Kalkine has a fully transformed New Avatar.

Company Overview: Ramelius Resources Limited is engaged in exploration, mine development, mine operations, the sale of gold and milling services. The Company's segments include Mt Magnet, Burbanks and Exploration. The Company's operational projects include Mt Magnet Mine, Kathleen Valley Mine and Vivien Mine. Its development projects include Blackmans and Water Tank Hill. Its exploration projects include Milkyway, Boorgardie Basin and Tanami Joint Venture Gold Project. The Mt Magnet gold project is located adjacent to the town of Mt Magnet, approximately 500 kilometers north-east of Perth in the Murchison Goldfield of the Western Australian Yilgarn Craton. The Blackmans gold project is located approximately 30 kilometers north of Mt Magnet, in Western Australia. The Water Tank Hill project lies over 1.5 kilometers west of Mt Magnet, in Western Australia. The Milkyway gold project is located approximately 3.6 kilometers southwest of the processing plant at Mt Magnet, Western Australia.

.png)

RMS Details

Achieved Production Guidance for June ’19 Quarter and FY19: Ramelius Resources Limited (ASX: RMS) has an engagement in exploration, mine development, mine operations along with the production and sale of gold. The company has achieved its stated production guidance for both June’19 quarter and Full Year period. Its June ’19 Quarter production was reported at 47,342 oz Au, which was within the stated guidance of 45,000 – 50,000 oz Au. RMS’ cash and gold balance at the end of the June quarter stood at $106.8 Mn, after considering significant capital and exploration expenditure of $28.2 Mn during the quarter.

The Company has substantial cash on balance sheet along with excellent gold balance at the end of the quarter period along with the current ratio of 3.41x. Recent geo-political circumstances are expected to boost gold prices for the forthcoming year, which will help Gold companies to lift their top and bottom-line. Considering the material business risks and production guidance for FY2020, it is expected that the company will deliver the sustainable value for its shareholders from the medium to long time frame.

.png)

Corporate Summary (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form around 26.75% of the total shareholding. Ruffer LLP and Van Eck Associates Corporation hold maximum interest in the company at 7.66% and 5.53%, respectively. Recently Van Eck Associates Corporation and the associates, changed its voting power in the company from 6.54% to 5.53%, effective from July 9, 2019.

.png)

Top 10 Shareholders (Source: Thomson Reuters)

A Quick Look at Key Metrics: Its current ratio for H1FY19 stood at 3.41x, better than the industry median of 1.88x, which implies that the company is in a better position to address its short-term obligations than its peer group. Its debt to equity ratio for H1FY19 indicates that company is debt free, and it utilizes its own funds to fuel its operations.

.png)

Key Metrics (Source: Thomson Reuters)

Key Highlights of June’19 Quarter: The Quarterly production of 47,342 ounces Au comprised of 18,913 ounces, 11,757 ounces and 16,672 ounces from the site Mt Magnet, Vivien and Edna May, respectively. Production from Mt Magnet increased by 19% as compared to the prior Quarter with higher grade feed becoming available from the open pit mines as well as ore from the high-grade Hill 60 underground. Significant progress was made in the establishment and pre-stripping of the Eridanus open pit with ore mining to commence early in the FY20 financial year. Vivien production was comparable to the prior Quarter as mining continued in higher grade stoping areas and progress of the Edna May underground continued with development ore being processed during the Quarter. Stoping activities are scheduled to begin early in the September 2019 Quarter. Strategic review for Tampia Hill was completed during the quarter which confirmed the haulage option to the Edna May mill as the most economical decision.

Moreover, for the first time, RMS outlined a comprehensive 5-year Life of Mine Plan that provides clarity around production and costs moving forward whilst still allowing for upside from organic growth and the potential acquisition of new projects.

During the quarter, RMS continued the progress across mining, development and exploration with the following accomplishments:

♦ It commenced mining at Eridanus open pit of Mt Magnet

♦ Submitted Greenfinch (Edna May) open pit revised Clearing Permit application

♦ Commenced decline development at the Shannon underground mine of Mt Magnet, following the establishment of surface infrastructure and the portal

♦ Processed first development ore from the Hill 60 underground mine of Mt Magnet

♦ Released new Resource/Reserve estimates for the Marda and Tampia development projects

♦ Processed first development ore from the Edna May underground mine

♦ Tampia project strategic review confirmed the decision to process ore through the Edna May processing facility

Cash & Gold Balance improved from the previous quarter: RMS’ cash and gold balance improved from $104.7 Mn in March ’19 Quarter to $106.8 Mn in June ’19 Quarter. The present balance would be crucial for the company in fuelling its capital investments for the future development of the Ramelius asset portfolio including $4.9 Mn on exploration and $23.3M in asset acquisition and project development costs. The asset acquisition costs will include $0.5 Mn for final cash component of Explaurum Ltd acquisition, whereas the project development costs would involve costs for Shannon & Hill 60 of Mt Magnet undergrounds, Eridanus open pit of Mt Magnet, Edna May underground and Marda resource definition & project studies at $7.1 Mn, $10.2 Mn, $4.3 Mn and $1.2 Mn, respectively.

At the end of June ’19 Quarter, forward gold sales consisted of 240,900 ounces at an average price of A$1,834/oz over the period to August 2021. During the period, contracts for 31,500 ounces at A$1,732/oz were delivered, and the company entered into new contracts of 69,150 ounces at A$1,914/oz.

H1FY19 (ended on December 31, 2019) Performance Highlights: Sales Revenue for the half-year period was reported at $181.9 Mn, which is a 26% increase as compared to $144.8 Mn in H1FY18. It comprised sales revenue contribution of $100.5 Mn and $81.4 Mn from sites Mt Magnet and Edna May, respectively. The main driver behind this has been the acquisition of Edna May with a full six months of operations being included in the half-year compared to only three months for the prior corresponding period (Edna May was acquired on 3 October 2017). The cash costs of production for the period increased by 33% on pcp to $109.4 Mn in H1FY19. Earnings before interest and tax (EBIT) for the half-year period was reported at $7.3 Mn as compared to $21.3 Mn in the previous corresponding period. Major reasons for the decline were:

(a) Lower grades at Mt Magnet (namely from the Milky Way open pit and Water Tank Hill underground mine) as operations focussed on opening up new ore sources

(b) Increased grades and production at Edna May.

(c) Higher realised gold prices.

(d) Lower grades at Vivien as ore was predominantly sourced from strike ends of the lode.

(e) Increased operating costs on a per tonne basis at Edna May as the mine progressed to its final depth.

The profit from continuing operations for the half-year period was reported at $4.8 Mn as compared to $13.6 Mn in H1FY18.

.png)

H1FY19 Income Statement (Source: Company Reports)

Risk Analysis: The Company remains susceptible to various risks such as:

(a) Fluctuations in the United States Dollar spot gold price and AUD/USD exchange rate.

(b) Government Regulations, new laws, rules and regulations on land use and water use, land claims, taxes, etc.

(c) Operating risks and hazards involved in the exploration, development and production of gold. Other risks involve equipment failure, toxic chemical leakages, loss of power, fast-moving heavy equipment, failure of tailings disposal pipelines and retaining dams around tailings containment areas, rain and seismic events which may result in the environmental pollution and consequent liability.

What to expect: As per the company reports, financial year 2020 production estimates have been kept at 205-225,000 oz, which is well above the production result of the financial year 2019.

In its landmark 5-year life of mine plan, key production centres will continue to deliver mine life extensions. The company anticipates keeping life at or greater than 5 years via exploration and acquisition. It expects production to be in excess of 1,000,000 oz over 5 years, with high subjectivity to Ore reserves and clarity over the exploration, production and development costs.

.png)

RMS’ Production Target for next 5 years (Source: Company Reports)

Strategic review for Tampia site confirms Ore haulage to Edna May mill, and the development is expected to commence in FY21. Marda development is expected to commence in FY20. The average All-In Sustaining costs between the FY2020 till FY2023 is expected to be in the range of $1,220-1,320 per oz. The average capital cost from FY2020 to FY2023 is expected to be in the range of $230-280 Mn. The average production from FY2020 to FY2023 is expected to be around 1,084,500 oz.

.png)

5-Year Mine Plan (Source: Company Reports)

Gold Outlook: Gold spot price (XAU/USD) at the time of writing was noted at the price of US$1413.80 on July 16, 2019. It has breached an important resistance level on a weekly timeframe chart at US$1,366.73, which indicates a higher probability for a fresh new upside rally. The main reason for this rise can be attributed to uncertainty arising due to geo-political tensions and prompting a shift of the global investment towards safe asset class such as gold. As per the media reports, the US-Iran tensions are rising in the Gulf reason. Iran recently broke 300 Kg cap on enriched Uranium stockpile along with shooting down the US drone, leading to a war like situation. The present circumstance is expected to affect global oil supplies, leading to a decrease in the global growth rate forecast. Moreover, market sentiments also turned positive towards gold investments when US Fed Chairman, Jay Powell said that they will act appropriately to deal with the current situation, which gave a hint for a rate cut to boost slowing business investments.

Gold Spot Price (XAU/USD) on July 16, 2019 (Source: Thomson Reuters)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: PE Multiple Approach (NTM):

PE Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

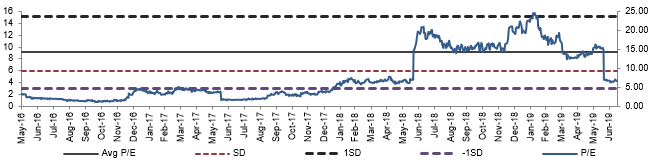

Historical PE Band (Source: Company Reports, Thomson Reuters)

Stock Recommendation: Ramelius’ stock generated an excellent return of 48.11% in the span of 6 months, while in the span of one-year, RMS generated a decent return of 38.94%. The company achieved its production guidance for both June ’19 Quarter and financial year 2019. Its production guidance for FY2020 has been estimated above the production result of FY2019. Strong cash and gold position on the balance sheet, well progressive projects, decent outlook, and a comprehensive 5-year Life of Mine Plan augur well for the organic growth of the company. Looking at the bright prospects of the company over the long-term, we have valued the stock using a Relative valuation method, Price/Earnings multiple and four-year average P/E market multiples of 9.0x for FY20E with consensus EPS of $0.090 and have arrived at target price upside of lower double-digit growth (in %). Hence, considering the aforesaid parameters and current trading levels, we recommend a “Buy” rating on the stock at the current market price of $0.735 per share, down 1.342% on July 16, 2019.

.png)

RMS Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...