted operating cost reduction of $100 million and achieved $61 million till date. As per the capital expenditure, the group intends to reduce over $50 million and delivered over $16 million till date.

To conserve the cash, the group has also taken decision to reduce the dividend payout. Moreover, to sustain the volatility in oil prices and currency movement, the company has purchased oil put options for FY17 at oil prices below US$40/bbl. The reduction in debt will help Origin to improve bottom line as higher interest payout weighs on bottom line growth.

Stock performance: The shares of Origin Energy have been consolidating in the last six months but generated outstanding returns of 34.48% (as of May 10, 2016) in the last three months driven by the recovering oil prices coupled with the group’s ongoing positive exploration results, new agreements and solid performance. Meanwhile, Origin has sale agreements for Mortlake terminal station and an Indonesian geothermal project, and is targeting at least $800 million by offloading its non-core assets. The Mortlake terminal station is worth A$110 million with an estimate of a 12.9x FY2017 EBITDA multiple and over $25 million pre-tax gain on sale. The Indonesian geothermal development project is worth US$30 million.

For APLNG project, the group delivered over $1 billion of annual cost reductions and is even aiming to decrease the breakeven by A$3-5/boe. ORG is also making efforts to enhance its operational efficiencies further and even expanding its Electricity margin. The group is able to survive rising competition for Natural Gas while increasing its focus on renewables. The improving shipments from Australia Pacific LNG operation would support the group’s top-line growth while cost cutting strategies and focus on reduction of debt will support bottom-line improvement.We maintain our bullish stance and reiterate our “BUY” recommendation on this dividend yield stock at the current price of $5.08

ORG Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...