Kalkine has a fully transformed New Avatar.

Company Overview: Origin Energy Limited (ASX: ORG) is a leading integrated energy company in Australia which operates through several energy activities, including exploration and production of natural gas, wholesale and retail sale of electricity and gas, electricity generation and sale of liquefied natural gas (LNG). Origin has a 37.5% interest in Australia Pacific LNG which is a significant supplier to both domestic and international LNG markets. The company is focused on providing clean energy and intends to be a low-cost operator with a disciplined capital management capability. Overall, the company’s vision is to move towards a cleaner, smarter and customer-centric energy future..png)

ORG Details

.png)

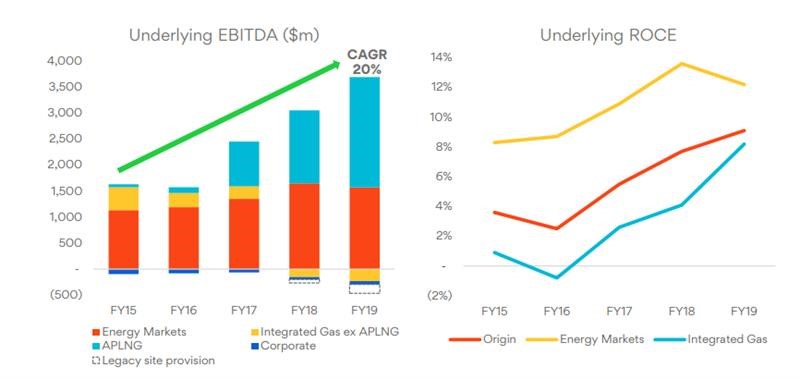

Operates two strong cash generating businesses: Origin Energy Limited (ASX: ORG) is a leading integrated energy company in Australia which is involved in the exploration and production of natural gas, wholesale and retail sale of electricity and sale of liquefied natural gas. As at 01 April 2020, ORG has a market capitalisation of around ~$7.71 billion. The company is focused on providing clean energy and intends to be a low-cost operator with a disciplined capital management capability. The company has two strong cash generating businesses - Energy Markets and Integrated Gas. From 2015 to 2019, the company’s Underlying EPS cents per share (continuing activities) grew at a CAGR of 5.19%. During the same period, the Energy Markets' EBITDA increased at a CAGR of 5.72% while Integrated Gas' EBITDA increased at a CAGR of 39.61%. Overall underlying EBITDA witnessed a CAGR of 20% over the same period.

Past Performance During FY15-FY19 (Source: Thomson Reuters)

The company expects the renewable generation in the National Electricity Market to significantly increase in the coming times. Origin Energy Ltd is working on improving affordability, adding more contracted renewables to its generation capacity, as well as investing to make its generation assets more flexible to support more wind and solar in the market, delivering more gas to domestic customers.

FY19 Key Highlights: In FY19, underlying EBITDA of the integrated gas business increased by $641 million or 51% to $1,892 million. Underlying EBITDA for Energy Markets stood at $1,574 million. Australia Pacific LNG reported strong operational and financial performance in FY19. In the energy market business, the company reported operating cash flow of $1,707 million, up $362 million on FY18.

A Look at Business Performance in H1FY20: During FY19 and in the first half of FY20, the performance of the company’s Integrated Gas business was benefited by the continued reliable production at Australia Pacific LNG. In the Energy Markets business, the company has been witnessing margin pressure with the impact of price re-regulation, as well as lower volumes reflecting reduced energy usage and lower customer numbers. In the first half of FY20, the company reported record production and an increase in profit in Integrated Gas, driven by the continued operational strength of Australia Pacific LNG. The company’s Integrated Gas business reported record production of 358 PJ up 5% on pcp, driven by the improved performance across operated and non-operated fields and commissioning of the ERIC pipeline improved utilisation of processing capacity. For the period, the company reported underlying EBITDA at $1,590 million and underlying profit of $528 million..png)

Half-Year Results Snapshot (Source: Company Reports)

In the company’s Energy Markets business, due to the retail price re-regulation, one-off unplanned generation outages at Mortlake and Eraring and lower electricity volumes, the earnings declined by 15% to $723 million. Over the period, the cost to serve improved by 9%, due to reducing headcount, increasing digitisation, targeted marketing and optimising sales channels.

Strong Cash Flow Generation: In August 2019, the sale of the Ironbark asset to Australia Pacific LNG for $231 million was settled. The contribution from Australia Pacific LNG and proceeds from the sale of Ironbark, as well as good cash conversion in Energy Markets, drove free cash flow to increase by 22% to $680 million in H1FY20. As a result of strong performance, the company increased its fully franked interim dividend to 15 cents per share in H1FY20, up from 10 cents per share in pcp.

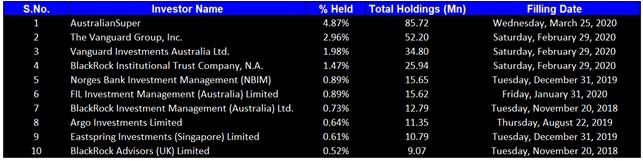

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 15.56%. AustralianSuper and The Vanguard Group, Inc. hold the maximum interest in the company at 4.87% and 2.96%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

Covid-19 Update: As per the media update provided by the company on 24 March 2020, there has been no material impact on the company’s energy supply operations as a result of COVID-19. The company believes that it has responded swiftly in activating business continuity plans in its Integrated Gas and Energy Markets divisions. Origin has implemented various precautionary measures to protect its people who continue to work in roles critical to maintaining energy supply. The company has also assured that it has plenty of fuel including natural gas, coal and LPG. Further, it is planning to minimise any planned maintenance to further mitigate risks to its people and assets.

On 27 March 2020, the company announced new measures to support its customers amid the current Covid-19 pandemic. The company has assured that there will be no disconnections for any residential and small business customers in financial stress until at least 31 July 2020 and there will be no default listing for any customer who is having trouble in paying the bill. Further, the company has paused all late payment fees. For customers who are impacted by COVID-19 the company is offering payment extensions.

Market Outlook: Going Forward, the company expects renewable generation in the National Electricity Market to almost double over 2019 and 2020. This will place downward pressure on average wholesale electricity and renewable certificate prices but will increase the volatility and the need for more reliable, dispatchable capacity such as flexible gas-fired generation which Origin is well placed to supply. The company expects the volatility in global oil and LNG markets to continue with near-term pressure on global LNG prices with significant new US supply expected over 2020–2022. The retail energy markets are expected to remain competitive.

The global crude oil price has tumbled a lot in the past few weeks, due to the increase in the production of Saudi Arabia and Russia. Although Origin Energy is exposed to the volatility in the oil prices, it has already entered into oil hedging instruments to manage its share of APLNG oil price risk based on the primary principle of protecting the Company’s investment grade credit rating. In FY2020, the company’s share of APLNG related JCC oil price exposure is estimated to be around 23 million barrels. Around 11.6 million barrels has been hedged at a floor of US$48/barrel 2.5 million barrel has been capped at US$85/barrel and 3 million bbl has been fixed via a swap at A$97/barrel.

Minimising exposure to the short-term LNG market: The International oil and LNG markets usually have a high degree of volatility. The company currently owns 37.5% interest in Australia Pacific LNG. Last year, 70% of APLNG gas volumes were sold as LNG and the remaining 30% sold domestically via a mix of long-term and short-term contracts. This contracting strategy minimises the company’s exposure to the short-term LNG market.

A Quick Look at Key Ratios: During H1FY20, the company maintained a gross margin of 18.3% which is slightly higher than the pcp. Further, the company has a Return on Equity (ROE) of 4.5% which is higher than the industry median of 4.1%, demonstrating the company’s efficiency in handling shareholders’ money. The company has a quick ratio of 0.91x which is higher than the industry median of 0.78x, demonstrating that the company is well positioned to pay its immediate short-term obligations. .png)

Key Metrics (Source: Thomson Reuters)

What to expect: In the next 3-5 years, Australia Pacific LNG will be focused on maintaining current strong production performance over with potential to increase production further by utilising spare upstream capacity. Beyond APLNG, the company has the opportunity to scale the low-cost operating model to new upstream development opportunities. In the Beetaloo Basin, it has a 70% interest in exploration permits. The Beetaloo exploration project continues to progress, with production testing expected to occur over the last quarter of FY2020 and the first quarter FY2021. Drilling operations on the Kyalla well have been completed and the company is now preparing for the next phase of operations. Origin remains positive about the potential of the lower Kyalla formation, with good results obtained to date. Further, the company is continuing to develop capabilities to test and deploy new connected energy solutions

Guidance for FY20: The company is implementing actions to improve the profitability of its retail business, by enhancing the customer experience, simplifying its processes and growing new revenue streams. The company is targeting to achieve $100 million in savings in its retail business by FY2021. For the financial year 2020, the company expects Energy Markets Underlying EBITDA to be in the range of $1.4-$1.5 billion. For the full year, the production from Australia Pacific LNG is expected to be at the upper end of the previously guided 690-710 PJ range. The production is expected to be underpinned by the improved operated and non-operated field and facility performance. Australia Pacific LNG is expecting total capital expenditure and operating expenditure to be between $2.5-$2.7 billion and a lower distribution breakeven of US$29-32/boe. For the year, Australia Pacific LNG is anticipated to make a cash distribution to Origin of $1.1-$1.3 billion..png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: EV/Sales Multiple Based Relative Valuation.png)

EV/EBITDA Multiple Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock is trading near to its 52 weeks low price of $3.750, offering investors a decent opportunity for accumulation. The company is expecting strong production from Australia Pacific LNG, underpinned by the improved operated and non-operated field and facility performance. To improve its retail business, Origin is enhancing the customer experience and growing new revenue streams. We have valued the stock using an EV/EBITDA Multiple based relative valuation method and arrived at a target price of lower double-digit growth (in % terms). For the said purpose, we have taken peers like AGL Energy Ltd (ASX: AGL), APA Group (ASX: APA) and Woodside Petroleum Ltd (ASX: WPL). Considering the aforesaid facts, H1FY20 performance, balanced outlook, resilient performance amid covid-19 crisis, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $4.60, up 5.023% on 1 April 2020.

.jpg)

ORG Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...