Kalkine has a fully transformed New Avatar.

Company Overview: Resolute Mining Limited (ASX: RSG) is a gold production company with several high-quality gold mines including the Syama Gold Mine in Mali, the Mako Gold Mine in Senegal and the Bibiani Gold Mine in Ghana. The company has also established strategic investments in highly prospective, well managed, African-focused gold exploration companies to provide a pipeline of future development opportunities. The company aspires to be a leader in mining innovation and aims to create sustainable economic growth in Africa. The company has over 30 years of experience as an explorer, developer, and operator of gold mines and over the period, it has gained significant operation expertise which provides a strong foundation for its future success..png)

RSG Details

.png)

Experience Operator of Gold Mines: Resolute Mining Limited (ASX: RSG) is a gold production company with multiple long life, high margin assets in Australia and Africa. The company is currently listed on the Australian Securities Exchange (ASX) as well as on London Stock Exchange (LSE), providing RSG improved access to gold and African-focused institutional investors. RSG has been an explorer, developer, and operator of gold mines for more than 30 years now and over this period it has produced more than 8 million ounces of gold. RSG’s vision is to be a multi-mine, low cost, African-focused gold producer. Over the period of 2016 - 2019, the company’s total revenue has increased at a CAGR of 5.78%.

.PNG)

Revenue Growth (Source: Company Reports)

RSG entered 2020 in a strong position to deliver on the full potential of its asset base and generate long-term value for its shareholders and broader stakeholders. Amid Covid-19 pandemic, the company has maintained its gold production with mining and processing operations continuing at the Syama Gold Mine and the Mako Gold Mine. At the Bibiani Gold Mine in Ghana, existing care and maintenance activities are continuing without interruption. With regional experience, secure supply lines, and robust relationships, RSG is well placed to deal with the challenges presented by COVID-19. Recently, RSG strengthened its balance sheet by completing debt refinancing and equity raising. The company seems to have the financial flexibility to pursue future growth opportunities and deliver on its strategy of being a multi-mine, African focused gold producer.

FY19 Performance Highlights: During the financial year 2019 or FY19, the company’s operations at Syama, Ravenswood and Mako produced 384,731 ounces of gold at an All-In Sustaining Cost of $1,577/oz. The company generated a revenue of $770 million and an underlying EBITDA of $208 million, reflecting the strength of core operations at Syama and Mako.

During the year, the company commissioned its Syama Underground Mine, successfully added the Mako Gold Mine to its portfolio, achieved exploration success across its portfolio with particularly exceptional results at Tabakoroni. Over the year, the company also completed the Ravenswood strategic review culminating in the sale of the project and significantly progressed its strategic review of Bibiani.

During the year, the company reported encouraging exploration results across its portfolio taking RSG’s Global Mineral Resource inventory to 19.1 million ounces of gold which is inclusive of 7.4 million ounces of gold in Ore Reserves. The company’s listing on the London Stock Exchange in June 2019 has raised its profile in global capital markets and has facilitated improved access to gold and African-focused institutional investors..png)

FY19 Results (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 53.69%. ICM Limited and Van Eck Associates Corporation hold the maximum interest in the company at 13.16% and 8.38, respectively..png)

Top 10 Shareholders (Source: Refinitiv, Thomson Reuters)

A Quick look at Key Margins: For FY19, the company’s gross margin and EBITDA margin stood at 9.2% and 10.7%, respectively. The company has an asset turnover ratio of 0.42x. RSG’s Asset to equity ratio stood at 2.27x, higher than the industry median of 1.78x. The company’s current ratio currently stands at 0.79x..png)

Key Metrics (Source: Refinitiv, Thomson Reuters)

March Quarter Performance: During March 2020 quarter, the company delivered decent production results while completing the Ravenswood asset sale and achieving important debt refinancing objectives. RSG started 2020 with a strong operating result, delivering around 100,000 ounces from Syama and Mako at a combined AISC of US$918/oz. Gold recovered in the March 2020 quarter stood at 119,683oz, up 15% on the December 2019 Quarter. Further, the company reported gold sales of 102,008oz at an average realised gold price of US$1,407/oz.

During the March 2020 Quarter, the company simplified its capital structure, reduced its borrowing costs and improved its financial flexibility through the completion of debt refinancing and equity capital raising activities. The new facility of US$300 million comprises a three-year US$150 million revolving credit facility and a four-year US$150 million term loan facility. The company’s net debt position at the end of March quarter stood at US$212 million, representing a reduction of US$109 million relative to 31 December 2019..png)

March 2020 Quarter Production (Source: Company Reports)

Repayment of Debt via Equity Raising: In January 2020, the company launched a ~A$195 million equity raising, comprising a two-tranche placement and share purchase plan (SPP). The funds from the equity raising are being used to repay all amounts outstanding under the US$130 million Toro Gold acquisition finance facility prior to the due date for repayment of 31 January 2020.

Vanguard Group becoming a Substantial holder: Recently, the Vanguard Group became a substantial holder in the company 57,995,943 ordinary shares in the company. The Vanguard Group now holds 5.259% voting power in the company.

Covid-19 Update: In response to Covid-19, the company has implemented company-wide new protocols and operating procedures which enabled the company to maintain its full-year production and cost guidance for Syama and Mako. No confirmed cases of COVID-19 at any of the company's sites or offices have been reported till now. The company’s gold production has remained unaffected by the pandemic. RSG has committed more than US$1 million to support African host governments in Mali and Senegal in their response efforts to combat COVID-19.

Key Risks: The COVID-19 pandemic poses unique risks and challenges to global mining companies operating in Africa. Further escalation of the COVID-19 pandemic, and the implementation of further government-regulated restrictions or extended periods of supply chain disruption, has the potential to negatively impact gold production, earnings, cash flow and the company’s balance sheet. Further, the company is also exposed to various environmental and social risks. The company’s operations may be impacted by the deterioration of the political environment and/or loss of licence to operate. Its operations could also be impacted by the negative environmental incident and critical operational or informational technology failure.

What to Expect: At Mako Gold Mine, the company is focused on maintaining high productivity and cash flow generative operations. Further, the company intends to optimise mine plan to support lower cost, longer life production. The company intends to operate Syama Underground Mine at full capacity while continuing high margin oxide operations. The company also intends to define mine plan for future Tabakoroni Underground Mine. With Syama poised to deliver on its potential, Mako on track to deliver another exceptional operating result and a pipeline of growth opportunities being progressed, 2020 is expected to be a positive year in the company’s history.

In FY20, the company expects its total production to be around 430,000oz at an All-In Sustaining Cost (AISC) of US$980/oz. From Senegal, the company expects the production to be around 160,000oz at an AISC of US$800/oz and from Syama Gold Mine, the company anticipated production to be around 260,000oz at an AISC of US$960/oz..png)

Key Valuation Metrics (Source: Refinitiv, Thomson Reuters)

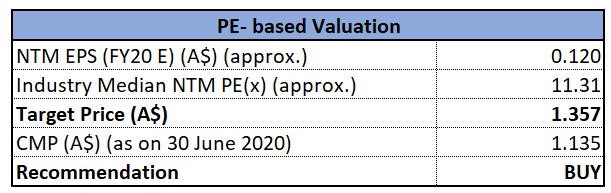

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (illustrative)

Price to Earnings Multiple Based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Over the last three months, the stock of RSG has increased by 20.54%, but it is still inclined towards its 52-week low, offering investors a decent opportunity for accumulation. Despite Covid-19 challenges, the company was able to maintain its gold operations in the March quarter, demonstrating the resilience of its business. With recent equity raising and debt refinancing, the company seems to have the financial flexibility to pursue future growth opportunities and deliver on its strategy of being a multi-mine, African focused gold producer. We have valued the stock using the price to earnings multiple based illustrative relative valuation method and have arrived at a target price with lower double-digit upside (in % terms). For the purpose, we have taken peers like St Barbara Ltd (ASX: SBM), Saracen Mineral Holdings Ltd (ASX: SAR) and Sandfire Resources Ltd (ASX: SFR). Considering the company’s resilient performance amid Covid-19, its decent operational and financial performance in FY19, FY20 guidance and its current trading levels, we give a “Buy” recommendation to the stock at the current market price of $1.135, up by 1.794% on 30 June 2020.

RSG Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...