Kalkine has a fully transformed New Avatar.

Company Overview: Resolute Mining Limited is engaged in gold mining, and prospecting and exploration for minerals. The Company operates through three segments: Ravenswood, Syama and Bibiani. It operates over two mines, the Syama gold mine in Africa and the Ravenswood gold mine in Australia. The Syama gold mine is approximately 30 kilometers from the Cote d'Ivoire border and over 300 kilometers southeast of the capital Bamako. The Ravenswood gold mine is approximately 95 kilometers south-west of Townsville and over 60 kilometers east of Charters Towers in north-east Queensland. Its key development focus is in Mali. It has a portfolio of open pit oxide resources located in various satellite pits to the north and south of the main Syama pit. In Ghana, it owns over 90% underground Bibiani Gold Project. It is exploring over 10,800 square kilometers of prospective tenure across two continents and holds Birimian age greenstone tenure in West Africa, with tenements across Mali, Ghana and Cote d'Ivoire.

.png)

RSG Details

Higher Capex in-line with Revised Production and Cost Guidance: Resolute Mining Limited (ASX: RSG) is a successful gold miner with more than 30 years of experience as an explorer, developer, and operator of gold mines in Australia and Africa which have produced more than 8 million ounces of gold. It currently owns gold mines, namely, the Syama Gold mine in Mali, the Ravenswood Gold mine in Australia, the Bibiani Gold mine in Ghana, and the Mako Gold mine in Senegal.

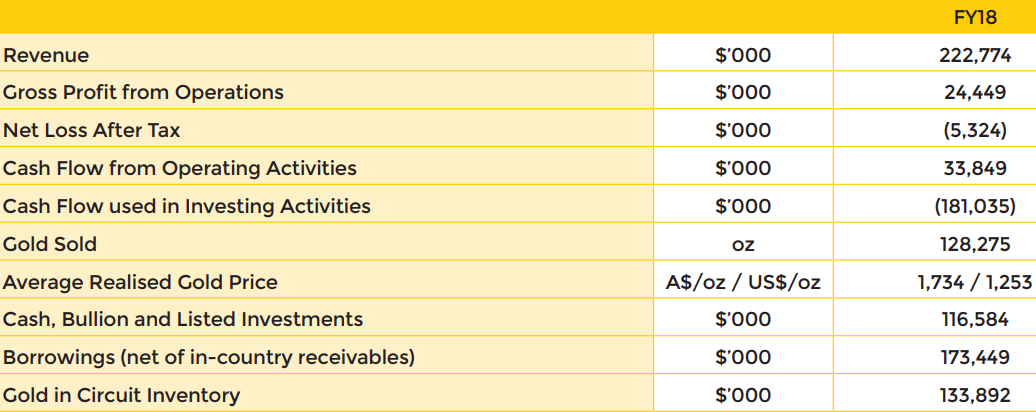

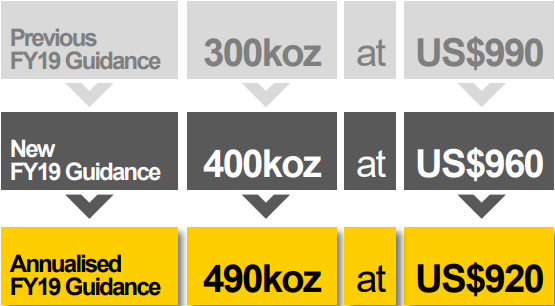

As per the annual report for FY18 (for the period of July 1, 2018 to December 31, 2018), the gold production stood at 129,199 oz at the All-In Sustaining Costs of $1,449 per oz. The company generated a revenue of $223 Mn from gold sales of 128,275 ounces at an average realised price of $1,734 per oz, which was close to the average gold spot price over the period at $1,690 per oz. The gross profit from operations was reported at $24 Mn after depreciation and amortization (related to gold sales) of $10 Mn. RSG reported a net loss after tax of $5 Mn, which was inclusive of an adverse movement in the valuation of net realisable inventory of $29 Mn offset by $15.5 Mn of unrealised foreign exchange gain on intercompany loans. The company continued to invest heavily in the business during the period with Capital Expenditures on development, property, plant and equipment totalling $175 Mn and exploration and evaluation expenditure of $10 Mn. Another achievement of the company was to bring down the total recordable injury frequency rate to 1.98 as on December 31, 2018 from 3.30 as at 30 June 2018. As per the recent update, the company has revised upward its annualised FY19 production guidance by 48.5% to 490 koz at All-In Sustaining cost of US$920 per oz as compared to the previous guidance of 330,000 oz at All-In Sustaining cost of US$990/oz. The company posted excellent quarterly numbers and is in the process to meet its objective of being a low-cost, multi-mine African-focused gold producer. The current projects and developments, enhancing portfolio opportunities, etc., augur well for the future growth of the company.

.png)

FY2018 Production Metrics (Source: Company Reports)

Decent Cash Reserves as at 31 December 2018: The Company continues to generate positive operating cash flows while making significant investments across its portfolio. The investing cash outflows were reported at $181 Mn. Its cash, bullion and listed investments at the end of the period were reported at $117 Mn, where cash balance stood at $39 Mn, 22,786 oz of gold valued at $40 Mn and investments valued at $38 Mn. The company made several strategic investments in multiple African-focused gold explorers such as Orca Gold Limited (16%), Loncor Resources Inc (27%), Kilo Goldmines Limited (27%), Manas Gold Limited (23%) and Oklo Resources Limited (10%).

FY18 Key Financial Metrics (Source: Company Reports)

RSG’s Hedging Strategy: In order to take advantage of gold price volatility, maximise revenues and protect the company’s balance sheet and cash flows, Resolute Mining Limited undertook to hedge above its budgeted gold price. On December 31, 2018, the company’s hedge book comprised 115,000 oz committed to monthly deliveries out to December 2019 made up of 85,000 oz forward sold at prices between $1,715 per oz and $1,760 per oz, and 30,000 oz forward sold at US$1,250 per oz.

On August 8, 2019, the company has forward sold an additional 30,000 ounces of gold at an average price of US$1,519 per ounce in scheduled monthly deliveries of 5,000 ounces between January 2020 and June 2020. Recently, RSG took advantage of gold price strength to extend the company’s US dollar denominated gold hedge position. The major objective behind the move was to secure price certainty for a portion of the US dollar revenues generated from the company’s African gold mines. RSG’s total gold hedge book consisted of 190,000 ounces in monthly deliveries out to June 2020 representing less than 3% of its Ore Reserves.

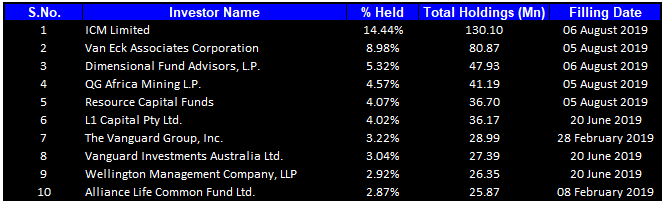

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 53.46% of the total shareholding. ICM Limited and Van Eck Associates Corporation hold maximum interest in the company at 14.44% and 8.98%, respectively. In a recent update, RSG and its related bodies reduced its interest in the Mako Gold Limited from voting power of 19.45% to 17.0%, effective from August 13, 2019.

Top 10 Shareholders (Source: Thomson Reuters)

June ’19 Quarter Key Highlights: The company’s 12-months gold production was reported at 305,436 oz, which exceeded the guidance of 300,000 oz. The All-In Sustaining costs for the 12-months period was reported at US$924 per oz, which was lower than the guidance of US$960 per oz. Gold production for the June quarter stood at 78,132 oz at an AISC of US$939 per oz.

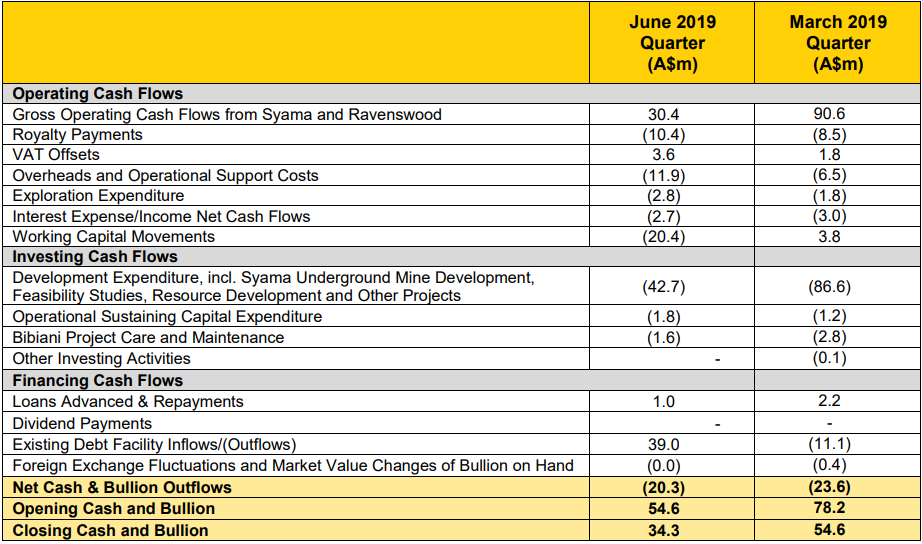

Syama sulphide circuit quarterly production stood at 22,532 oz, which is 69% up from the March quarter. The average gold price received for June 2019 Quarter was reported at US$1,274/oz from gold sales of 68,900 oz. The Ravenswood expansion study demonstrated the potential to deliver 200,000 oz annually for 15 years. The Tabakoroni mineral resource was confirmed with 1Moz at 5.1g/t Au. The cash, bullion and listed investments as on June 30, 2019 was reported at $56 Mn. The Gold in circuit inventory on as June 30, 2019 was reported at 66,917 oz worth an additional $134 Mn.

The Company’s Total Recordable Injury Frequency Rate as on June 30, 2019 was reported at 2.77 as compared to 2.01 on March 31, 2019.

RSG Cash and Bullion Balance Data (Source: Company Reports)

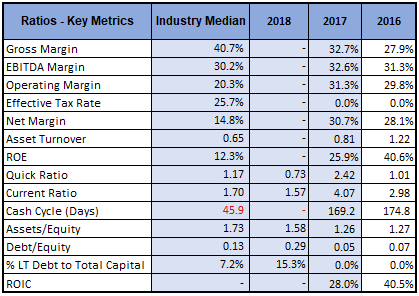

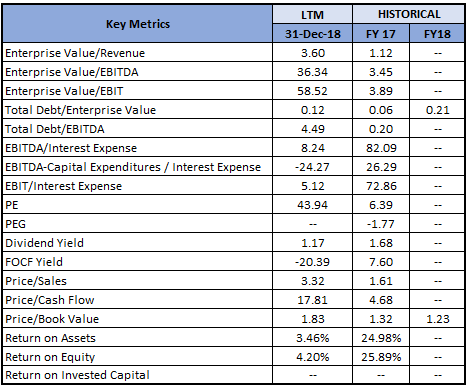

A Quick Look at Key Metrics: Its current ratio for FY18 stood at 1.57x, close to the industry median of 1.70x, which implies the company is in a better position to address its short-term obligations.

Key Metrics (Source: Thomson Reuters)

Key Risks: The company is vulnerable to certain risks such as changes to commodity prices, cash flow and credit risk, fraud and corruption, risks associated with projects across diverse jurisdictions and operating environments.

Changes in Accounting Period: The Group has changed its financial year end from 30 June to 31 December, as a part of the process of seeking a listing on the London Stock Exchange (LSE), and to synchronise the consolidation of Resolute’s African subsidiary companies’ accounts. The financial period for Resolute Mining is now a 12-month financial year, commencing on 1 January and ending on 31 December.

What to expect: Earlier FY19 production guidance for the company was estimated at 330,000 oz at All-In Sustaining cost of US$990/oz. As per the release, the new annualised FY19 production guidance for the company has been estimated at 490 koz at All-In Sustaining cost of US$920 per oz.

FY19 Production Guidance Metrics (Source: Company Reports)

Outlook for Syama: The company is highly focused on implementing fully autonomous fleet and the continued ramp-up of the Syama underground mine. It is expected that the production rates will increase in the September 2019 Quarter as additional stoping areas are brought online. During the September 2019 Quarter, work at the Syama Underground Mine will comprise Ore development on the 1080 and 1055 production sub levels; commencement of sub level caving on the 1080 level; ongoing sublevel caving production from 1130 and 1105 transverse zones; ongoing mapping and commissioning of automated loading from sublevel cave draw points; and commissioning of automated trucking.

Mining at the Tabakoroni Open Pit Mine is expected to be completed in the September 2019 Quarter, and the processed grades are likely to be lower than in the June 2019 Quarter as mining moves through though lower grades zones in these pits.

Gold production from Syama for FY19 is expected to be 270,000oz at US$890/oz with sulphide operations contributing 110,000oz and oxide operations contributing 160,000oz. The capital expenditure (non-sustaining) for Syama is for the six months ended December 2019 and has been forecasted at $57 Mn, which comprises capital for the completion of the Syama Underground Mine including final equipment, automation and remaining infrastructure works. Investment in exploration at Syama has been forecasted at $11 Mn for the six months to December 2019.

Outlook for Ravenswood: Production in Ravenswood Gold Mine is expected to improve in the September 2019 Quarter as a result of increased mill availability and improved production from the Mt Wright Underground Mine. The company is considering options for increasing mill throughput further, including re-commissioning of the currently inactive third ball mill. Gold production from Ravenswood in FY19 is expected to be 60,000oz at an AISC of US$1,270/oz. Project capital expenditure for the six months to December 2019 at Ravenswood as the Company prepares for the development of the Ravenswood Expansion Project (REP) has been forecasted at $10 Mn.

Gold Outlook: Gold Spot (XAU/USD) at the time of writing was trading at US$1,495.08 (on August 20, 2019, 14:50 (UTC+10)). It recently broke an important resistance level at ~US$1,366 on the weekly timeframe chart, since then the gold has risen by ~9.4%. As the geopolitical tensions are yet to stabilise, gold is expected to see more investments pouring in the coming times.

Key Valuation Metrics (Source: Thomson Reuters)

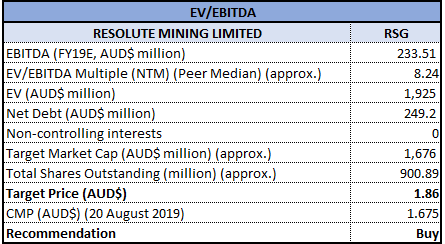

Valuation Methodology: EV/EBITDA Multiple Approach (NTM):

EV/EBITDA Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: Resolute Mining Limited’s share is presently trading above the average of 52 weeks high and low levels of $2.12 and $0.910, respectively. It made a sharp correction of around 21% from its recently made 52 weeks high level of $2.120. Moreover, it is trading at Fibonacci retracement level of 38.2%, and therefore the probability for a bounce back increases. On the backdrop of decent cash position and ongoing projects, it is expected that the company would be emphasizing on improving its bottom-line performance. Considering the present scenario, decent outlook for gold is likely to help the company to improve its margins further. Looking at the business prospects over the long-term, we have valued the stock using a relative valuation method, EV/EBITDA multiple and have arrived at a target price of double-digit growth (in %). Hence, in view of aforesaid parameters and current trading levels, we recommend a “Buy” rating on the stock at the current market price of $1.675 per share, down 2.332% on August 20, 2019.

.png)

RSG Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...