Kalkine has a fully transformed New Avatar.

Company Overview: Origin Energy Limited is an integrated energy company. The Company is engaged in exploration, production, generation and the sale of energy to households and businesses across Australia. Its segments include Energy Markets, Integrated Gas, Contact Energy and Corporate. The Company's exploration and production portfolio includes the Bowen, Surat and Cooper/Eromanga basins in Central Australia, the Otway and Bass basins in Southern Australia, as well as interests in the Browse and Perth Basin in Western Australia, and the Bonaparte and Beetaloo Basin in the Northern Territory. It also has exploration projects located in New Zealand in the Taranaki and Canterbury basins, as well as in Vietnam. It jointly owns and wholly operates gas-producing facilities in Australia and New Zealand, including the BassGas and Otway Gas Production plants in Victoria, coal seam gas (CSG) production plants as part of the Australia Pacific LNG Project in Queensland, and the Kupe Gas Project in New Zealand.

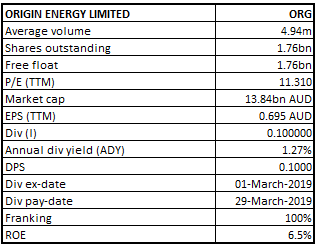

ORG Details

Decent Performance in FY19: Origin Energy Limited (ASX: ORG) has an engagement in the operation of energy businesses including exploration and production of natural gas; electricity generation; wholesale and retail sale of electricity and gas; and sale of liquified natural gas. The company recently released its June ’19 Quarterly report, where it highlighted that its revenue from Australia Pacific LNG increased by 36% in FY19, majorly driven by higher effective commodity prices. The production for Australia Pacific LNG in FY19 was stable, despite a period of significant planned upstream maintenance. The total cash received from Australia Pacific LNG for FY19 was reported at $943 million, higher than the stated guidance of $850 million. The Company is determined in delivering sustainable and better value to its customer and shareholders. To achieve this, ORG is investing in new revenue streams along with boosting its present technology. Its top-line and bottom-line for H1FY19 have shown decent performance as compared to the previous corresponding period. Moreover, upgrade in the credit rating by S&P and Moody, is expected to benefit it in raising funds from the market and institution at the favourable interest rate. Decent LNG outlook in the coming decade will be an icing on the cake for the company’s earnings and expansion programs in the future.

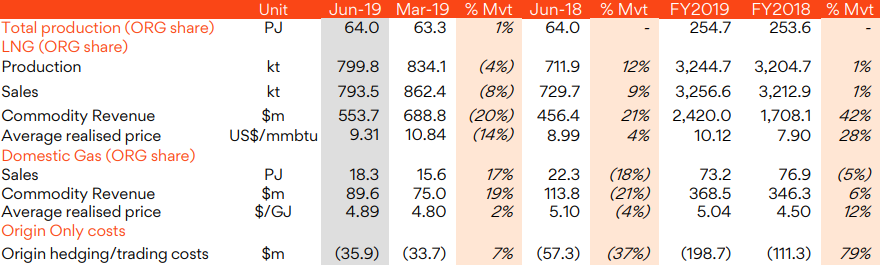

June ’19 Quarter and FY19 Results (Source: Company Reports)

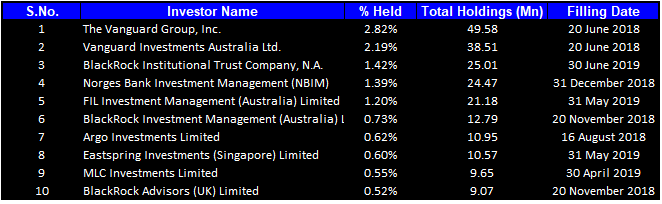

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 12.02% of the total shareholding. The Vanguard Group, Inc. and Vanguard Investments Australia Ltd. hold maximum interest in the company at 2.82% and 2.19%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

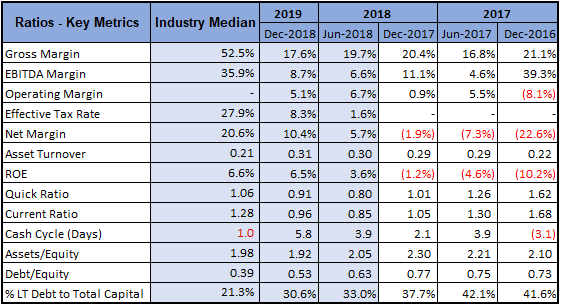

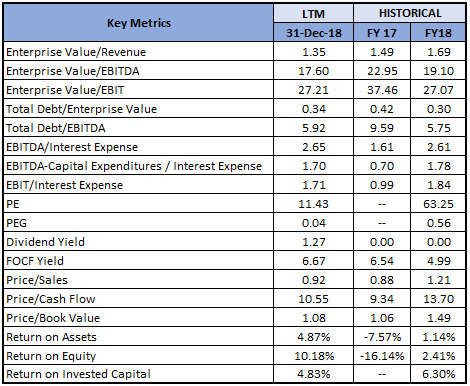

A Quick Look at Key Metrics: Its ROE for H1FY19 stood at 6.5%, which is mildly down as compared to the industry median of 6.6%, which implies that the company generated decent returns for its shareholders. Net margin stood at 10.4% in 1HFY19.

Key Metrics (Source: Thomson Reuters)

Quarterly LNG Gas Revenue Decreased By 16% On PCP: During the June ’19 Quarter, several Australia Pacific LNG gas supply contracts were signed with domestic manufacturing customers, which demonstrates the important role the gas industry plays in supporting local sector. In August 2019, the sale of Ironbark to Australia Pacific LNG is expected to be completed with an estimated amount of $231 million, which will be funded from the Australia Pacific LNG’s retained cash.

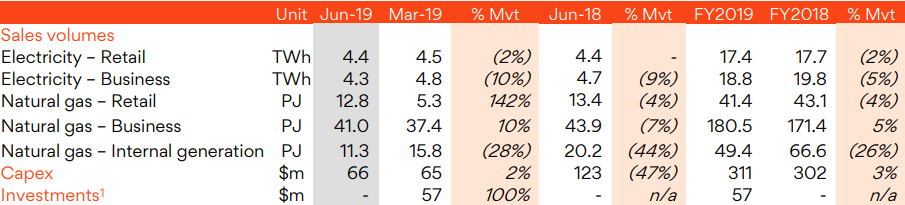

In the Energy markets, electricity sales volumes decreased by 3% to 36.2 TWh in FY19 as compared to 37.5 TWh in FY18, due to lower customer accounts and usage. Natural gas sales volumes decreased by 3% to 271.3 PJ in FY19 as compared to 281.0 PJ in FY18. ORG’s capital expenditure in FY19 was reported at $348 Mn, which is a 6% increase as compared to capex of $328 Mn in FY18, which was slightly lower than the guidance due to the timing of spend.

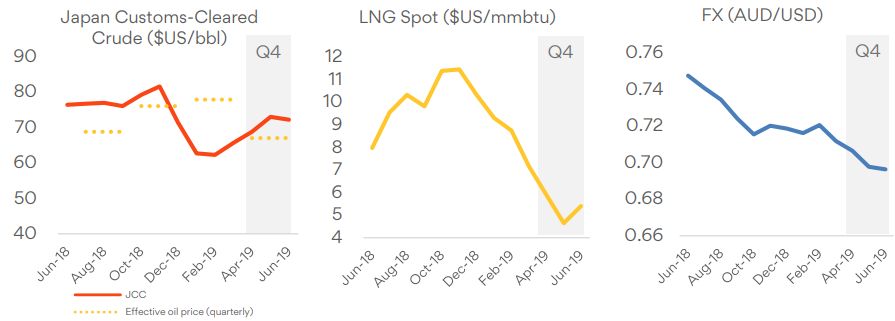

Moreover, Japan Customs-Cleared crude prices recovered in the June ’19 quarter, largely driven by OPEC supply cuts and supply outages in Russia. The Spot LNG prices continued to soften in the June’19 quarter driven by additional supply from new projects and subdued demand growth.

Oil & LNG Markets Data (Source: Company Reports)

Full Year Domestic Gas Revenue Increased By 6%: During the June 2019 quarter, LNG production decreased by 4% to 799.8 kt as compared to 834.1 kt in March ’19 Quarter, which was driven by an increase in gas being directed to the domestic market. Despite planned outages on upstream gas processing facilities in CY19, production for full-year remained stable as compared to the prior year.

LNG revenue decreased by 20% to $553.7 Mn in the June quarter as compared to $688.8 Mn in the previous quarter, due to lower effective oil prices and lower volumes. Domestic gas revenue increased by 19% to $89.6 Mn in the June Quarter as compared to $75.0 Mn in the March quarter. The full-year domestic gas revenue increased by 6% to $368.5 Mn as compared to $346.3 Mn in FY2018, due to higher realised prices (including oil-linked prices). Total FY19 Origin oil and LNG hedging and trading costs equated to $199 Mn, which was in line to the stated guidance.

Integrated Gas Data (Source: Company Reports)

Origin Only Capex Decreased By 50% In June Quarter: During the quarter, Origin Only capex decreased by 50% to $2 Mn as compared to $4 Mn in the March ’19 quarter, and the full-year capex increased by 33% to $11 Mn as compared to $9 Mn in the FY 2018. The exploration and appraisal (E&A) expenditure remained same in both the June and March Quarters at $6 Mn, and for the full year, E&A expenditure increased by 42% to $17 Mn as compared to $12 Mn in the prior period. The Origjn Only capex involves ongoing preparatory work at Beetaloo, and two horizontal appraisal wells planned in CY19, i.e., Kyalla liquids rich gas play and Velkerri liquids rich gas play.

At the Kyalla liquids rich gas play, water extraction licence is in place and the drilling approval is anticipated in August. Moreover, the water bores have been drilled and access road and well pad construction are near to its completion. At the Velkerri liquids rich gas play, water extraction licence is in place, water bore, and access roads have received approval, and well pad civils and drilling are yet to receive approval.

With respect to the APLNG capex, E&A spend in the Jun’19 quarter is primarily related to drilling in Peat and preparation for fracture stimulation and production testing for Burunga South 2. Sustain and Other spend increased by 5% to $1,175 Mn in FY19 as compared to $1,121 Mn in FY18, driven by higher non-operated field development, planned operated infrastructure spend and higher workover spend, which was partly offset by well cost savings and scope changes.

FY19 capex is lower than the given guidance in 1HFY19 results, primarily due to the deferral of activity and reduced scope, i.e., less fracture stimulation as a result of better than expected flow rates in Combabula / Reedy Creek. In another APLNG capex update, ERIC low pressure pipeline from Reedy Creek to Eurombah Creek started in July.

Integrated Gas Capex Data (Source: Company Reports)

Full Year Electricity Retail Decreased By 2%: The Electricity Retail and Business sales decreased by 2% and 10% to 4.4 TWh and 4.3 TWh, respectively, in the June Quarter as compared to 4.5 TWh and 4.8 TWh in the March Quarter, due to seasonal demand. The full year Electricity Retail decreased by 2% to 17.4 TWh as compared to the prior year, due to lower average customer accounts and lower usage.

For the Full year and June ’19 Quarter, Electricity Business volumes decreased by 5% and 9% as compared to the FY18 and June ’18 Quarter, respectively, due to the loss of higher volume customers. Gas Retail volumes declined by 4% on both full-year and Jun’18 primarily due to milder weather and lower usage. Gas Business volumes increased 5% on full year due to new wholesale contracts in Queensland in the first half, and down 7% on Jun-18 due to customer losses. Gas sales to generation decreased by 26% on the prior year and 44% on Jun’18, which was driven by a planned outage at Darling Downs in the final quarter and higher sales to domestic Business customers.

Energy Markets Operations Data (Source: Company Reports)

Key Risks: ORG’s business is exposed to few risks such as increase in competition, technology disruptions, change in demand for energy, regulatory policy and climate change. It is also vulnerable to financial risks such as change in commodity prices, foreign exchange and interest rate risks, liquidity and access to capital markets, etc.

What to expect: On climate change initiatives, ORG would be focusing over growing renewables by targeting additional 530 MW contracted wind online by 2020. It is committed to halve carbon emissions by 2032. In the retail segment, ORG wishes to transform customer experience and reduce cost over $100 Mn by FY2021. It will also focus on growing new revenue streams through centralised energy services and solar, storage and adjacencies. In order to boost future energy, ORG would be developing platforms to connect millions of distributed assets and develop leading digital and analytical capabilities. It would also be investing in technologies for new customer solutions.

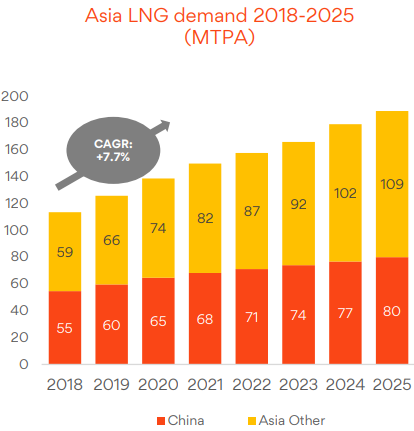

LNG Outlook: LNG demand is expected to increase dramatically in the Asian region by compounded annual growth rate (CAGR) of 7.7% from 2018-2025.

Asia LNG demand 2018-2025 (Source: Company Reports)

Key Valuation Metrics (Source: Thomson Reuters)

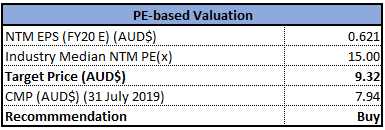

Valuation Methodology 1: Price to Earnings multiple Approach (NTM):

P/E Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

Valuation Methodology 2: EV/EBITDA multiple Approach (NTM):

(5).png)

EV/EBITDA Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: ORG’s stock generated a decent YTD return of 24.37%. The company has performed well on its top-line and bottom-line in the first half of the financial year 2019. Present projects and decent LNG outlook are expected to help the company in delivering a decent return for its shareholders. Moreover, upgrade in its credit rating from S&P and Moody, will help it to raise funds at an attractive rate from the market and institutions.

Looking at the prospects of the company over the long-term, we have valued the stock using two Relative valuation methods, Price/Earnings and EV/EBITDA multiples and have arrived at the target price upside of lower double-digit growth (in %). Hence, considering the aforesaid parameters and current trading levels, we recommend a “Buy” rating on the stock at the current market price of $7.940 per share, up 1.018% on July 31, 2019.

.png)

ORG Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...