Kalkine has a fully transformed New Avatar.

Company Overview: Over the Wire Holdings Limited is a provider of telecommunications, cloud and information technology solutions. The Company has an integrated product suite of services, including data networks and Internet; voice; cloud and managed services, and data center co-location. It offers custom built, private connections to construct a fully managed wide area network (WAN). It provides power redundant, rack space in its data centers as part of its managed collocation offerings. Its AWS Direct Connect services provide a private connection directly into Amazon Web Services hosted environment. It provides a range of infrastructure as a service (IaaS) options, utilizing virtual machines (VM's), physical machines and utility disk. Its backup as a service (BaaS) is a privately hosted cloud backup system for businesses. Its platform as a service (PaaS) offering allows business to utilize a fully outsourced infrastructure platform for computing needs.

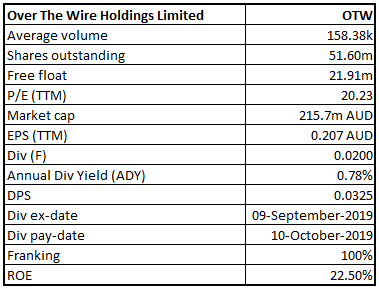

OTW Details

Growth Across all Product Lines: Over the Wire Holdings Limited (ASX: OTW) provides telecommunications, cloud and IT solutions. It has a national network presence with Points of Presence in all major Australian capital cities and Auckland, New Zealand. The company operates four product lines, including Data Networks, Voice, Cloud and Managed Services, and Data Centre Co-location. Looking at the performance over the period over FY15 - FY19, the company witnessed a CAGR growth of 50.9% in top-line with FY15 revenue amounting to $16.15 million and FY19 revenue amounting to $83.71 million. Bottom-line posted a CAGR growth of 50.6% over the same period, with FY15 profit amounting to $1.97 million and FY19 profit amounting to $10.14 million. In FY19, the company improved its profitability by maintaining its gross margin whilst increasing revenue. Moreover, the company managed the operating expenses effectively while simultaneously investing in future growth. Cash position improved during the period on the back of maintenance of expenses as well as cost synergies achieved from acquisitions. The acquisitions of Access Digital Networks Pty Ltd and Comlinx Pty Ltd were a highlight. The acquisitions offered an opportunity to accelerate the expansion of business into existing markets and are expected to offer attractive EBITDA and EPS accretion immediately.

Going forward, the company will continue working on business development and market initiatives. The company is aiming at organic growth through investment in the four product lines, supported by the acquisition of new customers and selling additional products and services to existing customers. Furthermore, the company will leverage its investments in Access Digital and Comlinx to deliver further synergies and is looking forward to growth through acquisitions of suitable businesses that will provide a strategic fit, significant synergies and additional value for shareholders. The company will focus on new customer acquisitions through targeted campaigns focused on industry tailwinds in SD-WAN, Hosted Voice and Cyber Security.

Acquisitions by OTW (Source: Company Reports)

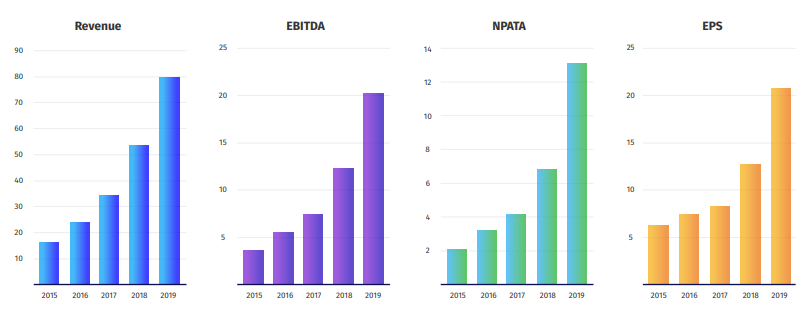

Over the period covering FY15 to FY19, the company has seen a positive trend in all the key metrics, including revenue, EBITDA, NPATA and EPS. Year on Year growth in revenue was the highest in 2019, with record organic growth of $6.9 million.

Key Financials on Rise (Source: Company Reports)

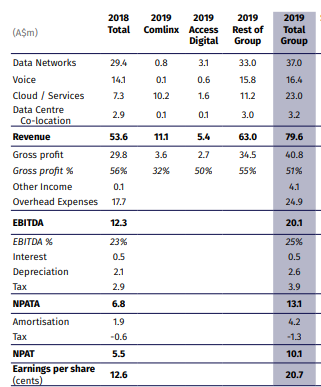

FY19 Financial Highlights: During the year ended 30 June 2019, the company reported revenue amounting to $79.6 million, increasing 49% on prior corresponding year revenue of $53.6 million. EBITDA for the period was reported at $20.1 million, up 64% on prior corresponding year value of $12.3 million. During the year, NPATA amounted to $13.1 million, rising 91% in comparison to the prior corresponding period value of $6.8 million. Earnings per share for the year stood at 20.7 cents, up 64% on pcp EPS of 12.6 cents.

Profit & Loss Statement (Source: Company Reports)

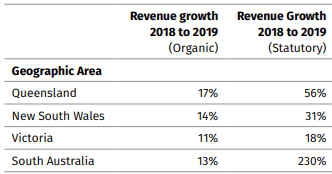

Product Performance: During the year, the company witnessed growth across all product lines. Data Networks revenue increased by 26% to $36,959k. Voice revenue for the year was reported at $16,417k, increasing 17% on pcp. Cloud and Managed Services revenue was reported at $23,028k, representing an increase of 217% on pcp. Revenue in this product line was boosted by organic growth and successful acquisition of Comlinx in November 2018. Data Centre co-location revenue increased by 11% to $3,185k.

Growth in Product Lines (Source: Company Reports)

Cash Flow: During the year, receipts from customers amounted to A$83.2 million, as compared to A$57.8 million in the prior corresponding year. Net cash from operating activities amounted to A$11.4 million, as compared to A$10.3 million in pcp. During the year, the company continued to generate strong conversion of EBITDA to cash. In October 2018, the company raised $25 million in cash for funding the acquisition of Comlinx and Access Digital. Sound management of overhead expenses in the underlying business, cost synergies in the acquired entities, maintenance of net debtor days metrics and revenue growth of 49%, collectively generated growth in EBITDA and positive cash from operating activities during the year.

Strong Balance Sheet Position: Balance Sheet at the end of FY19 depicted a strong position to deliver the next strategic acquisition. Net debt at the end of the period was less than $1 million. Debt to EBITDA ratio for the year stood at 0.5:1. Non-current borrowings for FY19 stood at $6.5 million, as compared to $9.2 million in prior corresponding period.

Dividend: The company recently released an announcement regarding a dividend of AUD 0.0200 per ordinary share. The shareholders will receive the dividend on 10 October 2019.

Acquisition of Access Digital: In November 2018, the company acquired 100% shares in Access Digital. The acquisition involved payment of total consideration of $13.05 million. Out of the total payment, $10.44 million was paid in cash and the remaining amount was paid via 567,393 OTW shares at an issue price of $4.60 per share. Access Digital added approximately 250 business customers to OTW’s network and accelerated its geographical expansion in South Australia. For the 12 months period to 30 June 2018, Access Digital had revenue of $8.5 million and EBITDA of $2.9 million. The business is now expected to contribute significantly to OTW’s financial results in the future.

Acquisition of Comlinx: Another acquisition completed in November 2018 was of Comlinx that included payment of total upfront consideration of $16.0 million, partly in cash and OTW shares. $12.80 million was paid in cash and the remaining via issue of 695,655 shares at an issue price of $4.60. This acquisition provided with 100 additional business customers to the company and accelerated its move into the provision of Software Defined WAN solutions. The company will see a significant contribution coming in from the acquisition, with Comlinx’s revenue and EBITDA for the 12 months period ended 30 June 2018 amounting to $16.10 million and $3.20 million, respectively.

Going forward, the company is aiming to achieve organic growth through continued geographic expansion and market penetration. It is planning on leveraging its strong customer relationships and high customer retention to provide a broader range of products and services. Moreover, the company is looking forward to new customer acquisitions to achieve significant synergies in business operations.

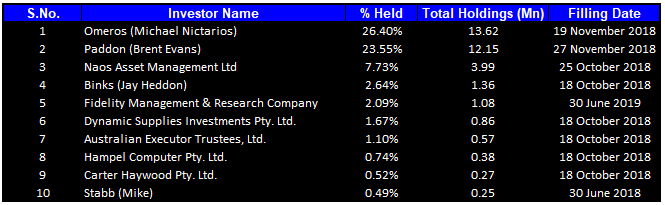

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 66.93% of the total shareholding. Omeros (Michael Nictarios) holds the maximum interest in the company at 26.40%, followed by Paddon (Brent Evans) holding 23.55% of the shares.

Top Ten Shareholders (Source: Thomson Reuters)

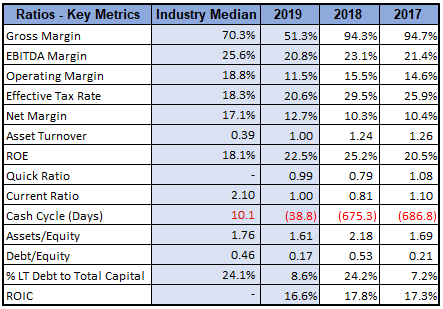

Key Metrics: In FY19, the company had a net margin of 12.7%, which is higher than the net margin of 10.3% in the prior corresponding year. Current ratio of the company increased from 0.81x in FY18 to 1.00x in FY19, that depicts an increase in the company’s capability to cater to its short-term obligations. Debt/Equity ratio also decreased in comparison to the prior corresponding period, representing a decent financial position. Furthermore, the company’s FY19 debt/equity ratio of 0.17x is less than the industry median of 0.46x.

Key Metrics (Source: Thomson Reuters)

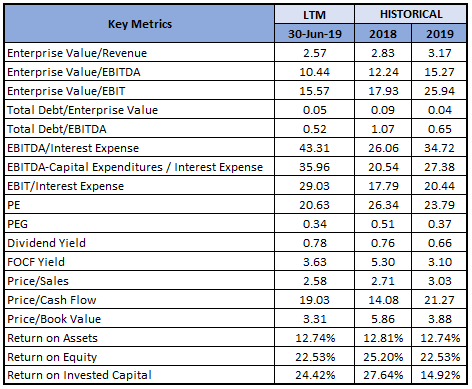

Outlook: In FY20, the company is expected to target more than 15% organic growth in revenue. The targeted growth will be a factor of expansion of geographical footprints and deeper penetration into the market. The company has also planned the geographical expansion of Comlinx business in FY20. The company will diversify its offerings to extend a broader range of products and services for building strong customer relationships and maintaining high customer retention. Moreover, it is also eyeing acquisitions that will add value to the business and provide significant synergies for boosting shareholder value. It is looking forward to new customer wins through SD-WAN capability and leveraging its solution partners for broader Cyber Security offering.

Key Valuation Metrics (Source: Thomson Reuters)

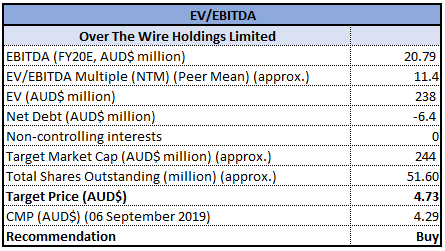

Valuation Methodologies:

Method 1: EV/EBITDA Multiple Approach:

EV/EBITDA Multiple Valuation (Source: Thomson Reuters)

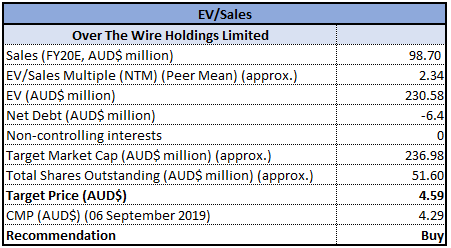

Method 2: EV/Sales Multiple Approach:

EV/Sales Multiple Approach (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The stock of the company generated negative returns of 6.49% and 13.81% over a period of 1 month and 3 months, respectively. In FY19, the company reported the highest YoY organic growth of $6.9 million in revenue. EBITDA margin in FY19 was reported at 25%, as compared to 23% in the prior corresponding period. Balance sheet for the year remained strong with cash and cash equivalents of $10.3 million, as compared to $7.0 million in pcp. The company witnessed growth across all the product lines with cloud/services reporting the highest organic growth of 52%. During the year, the company’s customer service led to high levels of customer retention at 96%, which will allow the company to further win customers from its competitors and expand the services provided. Considering the above factors, we have valued the stock using two relative valuation methods, i.e., EV/EBITDA multiple approach and EV/Sales multiple approach and have arrived at the target price in the ambit of $4.59 to $4.73 (high single-digit to low double-digit growth (in %)). Hence, we recommend a “Buy” rating on the stock at the current market price of $4.290, up 2.632% on 06 September 2019.

.png)

OTW Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...