Kalkine has a fully transformed New Avatar.

Company Overview: Origin Energy Limited is an integrated energy company. The Company is engaged in exploration, production, generation and the sale of energy to households and businesses across Australia. Its segments include Energy Markets, Integrated Gas, Contact Energy and Corporate. The Company's exploration and production portfolio includes the Bowen, Surat and Cooper/Eromanga basins in Central Australia, the Otway and Bass basins in Southern Australia, as well as interests in the Browse and Perth Basin in Western Australia, and the Bonaparte and Beetaloo Basin in the Northern Territory. It also has exploration projects located in New Zealand in the Taranaki and Canterbury basins, as well as in Vietnam. It jointly owns and wholly operates gas-producing facilities in Australia and New Zealand, including the BassGas and Otway Gas Production plants in Victoria, coal seam gas (CSG) production plants as part of the Australia Pacific LNG Project in Queensland, and the Kupe Gas Project in New Zealand.

.png)

ORG Details

Credit Rating Upgraded to BBB stable / Baa2 stable: Origin Energy Limited (ASX: ORG) has an engagement in the operation of energy businesses including exploration and production of natural gas; electricity generation; wholesale and retail sale of electricity and gas; and sale of liquified natural gas. The company recently published its presentation at Macquarie Conference where ORG highlighted that both of its businesses, i.e., energy markets and integrated gas are generating significant cashflows. Its credit rating has been upgraded to BBB stable and Baa2 stable from BBB- (positive) as per S&P's credit report and Baa3 (positive) as per Moody's credit report, respectively. Its retail segment is a simplified business centred around the customer, and by FY2021 it wishes to reduce its costs over $100 Mn. It is also growing new revenue streams. In its energy supply segment, it aims to develop low cost renewables by targeting additional 530 MW contracted wind online by 2020. It also plans to develop a platform to connect millions of distributed assets. To achieve this, it is developing leading digital and analytical capability, and investing in technology for new customer solutions.

.png)

Chart depicting Free Cash Flow and Net Debt/EBITDA (adj.) (Source: Company Reports)

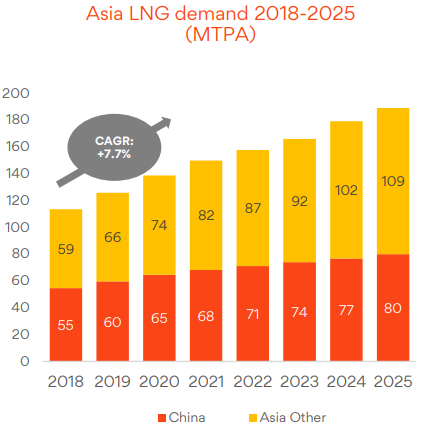

The Company is determined in delivering sustainable and better value to its customer and shareholder. To achieve this, ORG is investing in new revenue streams along with boosting its present technology. In the March’19 quarter, it increased its gas production as compared to the previous corresponding period. Rise in electricity retail sales and a reduction in hedging costs are expected to boost the company’s earnings in the forthcoming year. Moreover, LNG demand is expected to increase dramatically in the Asian region by compounded annual growth rate (CAGR) of 7.7% from 2018-2025, which will help the company to deliver sustainable growth for the long term.

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form around 13.46% of the total shareholding. BlackRock Institutional Trust Company, N.A. and The Vanguard Group, Inc. hold maximum interest in the company at 2.86% and 2.82%, respectively.

.png)

Top 10 Shareholders (Source: Thomson Reuters)

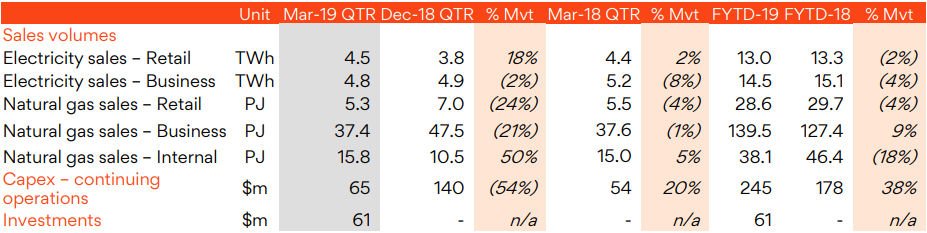

March’19 Quarter- Key Highlights: During the period, in the integrated gas segment, Australia Pacific LNG delivered its highest-ever quarterly revenue of $763.9 Mn (Origin Share), which is an increase of 53% as compared to the March’18 Quarter. Company’s share of production was stable at 63 PJ (petajoules), which can be supported by the fact that a total of 33 LNG (liquified natural gas) cargoes were loaded and shipped from Australia Pacific LNG. In the energy markets segment, electricity sales volumes rose by 7% when compared to the previous quarter, mainly because of higher retail demand over summer, partially offset by the lower Business volumes. The Natural gas sales fell by 10% as compared to the prior quarter, which was because of seasonal demand as well as the ending of short-term wholesale contracts in Queensland. This decline in sales got partly offset by more gas utilised in generation.

.png)

March’19 Quarter Performance (Source: Company Reports)

Total Integrated Gas production in Mar’19 Quarter increased by 1% in pcp: ORG reported LNG production at 834.1kt, which is an increase of 7% as compared to the previous corresponding period. The LNG revenue was reported at $688.8 Mn, which is an increase of 65% as compared to the previous corresponding period. Domestic gas revenue was reported down by 9% at $75.0 Mn as compared to the previous corresponding period.

ORG’s hedging costs were reported at negative of $33.7 Mn, which is an increase of ~53% as compared to the previous corresponding period. However, the hedging cost decreased by ~57% as compared to previous quarter, majorly due to lower oil hedge premium amortisation and smaller LNG hedge position. The company expects that the FY19 total LNG and oil hedging costs are expected to be in between the range of $190 - $210 Mn.

.png)

Total Integrated Gas Production (Source: Company Reports)

Rise in Electricity Retail Sales: Electricity Retail sales in March’19 quarter increased by 18% to 4.5 TWh as compared to the previous quarter. The Gas Retail sales decreased in March’19 Quarter by 24% to 5.3 PJ as compared to the previous quarter, due to lower seasonal demand. The Gas Business Sales in March’19 Quarter decreased by 21% to 37.4 PJ as compared to the previous quarter, due to non-recurrence of short-term wholesale contracts in Queensland (QLD) partly offset by more gas to generation.

Electricity Retail Sales (Source: Company Reports)

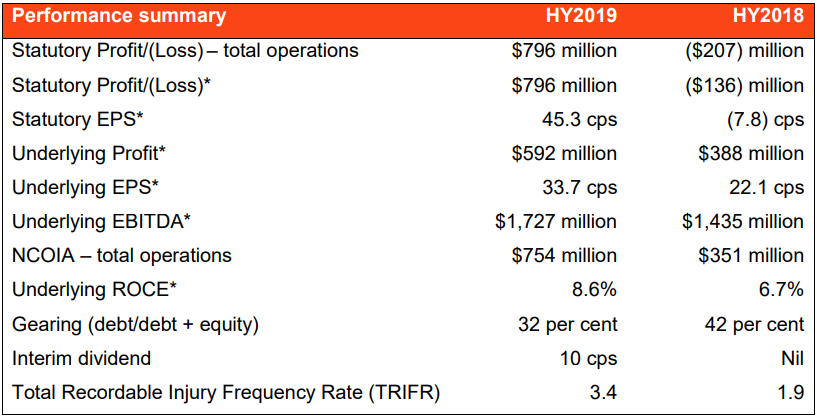

Decent Performance in 1HFY19: Origin Energy Limited reported a statutory profit of $796 Mn in H1FY19 ended on December 31, 2019, as compared to a statutory loss of $136 Mn from continuing operations in H1FY18, which included a significant after-tax impairment charge of $360 Mn. Its underlying earnings before interest, tax, depreciation and amortization (EBITDA) was reported at $1,727 Mn, with an underlying profit of $592 Mn, reflecting reduced financing costs from lower debt & a lower average interest rate and higher oil linked revenues in Integrated Gas.

Performance of Energy Markets segment was reported relatively flat because of an increase in competition in the retail electricity market, combined with the impact of the reduction in electricity prices in order to provide relief to customers. Net cash flow from investing and operating activities increased to $754 Mn, including a $393 Mn net cash distribution from Australia Pacific LNG. The Board of Directors has declared a fully franked interim dividend for H1FY19 of 10 cents per share (cps). As per the company’s management, the debt reduction is on track with adjusted net debt now standing at ~$6 Bn, down by $438 Mn in the half.

H1FY19 Key Metrics (Source: Company Reports)

Underlying EBITDA Growth Witnessed: Growth in energy markets segment improved by 2% to $852 Mn, as compared to the previous corresponding period. This increase can be attributed to the gas portfolio, supported by strong sales to business customers, whereas high levels of competition, customer price relief initiatives and lower electricity usage per customer, impacted the electricity portfolio.

Integrated Gas’ underlying earnings before interest, tax, depreciation and amortization (EBITDA) increased by 43% to $900 Mn as compared to the previous corresponding period. This was because of the rise in the commodity prices, especially oil prices combined with reliable production from the Australia Pacific LNG project, partly offset by the commodity hedging cost.

H1FY19 Operational Performance (Source: Company Reports)

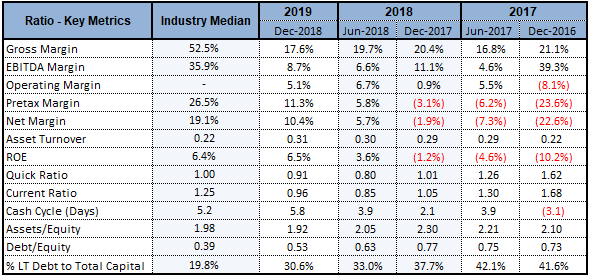

Key Ratios: Its ROE for H1FY19 stands at 6.5%, which is better than the industry median of 6.4%, which implies the company generated a decent return for its shareholders than its peer group.

Key Ratios (Source: Thomson Reuters)

What to expect: As per the report, if market conditions do not materially change, and the regulatory and political environment does not adversely impact operations, then the company expects energy markets guidance to remain unchanged with the underlying earnings before interest, tax, depreciation and amortization (EBITDA) to be in the range of $1.5-$1.6 Bn. The H2 FY2019 is anticipated to be lower as compared to the previous corresponding period, due to the impact of retail competition along with lower customer usage, result of environmental certificate trading gains not repeated ($30 million), and price relief initiatives ($60 million).

Australia Pacific LNG’s guidance is an expected production range of 665 to 685 PJs (petajoules) and 250 to 300 operated wells drilled (100% share). An operating breakeven of USD23 to 26/boe and a distribution breakeven of USD39 to 42/boe, is being targeted by Australia Pacific LNG.

The Capital expenditure (CapEx) after excluding Australia Pacific LNG as well as acquisitions, has been kept unchanged, and is anticipated to be in the range of $385 to $445 Mn. A final dividend (fully franked) of 10 cents per share (or cps) is expected at Full Year 2019 results.

LNG Outlook: LNG demand is expected to increase dramatically in the Asian region by compounded annual growth rate (CAGR) of 7.7% from 2018-2025.

Asia LNG demand stats (Source: Company Reports)

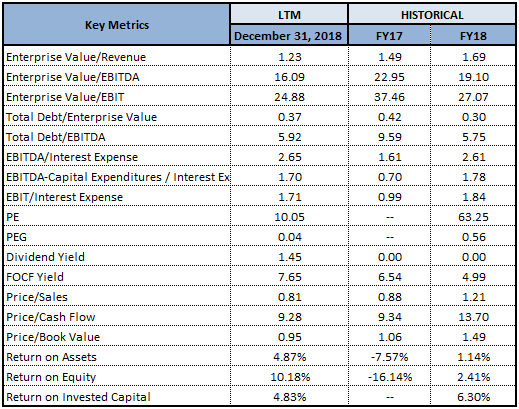

Key Valuation Metrics (Source: Thomson Reuters)

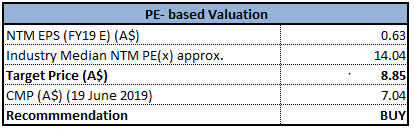

Valuation Methodology: Price to Earnings multiple Approach (NTM):

P/E Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: Origin Energy generated a positive YTD return of 9.34% and is trading close to 52-week low prices of $6.030 with a PE multiple of 9.940x and annual dividend yield of 1.45%, representing a decent opportunity for accumulation. Moreover, the total gas production in the March’19 Quarter increased by 1% as compared to the previous corresponding period. LNG outlook will support the company in its endeavour to increase its sales number along with delivering sustainable returns to its shareholders. In the half year of FY19, ORG delivered a statutory profit of $796 Mn as compared to a statutory loss of $207 Mn in the previous corresponding period, which indicates an improvement in the bottom-line of the company. The company this time also provided an interim dividend of 10 cps to its shareholders as compared to no dividend in the previous corresponding period.

Considering the decent prospects of the business over the long run, we have valued the stock using Relative valuation method, P/E multiple and arrived at a target price of $8.85 (double-digit upside (%)) in the next 12-18 months. Hence, considering the aforesaid facts and current trading levels, we recommend a “Buy” rating on the stock at the current market price of A$7.040 per share (up 1.881% on June 19, 2019).

).png)

ORG Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...