Kalkine has a fully transformed New Avatar.

Company Overview: Regis Resources Limited is a gold production and exploration company. The Company is principally engaged in the production of gold from the Duketon Gold Project; exploration, evaluation and development of gold projects in the Eastern Goldfields of Western Australia, and exploration and evaluation of the McPhillamys Gold Project in New South Wales. It has two business segments, which comprise the Duketon Gold Project, being Duketon North Operations (DNO) consisting of Moolart Well, and Duketon South Operations (DSO), incorporating Garden Well and Rosemont. Its portfolio projects include Duketon Gold Project and McPhillamys Gold Project. Its Duketon Gold Project is located in the North Eastern Goldfields of Western Australia approximately 130 kilometers north of Laverton. Its McPhillamys Gold Project is located approximately 35 kilometers southeast of the town of Orange and approximately 30 kilometers west of the town of Bathurst in the Central West region of New South Wales, Australia.

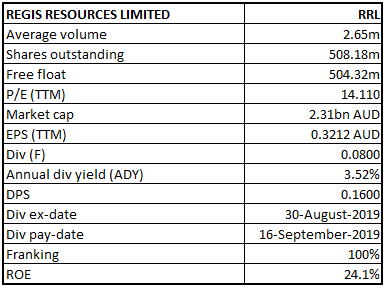

RRL Details

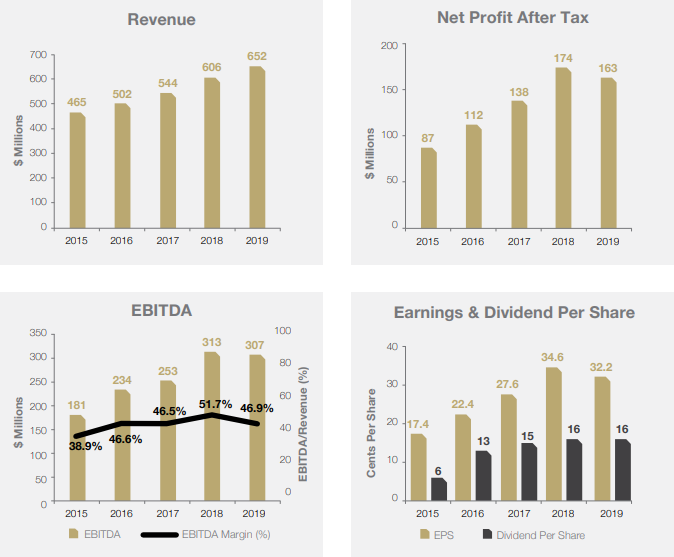

Top-Line and Bottom-Line CAGR Growth of 8.92% and 17.06% for FY15-19: Regis Resources Limited (ASX: RRL) is involved in the production of gold from the Duketon Gold Project; exploration, evaluation and development of gold projects in the Eastern Goldfields of Western Australia; and exploration and evaluation of the McPhillamys Gold project in New South Wales. Looking at the past performance over FY15 to FY19, total revenue and net income of the company have grown with a CAGR (compounded annual growth rate) of 8.92% and 17.06%, respectively. Group’s total revenue improved from $465.3 Mn in FY15 to $654.8 Mn in FY19, and net income improved from $86.9 Mn in FY15 to $163.2 Mn in FY19. Company’s revenue and net profit after tax for FY19 were commendable, where growth in revenue can be attributed to increased gold production and a higher realised gold price, offset by increased costs, primarily due to increased strip ratios and industry-wide cost pressures.

The group aims to continue to optimize mining and processing operations across the Duketon Gold project whilst maintaining a high standard of safety. It is determined to organically increase the reserve base of the group by discovering and developing satellite resource positions, extending the reserve base of existing operating deposits. Moreover, it is advancing the economic study of the McPhillamys Gold Project in NSW with a view to develop a significant long-life gold mine at the project.

RRL is determined to continue its investment in growth through significant exploration expenditure and capital investment as well as an active but disciplined business development effort. Outlook for the Australian dollar gold price is positive which is likely to help the company in further enhancing its earnings and to deliver sustainable value to its shareholders. FY20 production guidance range of 340,000-370,000 oz at an AISC range of $1,125-$1,195/oz, indicates the confidence of the company in its mine expansion projects.

RRL’s Financial Performance over FY15-FY19 (Source: Company Reports)

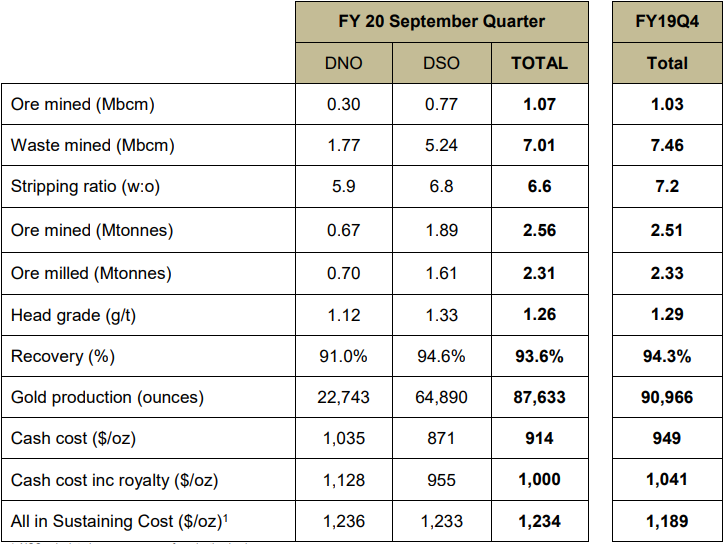

September’19 Quarter Key Highlights: Gold production for the quarter stood at 87,633 oz as compared to 90,966 oz in the previous quarter. Pre-royalty cash cost (CC) for the quarter stood at $914/oz and All-In Sustaining Cost of $1,234/oz as compared to CC of $949/oz and AISC of $1,189/oz in the previous quarter. The decrease in cash cost was driven by a greater proportion of costs associated with new satellite pits being classified as capital in the September quarter. On the other hand, an increase in AISC was largely driven by a temporary reduction in grade due to short term valuations in the mine schedule; and the reduction in mill throughput impacted by an unplanned maintenance shutdown at Garden Well.

Production of gold at Duketon Northern Operations (DNO) for the quarter increased to 22,743 ounces at AISC of $1,236 per ounce. The small increase in AISC can be attributed to the winding down of the growth capital phase and a subsequent transition to sustaining capital. Gold production at Duketon Southern Operations (DSO) for the quarter decreased by 8% to 64,890 ounces on Q-o-Q, at an AISC of $1,233 per ounce. The decrease in production at DSO was due to lower throughput, driven by an unplanned maintenance shutdown of the Garden Well mill for around 6 days.

September’19 Quarter Key Operating Metrics (Source: Company Reports)

Cash & Bullion Balance Stood at $147.4 Mn as on September 30, 2019: Cash flow from operations for the quarter stood at $82.5 Mn as compared to $85.2 Mn in the previous quarter. Cash and bullion as on September 30, 2019 was reported at $147.4 Mn as compared to $205.3 Mn in the previous quarter. The cash outflow included payment of $40.7 Mn in dividends, $20 Mn to triple the company’s landholdings in the Duketon Greenstone Belt, $30.6 Mn in capitalised mining costs, $10.1 Mn on exploration and feasibility projects, $13.3 Mn in income tax payments and $5.7 Mn on land acquisitions in NSW.

September’19 Quarter Cash Flow Metrics (Source: Company Reports)

Gold Hedging: Total hedging position at the end of September quarter was reported at 438,510 ounces of gold with an average delivery price of $1,615 per ounce as compared to 451,514 ounces of gold with an average delivery price of $1,611 per ounce at the end of June quarter. In order to reduce the exposure to around 200,000 ounces of its lowest priced hedges, the company is delivering into these hedges at a rate of at least 10,000 ounces per quarter. The continuation of this approach will be subject to the prevailing gold price, company’s cash balances and capital requirements.

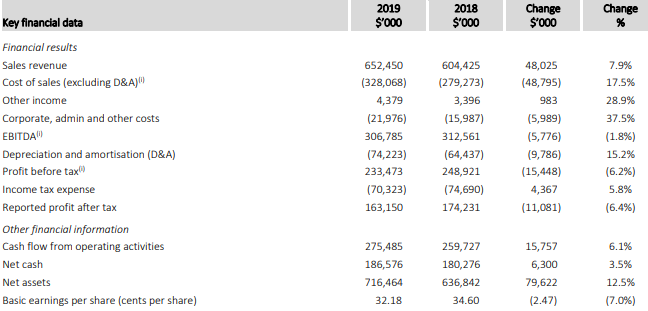

FY19 Key Financial Highlights for the period ended June 30, 2019: Revenue for the period was reported at $654.8 Mn, with the sale of 369,721 ounces of gold at an average price of $1,765 per ounce. Gold production for the period stood at 363,418 ounces at an all-in sustaining cost (AISC) of $1,029 per ounce. EBITDA for the period was reported at $306.8 Mn. Net profit after tax for the period was reported at $163.1 Mn. Cash flows from operating activities for the period was reported at $275.5 Mn. At the year-end, the Company had a net cash and bullion position of $205.3 Mn and a total hedging position of 451,514 ounces of spot deferred contracts with an average delivery price of $1,611 per ounce. The company had zero debt at the end of the year.

The Board of Directors declared a fully franked final dividend of 8 cents per share, taking the full-year fully franked dividend of 16 cents per share for FY19. The record and payment dates were on September 2, 2019 and September 16, 2019, respectively.

FY19 Key Financial Metrics (Source: Company Reports)

Recent Updates:

On November 19, 2019, the company announced the appointment of Mrs Lynda Burnett as an independent Non-Executive Director of the Company, effective November 27, 2019. Mrs Burnett has an impressive track record as a geologist and brings additional experience as a director of ASX-listed mining companies. Currently, Mrs Burnett is the Managing Director of ASX listed explorer Sipa Resources (ASX: SRI) since July 2014.

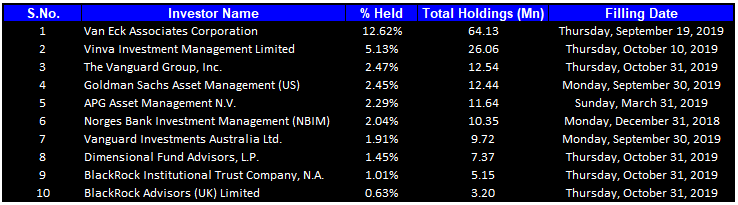

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 31.99% of the total shareholding. Van Eck Associates Corporation and Vinva Investment Management Limited hold maximum interests in the company at 12.62% and 5.13%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

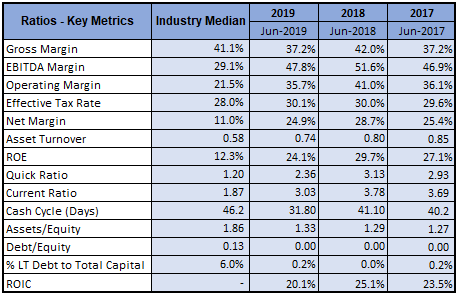

A Quick Look at Key Metrics: Its EBITDA margin and net margin for FY19 stood at 47.8% and 24.9%, better than the industry median of 29.1% and 11.0%, respectively, implying the company’s decent fundamentals. Its current ratio for FY19 stood at 3.03x, better than the industry median of 1.87x, implying that the company is in a better position to address its short-term obligations. Its long-term debt to total capital for FY19 stood at 0.2%, lower than the industry median of 6.0%.

Key Metrics (Source: Thomson Reuters)

Key Risks: The company is susceptible to certain financial risks such as credit risk, liquidity risk and market risk (including foreign currency risk, interest rate risk and commodity price risk).

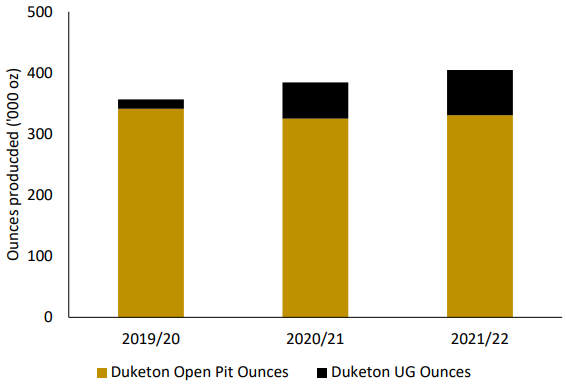

What to Expect: Commencement of production at the Rosemont underground is expected to provide desired results for the company. With the increase in high-grade material from the Rosemont underground, gold production over the next 3 years is expected to lift by around 10% above the current level to ~400,000 ounces by FY2022. Beyond this timeframe, the production profile will be impacted largely by the timing of McPhillamys, additional underground production, for example, Garden Well, exploration success, reserves depletion and business development initiatives.

The group has kept its full-year guidance unchanged for FY20 with a production range of 340,000 - 370,000 oz at an AISC range of $1,125-$1,195/oz, with an assumption of $0.70 exchange rate, diesel prices as on June 30, 2019 and gold price of $1,750/oz.

Indicative 3-year Gold production profile from the Duketon operation (Source: Company Reports)

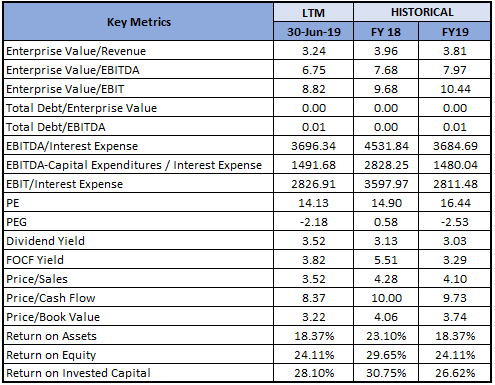

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

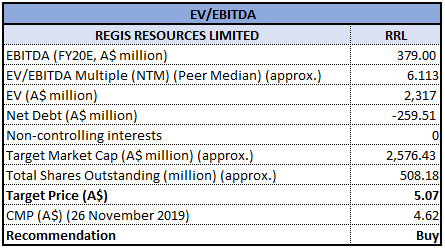

Method 1: Enterprise Value to EBITDA Multiple Approach:

EV/EBITDA Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

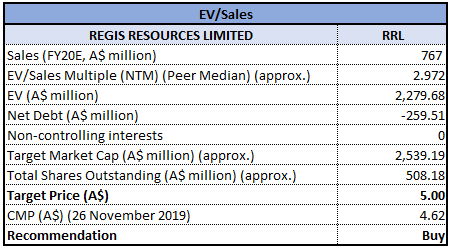

Method 2: Enterprise Value (EV) to Sales Multiple Approach:

EV to Sales Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The stock posted a negative YTD return of 4.42%, whereas in the past one year, the stock has gained 5.09%. Currently, the stock is trading towards its 52-week low level of $4.030, proffering an opportunity for accumulation. Company’s robust performance has allowed it to deploy significant capital towards the development of new and existing satellite ore sources for future growth. Its strategy can be underpinned by the on-schedule development of the Rosemont underground and significant progress towards McPhillamys Project in NSW. Moreover, its September quarter results were satisfactory. FY19 top-line grew at a decent rate due to increased gold production. It stands at a net cash position along with decent profitability margins for FY19, combined with a positive outlook with the expectations that the company will continue to fuel its operation and look for leverage options in the future in case of an aggressive expansion program. Looking at the business prospects over the long-term, we have valued the stock using two relative valuation methods, i.e., EV to EBITDA and EV to Sales Multiples, and arrived at a target price of higher single-digit growth (in % term) Hence, we give a “Buy” recommendation on the stock at the current market price of A$4.620 per share, up 1.762% on November 26, 2019.

.jpg)

RRL Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...